The critical role of a consultant in umbrella funds

FAnews received a press release penned by Magda Wierzycka, CEO of Sygnia Group in which she stated that there is widespread and insidious conflicts of interest that is corrupting the retirement savings industry and calls on regulators to assist millions of South African savers. We asked Sanlam's David Gluckman for his opinion. Below Wierzycka views is Gluckman’s views.

The critical role of a consultant in umbrella funds

By Magda Wierzycka – Sygnia Chief Executive Officer

As more and more companies abandon their stand-alone retirement funds in favour of offering their employees umbrella fund arrangements, it becomes more important to monitor the “value for money” that employees receive.

Fortunately, most companies that have made the change have put a management committee in place to do just that. Unfortunately, South African umbrella funds well deserve the moniker of “opaque” when it comes to full disclosure of all fees and charges.

As it currently stands, most commercial umbrella fund arrangements are provided (under the label of being “sponsored”) by the same financial services companies that provide consulting and administration services to the stand-alone retirement funds. The “big five” umbrella funds are offered by Alexander Forbes, Momentum, Old Mutual, Sanlam and Liberty. Hence, when a stand-alone retirement fund folds into an umbrella fund, the board of trustees tends to be steered, through a carefully choreographed tender process, into retaining the same consultants and administrators as they had as a stand-alone fund. This is a major error of judgement, as the relationship going forward is rife with conflicts of interest.

Where the consultant is employed by the sponsor of the umbrella fund there can be no independent, objective advice with respect to any aspect of the umbrella fund arrangement. The only exception is the rare umbrella fund where the sponsors are themselves independent consultants and all the providers are appointed on an arms-length basis.

To fully appreciate the insidious nature of the large umbrella funds, it is enough to look at the range of products and services built into these arrangements – and charged for – by the sponsor:

- Consulting services

- Investment products

- Investment administration platform

- Liability administration

- Risk benefits (death and disability cover)

- Ancillary benefits e.g. wellness programmes, funeral cover

Where all of the above are provided by a single party there is huge scope for abuse. The key party contributing towards the status quo being maintained for service providers is, of course, the consultant. In practice the consultants employed by the large institutions steer the management committees away from fair and transparent competitor reviews and maintain the illusion that the client is receiving the best cost and investment performance proposition. At the end of the day his salary and bonus depend on the sponsor – his allegiance is thus not difficult to figure out. And yet so many management committees miss this point entirely, blindly trusting the consultants to provide objective advice. As one of my ex-bosses was fond of saying, you are asking turkeys to vote for Christmas.

I was very amused by a recent Moneyweb article in which Anne Cabot-Alletzhauser, the head of the Alexander Forbes Research Institute, was brave enough to say that pension fund savings should be provided at a total charge of 0.75% pa. I am prepared to put my head on the block that not a single Alexander Forbes consultant has taken that message back to their clients and definitely not those who participate in the Alexander Forbes Retirement Fund and who, in most cases, pay between two to four times more than the quoted 0.75% pa.

So what does a good governance model look like in the umbrella fund environment?

The fundamental first step for any company considering the move to an umbrella fund, or reviewing their current umbrella arrangement, is to appoint a consultant independent of any sponsor of an umbrella fund to oversee the tender process. Once in an umbrella fund, the appointment of an independent consultant should be a prerequisite. In fact, it is something that the regulators should insist upon. Once the consultant is in place he should be tasked with regular reviews of the quality of service provided by the umbrella fund, the investment performance delivered and the costs associated with the arrangement. Risk benefits should be put out to tender at least once every three years to make sure that members benefit from the lowest quotations.

The appointment of an independent consultant is the key to ensuring that employees retire in comfort. The best part is that most companies already pay for that “consulting”, bundled as it is into the umbrella fund proposition. So there should be no increase in cost – there is merely a switch from tied non-independent consulting advice to objective independent advice.

I cannot emphasise this enough. A consultant seconded to the management committee by the umbrella fund sponsor is highly unlikely to alert the management committee to poor investment performance or to high costs. Nor is he likely to recommend any other risk provider than his own employer.

To disclose my own conflicts of interest, Sygnia recently launched the Sygnia Umbrella Retirement Fund (SURF), with no consulting or administration fees. There is only one fee, an asset management fee. The objective has been to leave plenty of “financial” scope for the appointment of the independent consultants.

The launch of SURF has been met with dismay by the umbrella fund industry, which promptly responded by dropping administration fees to nil for new business quotes. Again I am willing to put my head on the block that the “consultants” associated with those umbrella funds did not present the “nil administration fee” proposition to their existing umbrella fund clients (for the sake of full transparency, we have recently encountered both Old Mutual and Sanlam umbrella funds quoting nil administration fees on new business). In fact, most umbrella funds have cut their charges over time to attract new business as competition in the umbrella fund space has grown. Once again, the consultants have seldom taken the lower fees offered to new clients to their existing client base. That fact alone should destroy the perception that independent advice is being provided and that the fundamental trust in the relationship with a tied consultant is one of fiduciary care.

It is time for corporate South Africa to take back control of their retirement savings arrangements from the financial services industry. It only takes one step. It is also time for regulators to become involved. Again, all it would take is one directive to clean up the greatest abuses in the retirement savings industry to the great benefit of all South Africans valiantly saving for their retirement.

The critical role of a consultant in umbrella funds

By David Gluckman Head: Special Projects, Sanlam Employee Benefits

“Consistency is the only currency that matters” is a well-known slogan of one of South Africa’s leading asset managers.

At the other end of the spectrum, a new player entered the commercial umbrella fund market less than 4 months ago proudly announcing “one all-in fee as a percentage of assets under management” and illustrating projected cost savings to clients adopting this model versus the competing leading commercial umbrella funds. Besides some fees such as costly hedge funds being over and above the so-called “one all-in fee”, importantly all these projections assumed there would be no need to separately pay for the services of a consultant. Today the message is slightly different and we should now understand that these projections were never accurate in that the true intention was always to leave “financial room for the employment of independent consultants.”

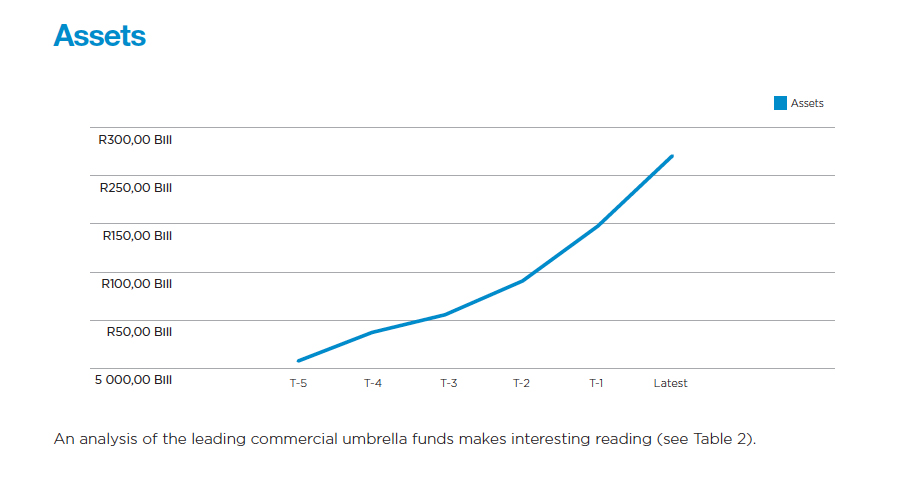

But the new player does raise some valid questions as regards the most appropriate governance model for commercial umbrella funds. These questions are important given the massive growth in this market (see figure below).

Two recent experiences highlighted to me that a very important question to explore is what will in the future be the role of the consultant in commercial umbrella funds.

- One highly respected independent consultant to a large book of Sanlam Umbrella Fund clients (and who also has many clients participating in other major commercial umbrella funds) raised the issue with me at our 2016 Sanlam Employee Benefits Benchmark Symposium, and said he is worried about the sustainability of his business given the increasing power of the major commercial umbrella fund sponsors.

- Various senior Financial Services Board officials also raised the matter in an April 2016 workshop with Sanlam Umbrella Fund representatives, essentially asking whether consultants introduce an extra and unnecessary layer of costs. They wanted to explore whether Sanlam could instead provide these advisory services thus savings costs for the ultimate clients of umbrella funds being the members.

The Sanlam Umbrella Fund governance model was structured consistently with thinking as set out in my paper entitled “Retirement Fund Reform for Dummies” presented to the Actuarial Society of South Africa as far back as 2009. In that paper I argued:

“The role of intermediaries (aka consultants) requires particularly close scrutiny. I would argue their role is a particularly vital one if we want to create a culture of effective competition.

Rusconi argues “In the institutional space, however, savings levels are less likely to change and marketing is more about attracting another provider’s customer than about motivating additional savings”.

Such arguments emanate from the premise that intermediaries do not add value to consumers - an assertion that I would challenge. My view is that there are both good and bad intermediaries, and we need to find a model where market forces will push in the direction of forcing intermediaries to continually “up their game”. There are many good intermediaries who not only fight for the rights of their clients, but also serve as an effective means to ensure that product providers are continually aware of the need to provide quality service in an increasingly competitive environment.”

I then went on to argue in that paper that commission should be deregulated and that “In an environment of unregulated commission scales, intermediaries would be forced to demonstrate their true value add to consumers. This would include demonstrating their degree of independence from product providers. Certainly the market we would end up with is very different to what it looks today – I would argue we would end up with a better more efficient market, with fewer but more effective intermediaries each forced to continually focus on delivery to their clients.”

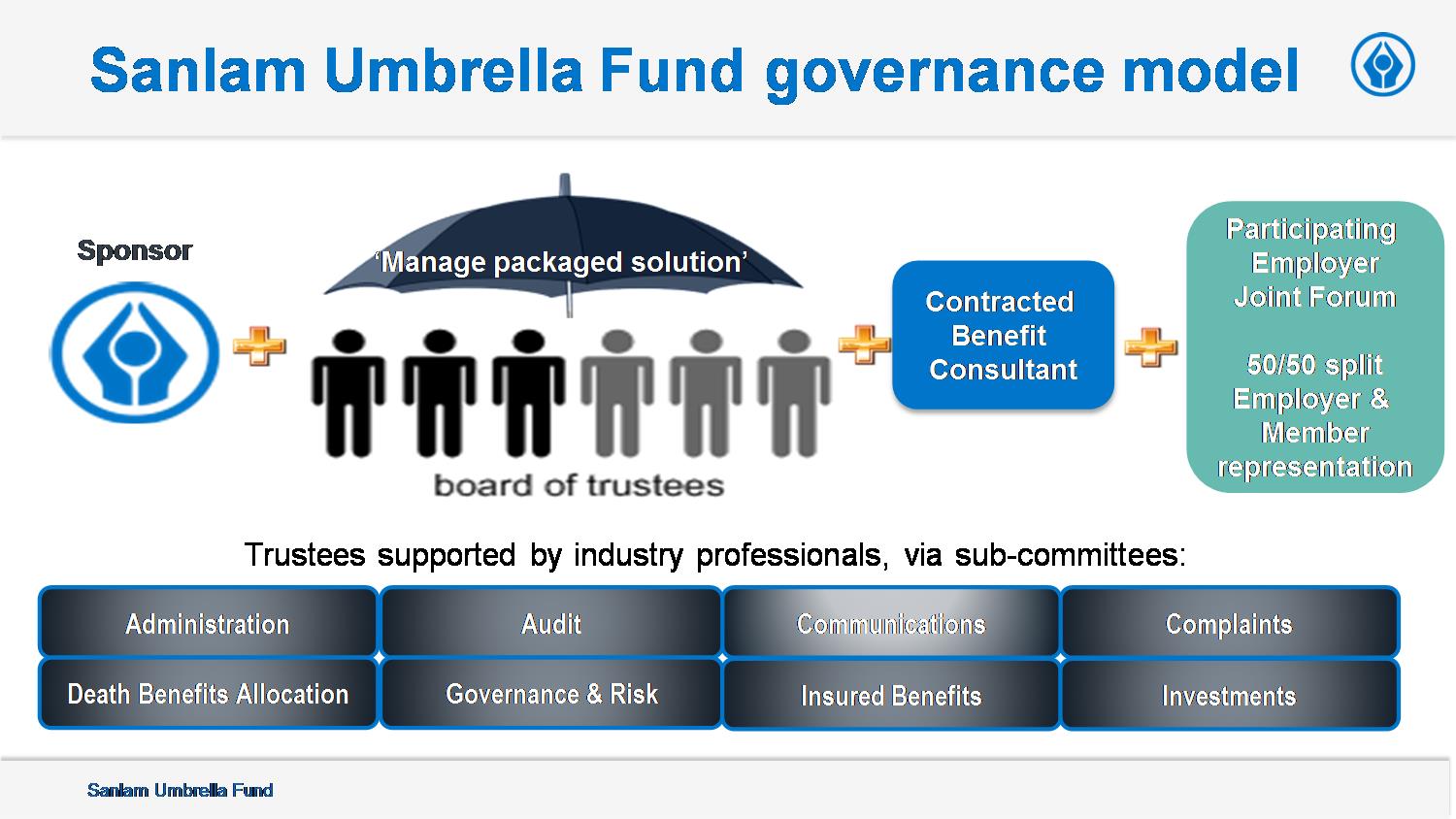

The forward thinking Sanlam Umbrella Fund governance model (see figure below) attempts to clearly define every accountability and allocate it where most efficient.

The role of the Contracted Benefit Consultant (not to be confused with the non-advisory Sanlam Client Relationship Manager responsible to ensure smooth day-to-day administration service delivery) is vital and we have attempted to define and contract in writing the services to be provided by this important stakeholder. Furthermore these services are remunerated on a monthly fee-for-service basis, and one will find no mention of the term ‘commission’ in any Sanlam Umbrella Fund product material. The services might evolve and differ from the traditional intermediary services provided to stand-alone retirement funds, but in our view this key stakeholder will always remain the trusted face to face confidant of the client and pivotal as regards advisory and communication services.

That is why, in our April 2016 workshop, we responded to the the FSB officials’ queries that ‘yes’ in theory Sanlam could step in and provide similar advisory services to the consultant, but there would be no cost saving to clients were the identical level of services to be provided by similarly qualified individuals, and worse still that would represent a significant backward step to building a competitive commercial umbrella fund industry.

Indeed our practical experience over the last 8 years since the launch of the Sanlam Umbrella Fund is that good consultants can and do add significant value to their clients, and represent an important balance of power to protect members’ interests.

We hold out and believe the governance model as set out above is the optimal solution as our policymakers grapple with how best to structure a future commercial umbrella fund model that even today is not yet adequately defined in legislation. Consistency!