What difference does a quarter of a percent interest rate change make?

Guy Fletcher, Head of Research and Client Solutions at Sanlam Investments.

So there you were, going about business as usual, when unexpectedly you hear the murmurs – the MPC could cut interest rates today! Suited men nod sagely while CNBC Africa invites experts to share their knowledge. Friends tell you how successful they’ve been at investing while you are struck by a dawning sense of FOMO – what should you do and why? Guy Fletcher, Head of Research and Client Solutions at Sanlam Investments unpacks the knock-on effect of even a small percent change in interest rate on investments.

Economists, media commentators and investment professionals alike spend multiple hours observing the nuances of Central Bank policy announcements, the way that the committee members voted and what their expectations are. However, interest rate policy is acknowledged to be a fairly blunt instrument in supporting economic growth and managing inflation risk, often with (at best) an impact that takes many months to take effect.

So why should we concern ourselves?

Interest rates are considered to be important since they underpin the very foundation of asset pricing – in simple terms, the price of an asset is considered to be the present value of all the future payments that asset will make, whether in the form of dividends from equities or coupons from bonds. Higher interest rates imply lower present values and vice versa.

Two observations must be made:

a) the impact that a change in short-term interest rates has on asset price formation is thus increasingly a function of the persistence of that change and

b) the sustainable impact of these changes on real long-term interest rates is, perhaps, at odds with standard monetary theory that argues that the markets will ultimately dominate central bank interventions.

So far, so good, but who sets interest rates?

Historic monetary policy

The South African Reserve Bank currently has full operational autonomy – the Monetary Policy Committee sets the levels of interest rates (commonly known as the repo rate or the rate at which commercial banks borrow rands from the Reserve Bank) within an inflation-targeting framework. However, monetary policy has evolved over the previous decades with the Governors since 1990 as follows:

• Dr CL Stals : 8 August 1989 to 7 August 1999

• Mr TT Mboweni : 8 August 1999 to 8 November 2009

• Ms G Marcus : 9 November 2009 to 8 November 2014

• Mr L Kganyago : 9 November 2014 to date

South Africa introduced inflation targeting in February 2000 after a proposal to adopt the framework in August 1999; prior to adopting this, the Reserve Bank had followed policies including: (source: SARB)

• exchange-rate targeting

• discretionary monetary policy

• monetary-aggregate targeting

• an eclectic approach (multi-method)

“The SARB acknowledges that monetary policy cannot directly contribute to economic growth and employment creation in the long run. However, by creating a stable financial environment, monetary policy fulfils an important pre-condition for the attainment of economic development”.

This clearly has implications regarding the analysis of interest rate policy since the Reserve Bank was executing interest rate changes for different reasons and under different economic conditions (witness Governor Stals’ attempt to shore up the Rand during the 1997/8 Korean crisis). Thus, any direct inferences must be tempered with a healthy respect for prevailing policy implications.

And, similarly, it makes you wonder what was on the Public Protector’s mind when she challenged the SARB’s mandate!!

The data

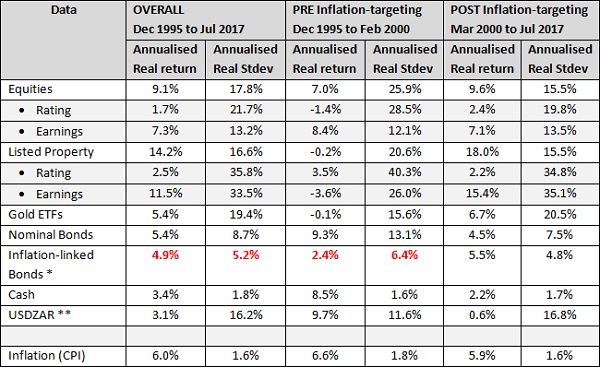

Let’s have a look at the historical evidence within the South African markets to see whether interest rate changes have a direct and sustainable impact on asset price formation. In doing so, we will break the information into two sets: pre- and post-inflation targeting, the former commencing December 1995 (after the new regime had settled down), and the latter commencing February 2000. Please note that the numbers presented below are in REAL terms.

Source: IRESS, Sanlam Investments, August 2017

* The ILB numbers pre-2000 have been estimated from post-2000 relationships for the sake of completeness

** Note that the USDZAR real return is the change in the exchange rate adjusted by the difference between the SA and US CPI rates