Reflecting on the year that was

Victoria Reuvers, Managing Director of Morningstar Investment Management South Africa

At face value, it appears as though markets have performed well, however, broadly speaking there have been some landmines that simply could not have been avoided by all investors. 2021 was also by no means a dull year – global bonds bottomed out, the Evergrande debacle, Chinese tech stocks slumped and the contagion of it all to emerging markets.

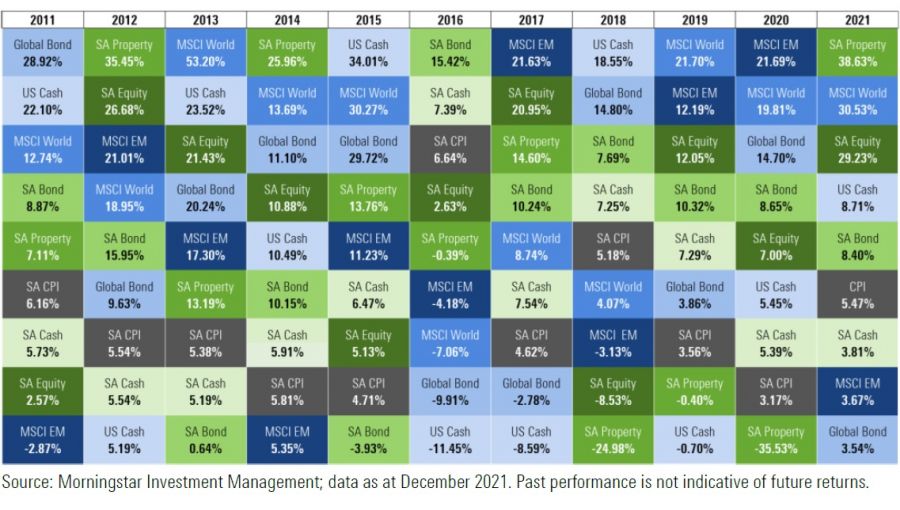

If we look at the various asset classes across the calendar year, the first point that stands out is the broad positive returns across all the nine asset classes in 2021 (as can be seen in the chart below). The second is the rotation in the ranking, highlighting the importance of diversification.

Looking at local markets in 2021

- S.A. Equities are making a comeback

After a seven-year drought of returns for domestic equities, the past 18 months have seen a strong rebound in S.A. equities with broad-based returns across the sectors. While 2020 saw resource shares (mainly platinum and diversified miners) performing well, 2021 saw a rotation into more unloved areas of the market. Looking back at 2021, the strongest performing areas were what we would term “S.A. Inc.” shares, namely banks, retailers and select industrial shares.

What caught many investors by surprise in 2021, was the sharp fall in the Naspers and Prosus share price. Market darling Naspers, combined with Prosus (its European listed counterpart) account for almost 20% of the All-Share Index. A combination of concerns regarding the Chinese government’s interference in their market with regards to the new regulation for select tech companies alongside the disappointment surrounding the Naspers Prosus share swap and/or company restructure has proved to be strong headwinds for these shares.

- Fixed Income, wasn’t so ‘fixed’

Fixed income managers did not have an easy year, with 2021 not being the year for income assets. What had appeared to be a stable (and dare I say “boring” asset class) was no more, as 2021 saw fixed income assets experience a lot of volatility.

- S.A. Government bonds bamboozled

S.A. Government bonds remain perplexing. We are seeing good value in this asset class, with S.A. government bonds offering a yield of around 9.5%. This is almost 5% ahead of cash and 4% ahead of inflation, which is unheard of in global markets. Yet despite this attractive yield, foreigners have not been investing in our bond market to the levels they have previously. As a result, this asset class is generating a decent yield for investors but has been subject to market volatility this year due to the lack of foreign support.

- Cash is still out in the cold

We see little room for holding cash in portfolios. Not only is the nominal yield low (around 4%), it is in fact offering a negative real yield, given that inflation is close to 5%.

Turning to global markets, it seems nothing could stop this bull.

While value shares and unloved sectors (such as energy and UK equities) certainly rallied and were solid contributors to portfolio performance, the tech stocks in the US reached stratospheric levels (both in terms of performance and in price).

In our opinion, this sector is starting to carry a striking resemblance to the tech bubble of the late 90s. Firstly, the market is trading at extreme valuations and is experiencing new IPO’s (stock listings) in the magnitude last seen in the late 1990s. (If it walks like a duck and talks like a duck…) We prefer to be cautious at this point. We remain materially underweight US large-cap tech shares.

Despite emerging markets selling off sharply on the back of the Chinese government’s interference in capital markets and the restrictions and regulations placed on their tech companies, we are seeing good pockets of opportunity in emerging markets.

It was not only S.A. fixed income managers that had a tough time in 2021; global fixed income managers had it even worse. Global bonds were one of the worst performers in 2021. With starting yields at low levels and bond yields rising throughout the year, this led to bondholders experiencing meaningful capital losses.

How have we positioned Morningstar portfolios?

Our Morningstar capital markets work guided us to have meaningful exposure to domestic equities, with an overweight allocation to the S.A. Inc. shares (which benefitted portfolios). We have always had an implied 10% cap exposure to Naspers and Prosus combined, which also helped limit drawdowns as this share fell. I have to say that for the years that this share drove returns, the implied cap we held in portfolios resulted in a contained drag on performance. Nevertheless, risk mitigation is key. We are prepared to forego some upside in order to protect on the downside.

We have remained fully invested offshore with the majority of this allocation being held in global equities. This allocation has been a solid contributor to performance as we have captured the returns from global equities markets, despite the rand zigzagging between R14.50/$1 – R16,50/$1. We have a healthy exposure to emerging markets which detracted marginally from performance; however, this remains a high conviction allocation looking forward.

Our meaningful exposure to S.A. government bonds has not provided the returns we had envisaged, however, when compared to cash, it has been the right decision. We remain confident in this holding as we expect interest rates to rise in 2022 (albeit in small increments) and this should be beneficial for long-dated government bonds.

Looking forward – onwards and upwards into 2022

Overwhelmingly, the so-called “TINA Theory” narrative from 2021 is still alive and well as we enter 2022. For a while now, the TINA - "There Is No Alternative" – Theory, has been used as the reason or basis for why the current bull market simply won't quit.

The fact that we have very low cash yields and very low global bond yields has pushed investors towards riskier assets such as stocks, which seemingly continue to go up (and up, and up). Let’s not forget that equity markets looked fairly expensive going into 2021—and many key markets are again looking expensive going into 2022.

In the wise words of Warren Buffett – “Be fearful when others are greedy and greedy when others are fearful”. There is much exuberance, easy money and excitement in certain areas of the market. This level of optimism and crowding makes us “fearful”.

There will be good news stories for companies and sectors that will be extrapolated into the future with investors prepared to pay extreme prices just to own these golden companies. Remember that “Price is what you pay, but value is what you get” – another valuable lesson shared by Mr Buffett. Now is the time to be vigilant and to ensure that you are getting value for what you buy.

At Morningstar, we are certainly seeing attractive opportunities in select areas of the market. While we have a healthy exposure to select equities (both domestic and global) we also retain our holding in S.A. government bonds in favour of cash and global bonds. As a result, our portfolios are constructed to invest in areas where we see good long-term upside but also to ensure that risk is considered and there is a balanced exposure to both growth and income assets.

You may not know if you should choose heads or tails, but at least you have the coin.

You may hear some commentators saying that “markets are expensive and now is not the time to be invested” whereas others say that “things will just keep going up”. To this we would say there is never a “right time” to invest, the key is just to be invested and to remain invested.

To quote Morgan Hounsel “Compounding works best when you can give a plan years or decades to grow. This is true for not only savings but careers and relationships. Endurance is key.

And when you consider our tendency to change who we are over time, balance at every point in your life becomes a strategy to avoid future regret and encourage endurance.”

As you reflect on the year that was, you can be pleased knowing that you remained invested and that you now have more wealth than you did this time last year. The seasons will inevitably keep changing, and so too the seasons for asset classes. This is exactly why your portfolios are being actively managed to ensure that as markets change, your investment changes to take advantage of the next cycle. All you need to do is stay invested and let the magic of compounding do its work.