Slowly then suddenly: The power of sustained success

When we think about breakout success, we often envision a phenomenon characterised by sudden and rapid changes—a rocket launching into orbit, for example.

The default condition of a rocket is to be stationary on the ground, but in a relatively short period, it leaves the earth’s atmosphere. To achieve this, the rocket must overcome Earth’s gravitational force, requiring an extraordinary amount of energy. To reach escape velocity, the rocket needs to travel at 11.2 kilometers per second or 40,234 kilometers per hour.

Let’s consider the definition of velocity for a moment. Velocity is defined as displacement per unit of time - a measure of how much work has been done (distance covered) in a given amount of time. This concept of work done over time is pervasive across many fields, including commerce and economics, where the equivalent is production or yield over a given period. Since time is the most static of variables (we cannot change it in any way), the focus often shifts to magnitude - how much work has been done.

We compete on the top speeds of performance vehicles, debate the profitability of various industries, and rank the annual performance of investment professionals. In a time-scarce world, it’s reasonable to emphasise (and even celebrate) the magnitude of achievement. But are we missing something equally potent by not giving the same degree of focus to how long something can be sustained?

Duration: force majeure

“You can be an extraordinary investor by earning average returns for an above-average period of time.”

- Morgan Housel

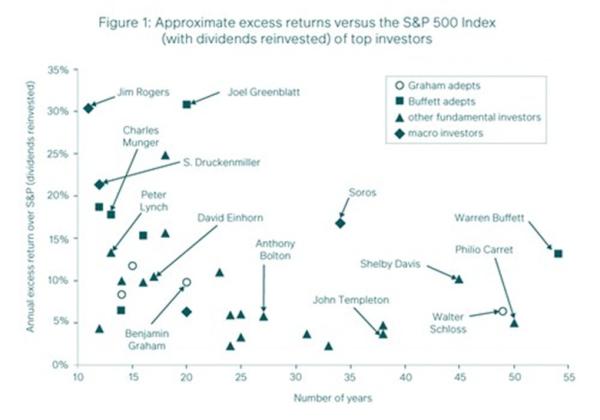

The figure above, sourced from “Excess Returns” by Frederik Vanhaverbeke, offers a valuable comparison of the excess returns achieved by several rockstar investors (relative to the S&P 500) and the length of time over which those excess returns were sustained.

One might notice a general negative relationship between the magnitude of excess returns and the number of years they were upheld. The two-dimensional nature of an x-y plot implies equal importance between these two variables, but this depends on the underlying investor and the opportunity set. However, it does appear, based on how few investors have achieved it, that sustaining excess returns for a long period is rare.

The benchmark return against which all these investors are measured is running at 10% per annum, in line with the long-term average return of the S&P 500. While this isn’t entirely accurate, it doesn’t detract from the point being made. The charts depict three time periods: 20 years, 35 years, and 55 years.

Click here to read more...