Swiss Re reports strong first quarter net income of USD 1.2 billion; premium income rises to USD 7.9 billion

• Group net income strong at USD 1.2 billion; premium income rises, reflecting profitable growth through large and tailored transactions • Property & Casualty Reinsurance net income USD 587 million; ROE 19.1% • Life & Health Reinsurance net income USD 244 million; ROE 16.1% • Corporate Solutions net income USD 80 million; ROE 13.5% • Life Capital net income USD 321 million; ROE 21.2%, supported by Guardian Financial Services acquisition • Strong return on investments of 3.7% in a challenging yield environment • Price quality of P&C Re portfolio remains attractive during April renewals • Moses Ojeisekhoba to become CEO Reinsurance; Jayne Plunkett to become Regional President and CEO Reinsurance, Asia and a member of the Group Executive Committee

Swiss Re reported strong net income of USD 1.2 billion for the first quarter of 2016, supported by solid underwriting and strong investment results. The Reinsurance Business Unit delivered strong results, benefiting from large and tailored transactions. Corporate Solutions achieved a net income of USD 80 million and invested in further profitable growth by expanding its footprint. Life Capital, created at the start of 2016, reported net income of USD 321 million, supported by the acquisition of Guardian Financial Services (Guardian). The Group also delivered a strong investment result, with a 3.7% return on investments. Swiss Re reported a very strong Group SST ratio of 223%. With the new capital actions approved at the 2016 Annual General Meeting, Swiss Re continues to focus on its capital management priorities.

Swiss Re's Group Chief Executive Officer, Michel M. Liès, says: "The overall environment remained challenging during the first quarter, in which low interest rates and declining reinsurance prices continued to make their mark on the entire industry. However, our strategic framework helped us navigate these market pressures. We continued to successfully differentiate ourselves through outstanding relationships with our clients and the development of tailored risk solutions, which resulted in several unique reinsurance transactions. We also made good progress on integrating Guardian Financial Services into Life Capital, which is already showing a strong contribution to our bottom line."

Strong first quarter Group results

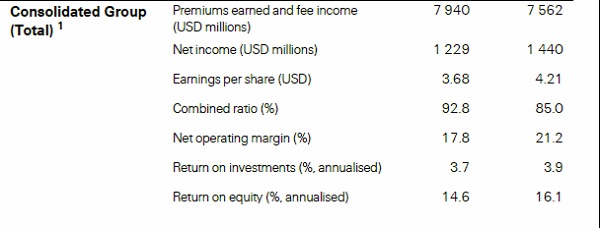

Swiss Re reported strong net income of USD 1.2 billion for the first quarter, below the USD 1.4 billion reported in the prior-year period. The result reflects continued good underwriting discipline and higher income from Life Capital.

The annualised Group return on equity (ROE) for the first quarter was 14.6% (vs 16.1% for Q1 2015), with earnings per share (EPS) of CHF 3.68 or USD 3.68, compared with CHF 4.00 or USD 4.21 for the first three months of 2015.

The net operating margin in the first quarter of 2016 was 17.8% (vs 21.2%). Swiss Re has introduced net operating margin as a new, more comprehensive metric to facilitate an easier comparison of performance not only across its three Business Units, but also across industries.

Premiums earned and fee income for the Group totalled USD 7.9 billion for the first three months of 2016, up from USD 7.6 billion for the same quarter of the previous year. At constant exchange rates, premiums earned and fees increased by 9.0%, reflecting growth in selected markets and lines of business, often through tailored transactions.

Common shareholders' equity increased to USD 34.8 billion as of 31 March 2016 from USD 32.4 billion at the end of December 2015. Book value per common share was USD 105.04 or CHF 100.57 at the end of March 2016, compared to USD 95.98 or CHF 96.04 at the end of December 2015. The Group's Swiss Solvency Test (SST) ratio was 223% as reflected in the submission to FINMA at the end of April 2016, reaffirming the Group's very strong capital position. For a better comparison with peers in the EU, Swiss Re today also published a comparable Group Solvency II ratio, which is estimated to be 312% on the same basis.

Swiss Re's Group Chief Financial Officer, David Cole, says: "We were able to demonstrate our resilience in the first quarter, differentiating ourselves via large and tailored transactions. All Business Units contributed to our strong profitability in the quarter and we remain very well capitalised."

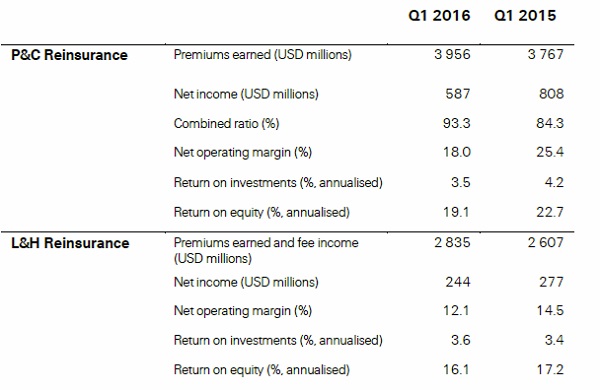

P&C Re reports net income of USD 587 million; ROE 19.1%

P&C Re delivered strong net income of USD 587 million in the first quarter (vs USD 808 million for Q1 2015), reflecting good underwriting and continued benign natural catastrophe experience and higher realised gains, partly offset by unfavourable prior-year developments. The annualised ROE for the first quarter was 19.1% (vs 22.7%).

Net operating margin in the first quarter of 2016 declined to 18.0% (vs 25.4%), due to a lower underwriting result, pricing pressures and prior-year developments.

Net premiums earned increased 5.0% to USD 4.0 billion, up from USD 3.8 billion in the prior-year period. At constant exchange rates, premiums earned increased by 8.9%, mainly driven by large transactions in the US and Europe. The combined ratio was 93.3%, compared to 84.3% for the previous year.

L&H Re delivers net income of USD 244 million; ROE 16.1%

L&H Re reported solid net income of USD 244 million for the first quarter, compared to USD 277 million for the same period in 2015. The decrease was mainly driven by lower realised investment gains. The ROE was 16.1% (vs 17.2% for Q1 2015).

The L&H Re net operating margin in the first quarter of 2016 was 12.1% (vs 14.5%) impacted by lower foreign exchange re-measurement gains and higher revenues.

Premiums earned and fee income rose to USD 2.8 billion. At constant exchange rates, premiums earned and fees increased by 13.6%, driven by several large transactions in the US, UK and Australia.

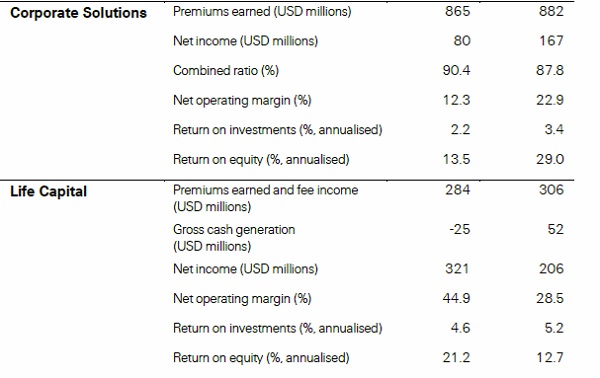

Corporate Solutions net income of USD 80 million; ROE 13.5%

Corporate Solutions reported net income of USD 80 million in the first quarter of 2016 (vs USD 167 million for Q1 2015). The 2016 result was driven by profitable business performance across most lines of business and moderate income from investment activities, partially offset by realised losses from insurance in derivative form, due to the continued impact of the unseasonably mild winter. The ROE was 13.5% compared to 29.0% in the same period of 2015.

Net operating margin in the first quarter of 2016 was 12.3%, (vs 22.9% in Q1 2015), impacted by lower realised gains on equities and realised losses from insurance in derivative form.

Net premiums earned were USD 865 million, a decrease of 1.9%, driven by foreign exchange rate movements. At constant exchange rates, net premiums earned increased 0.6%.

The combined ratio increased to 90.4% in the first quarter (vs 87.8%), with the prior period benefiting from favourable prior-year development. Both periods benefited from the absence of major natural catastrophe events.

In March 2016, Corporate Solutions completed the previously announced acquisition of IHC Risk Solutions, LLC (IHC), a leading US employer stop loss underwriter. This acquisition broadens Corporate Solutions' capabilities in the small- and middle-market self-funded healthcare benefits segment.

Life Capital delivers net income of USD 321 million; ROE 21.2%

Created on 1 January 2016, Life Capital manages Swiss Re's closed and open life and health insurance books, including the existing Admin Re® business and primary life and health insurance business. Comparative information has been restated accordingly.

For the first three months of 2016, Life Capital reported a net income of USD 321 million (vs USD 206 million in Q1 2015). The 2016 result includes the contribution from Guardian since the date of acquisition. Net realised gains on the Guardian investment portfolio contributed to the increase in net income in the period. The ROE was 21.2% in the first quarter, compared to 12.7% in the same period of 2015.

Life Capital's net operating margin for the first quarter increased to 44.9% (vs 28.5%) driven by the investment result, mainly from the Guardian portfolio.

Gross cash generation was a negative USD 25 million in the first three months of 2016 (vs a positive USD 52 million), reflecting the fact that from January 2016 the metric is calculated based on Solvency II, which is more sensitive to economic movements. As a result, large movements in interest rates and credit spreads can have a more pronounced impact on reported gross cash generation during a period.

Net premiums earned and fee income was slightly lower at USD 284 million (vs. USD 306 million).

April renewals maintained attractive portfolio; price erosion slowed

The April treaty renewals saw Swiss Re increase the volume of renewed business by 13%. The year-to-date price quality, at 102%, is the same as during the January renewals, exceeding the company's economic return hurdles. Swiss Re maintained an attractive portfolio, supported by large and tailored transactions. The price erosion for property natural catastrophe business has slowed, while casualty markets remained relatively stable.

Moses Ojeisekhoba to become CEO Reinsurance, Jayne Plunkett to succeed him as Regional President and CEO Reinsurance, Asia

Following the announcement that current Group CEO Michel M. Liès will retire after four successful years and that Christian Mumenthaler, currently CEO Reinsurance, will succeed him as of 1 July 2016, Swiss Re's Board of Directors announces that Moses Ojeisekhoba (49, Nigerian and British), currently Regional President and CEO Reinsurance, Asia and a member of the Group Executive Committee, will become the new CEO Reinsurance. Jayne Plunkett (46, American), currently Head Casualty Reinsurance, will succeed Moses Ojeisekhoba as Regional President and CEO Reinsurance, Asia. As part of this move Jayne Plunkett will become a member of the Group Executive Committee. Both moves are effective 1 July 2016.

Christian Mumenthaler, currently CEO Reinsurance, says: "I am excited about these two announcements as both Moses and Jayne are very strong leaders with impressive track records. They have an exceptional depth of experience, especially in strategic areas where we will look for further growth, including high growth markets, casualty lines, transactions and the opportunities driven by technological change."

Moses Ojeisekhoba has been with Swiss Re since 2012, when he was named Regional President and CEO Reinsurance, Asia. Together with his team, he has increased both Swiss Re's market share and its profit share in the region over the last four years while simultaneously improving operational efficiency. He also led the High Growth Markets initiative for the Reinsurance Business Unit on a global basis. His career has spanned more than 25 years in both life and non-life insurance, from personal to commercial lines, and he has lived in Africa, Asia, Europe and North America.

Jayne Plunkett has worked in the re/insurance industry for 24 years, with roughly equal experience in insurance and reinsurance. She has held positions of increasing responsibility in Swiss Re since 2006, when she joined in the context of the acquisition of GE Insurance Solutions. Since that time she has consistently proven to be effective and adaptive, delivering results from three continents – North America, Asia and Europe. From 2008 to 2012 she worked in Asia as Swiss Re's Head of Casualty Underwriting for the region, during which time she grew premiums and net income significantly. In addition to her current global role as Head Casualty Reinsurance, where she focuses on growing and developing business in response to technological changes, she also manages the unit handling all large and complex transactions for P&C Re.

Swiss Re well positioned to capture opportunities ahead

In a challenging external environment, Swiss Re is well positioned to capture the opportunities that lie ahead, and continues to shape the re/insurance industry. Large and tailored transactions drive a growing share of Swiss Re's results. These are complex solutions that bring unique added value to its clients. Swiss Re is on track to reach its financial targets over the cycle.

Michel M. Liès, Swiss Re's Group Chief Executive Officer, says: "In the first quarter of 2016, we have – once again – demonstrated our resilience in a soft market. I expect that we will continue to operate amid a challenging environment throughout the year – but this plays to Swiss Re's strengths. In this demanding business environment there is little substitute for global expertise and long-range vision, both of which we bring to the table. Moreover, closing the protection gap remains a priority and this is why the fundamental demand for insurance remains intact – creating new opportunities across all lines of business. I am confident that Swiss Re is well positioned to continue to deliver sustainable results and capture attractive business opportunities going forward."

Michel Liès continues: "I'm very pleased to see Moses and Jayne moving to their new roles. Swiss Re invests a great deal in finding and retaining the best people and these moves just show how these investments pay off. Of course the biggest beneficiaries are our clients, who enjoy Swiss Re's depth and breadth of expertise on a day to day basis, at all levels and areas of the organisation. It's part of what makes Swiss Re unique."

Details of first quarter performance (Q1 2016 vs Q1 2015)

1 Also reflects Group Items, including Principal Investments.

To see key information click here.