Are The Magnificent Seven Valuations Justifiable?

The Magnificent Seven’s (M7) valuations have generated considerable attention, with the companies’ share prices skyrocketing since the end of 2022. Critics argue that these companies’ valuations are unjustified, with some drawing comparisons to the Dotcom era’s exuberance.

Taking a step back and looking at the fundamentals of these businesses, as well as what the market expectations are for growth in the years ahead, allows one to arrive at a more balanced view.

The advent of generative AI language models, like ChatGPT have provided the catalyst for the surge in the M7 companies’ share prices. At Nividia’s recent results, CEO Jensen Huang remarked that “AI is at the tipping point”, suggesting that the widespread use of AI technology is just beginning. If this is true, then perhaps there is significant runway ahead for a number of the M7 companies. A more cynical view would be that he is talking his own book.

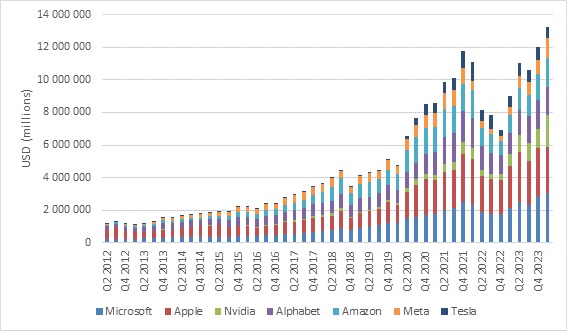

Over the past 11 years [1], the collective market capitalisation of the M7 companies has grown from just over US$1 trillion to well over $13trillion. This represents a remarkable compounded annual return of 24.3% – doubling the S&P 500’s capital return of 12% over the same period. Unsurprisingly, this growth has seen the M7’s contribution to the S&P 500’s market capitalisation soar from 10% to over 30%.

Graph 1: Market Capitalisation Q4 2012 – Q1 2024

Source: Refinitiv Datastream, Private Clients by Old Mutual Wealth (2024)

A closer look at the fundamentals

While this market capitalisation growth is impressive, the key question is whether the companies’ fundamentals have kept pace. As shown in graph 2, the M7 companies’ earnings have grown from US$9.8 billion in 2012 to $53.1 billion today. While impressive, this earnings growth has notably lagged the expansion in market capitalisation. Basic analysis suggests that collectively, when using earnings multiple, these businesses are considerably more richly priced today than they were in 2012. We acknowledge that this growth number will be heavily weighted to those companies generating the lion’s share of earnings. However, the narrative remains unchanged.

Click here to read more...