Saving vs Investing

Conventional economics say you can foretell a country’s future by its domestic savings rate. In South Africa’s case, the national savings rate is precariously low, particularly compared with some BRICS member countries. For example, South Africa’s savings rate is less than 18% of GDP compared to over 42% in China.

Tradingeconomics.com recently reported a drop in the South African household saving ratio, by 0.4% from the last quarter of 2017 to the first quarter of 2018. This results in a negative savings trend, which we have long been used to, at least consistently from 2008, save for two quarters in 2017.

This is a concerning trend, which does not bode well for the ability of the average South African to adequately provide for shorter term emergencies, or longer term retirement requirements.

This may be a result of a lack of knowledge as to how to save. Retail banks have largely discontinued interest of credit balances in current accounts, a common reserve for surplus funds, and the complex world of investing or savings, exacerbated by poor financial knowledge, makes the problem easier to ignore.

Further to this, those of us that do save, often do not understand how to maximise our return, often using incorrect account types with lower returns that does not make the best of the compounding factor of investing. The question we are faced with is do I save my money, or do I invest it? According to finweb.com, saving, by definition, involves the protection and preservation of money from loss. Investing, on the other hand, means to make a long-term commitment of putting money away and letting it grow.

Investopedia.com also suggests that as a general rule of thumb is we should not save long term but should invest long term. We should not invest short term, but save short term. Many individuals do not know this, or even if they do, are often scared of investments post the 2008 crisis, that saw many lose a lot of value on equity (stock market) investments. Is this necessarily true?

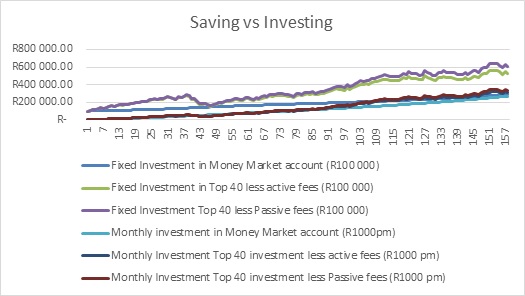

At Alexander Forbes we researched the longer term returns for savings product versus investments by studying the most popular saving vehicle, namely the money market account, compared to the average returns that one would expect to achieve from an equally popular equity investment index, being the Top40 over various periods of time.

Whilst both the saving and investment landscape is quite vast, and individuals would have to get personal advice regarding their level of risk to make more informed choices, this comparison attempts to simplify the analysis to make it understandable.

We looked at two potential scenarios: investing or saving a lump-sum of R100 000 and investing or saving a monthly amount of R1000, either in a Top 40 fund, advised or passively in a money market account. We used various time periods to test the return theory, and included a 5 year period, 10 year period and a 13 year period which encompassed the financial crisis of 2008/09, to understand if the outcomes change when invested through a market crash.

We made the following assumptions given the complexity of the analysis and number of offerings in the market:

1. Money market rates are assumed to be set at the Repo rate plus 1%, consistently. In the research, this would usually be top rate offered in the market, and if anything would err to overstate reality a little, given that many institutions only offer the rate on higher balances

2. The “Active Management” fee assumed was 1.3% p.a or 1.083% per month

3. The “Passive Management” fee assumed to was 0.25% p.a or 0.02083% per month

Both fees in 2 and 3 above are relevant in the current investment period.

The results are quite telling:

Over the total period of 157 months (May 2005 to May 2018), the equity investment income out performs returns from the savings products in both lump sum and monthly saving scenarios, however for shorter periods the results are mixed. The quantum of the returns can be seen in the table below.

In the longer term the equity market performance is quite significantly higher than the savings performance, up to 2.13 times more for lump sum investments and 1.25 times for monthly investments. For shorter dated investments we can see mixed results with the money market investment outperforming the equity investment in the 5 year term by a small margin.

On conclusion, before making these investment choices, one should take into account personal circumstances and needs over time. Professional advice is also very important, so get yourself good financial advice, and do your homework.