Old Eras and New

The story of South Africa’s modern economy cannot be told without Anglo American, the giant mining conglomerate that also owns De Beers.

It was the Kimberly diamond rush in 1867 and Witwatersrand gold stampede in 1886 that forcefully pulled South Africa into the global economy and financial markets. The dark flipside of the rapid development and industrialisation was the exploitation of black workers from across Southern Africa, planting the seeds of the apartheid system.

Anglo American’s name points to its origins and global links, started in South Africa in 1917 by a German Jewish immigrant, Ernst Oppenheimer, with funding from American and British investors and lenders. It became a major mining conglomerate, but by the 1980s capital controls meant its profits were trapped domestically, and it ended up as a sprawling domestic business empire, owning everything from banks to wine farms. In the post-apartheid era, it returned to focusing purely on mining, listing in London to raise capital for its global ambitions. The fact that it is now widely seen as a takeover target or a candidate for restructuring suggests that this goal was achieved only with mixed success.

Without getting into the merits of BHP’s unsolicited bid for Anglo American, which the latter has already rejected, or the many complexities associated with such a transaction, or speculating too much on Anglo’s future, there are at least three notable elements worth exploring. Firstly, what does it tell us about the global mining cycle? Secondly, what does it tell us about South Africa’s mining climate? Thirdly, what will it mean for the JSE if a stalwart share was to disappear?

Dr Copper

BHP is primarily interested in Anglo’s South American copper mines. Copper remains the best metal for conducting electricity, and therefore has a major role to play in electrification of energy supplies and the green transition. A battery-powered electric vehicle requires about three times more copper than a traditional internal combustion car, for instance. Even if elements of the green transition end up lagging expectations – electric vehicle sales have recently lost momentum internationally though production has been ramping up in China – the artificial intelligence boom will put great strain on electrical grids. As much as we think of AI as existing somewhere “in the cloud,” it very much has a physical presence in data centres and needs consistent electricity supplies. All this will require copper. For instance, last week Microsoft announced a $10 billion deal with Brookfield to purchase 10GW electricity to power its data centres. That is enough electricity for 1.8 million homes.

Global copper production seems unlikely to keep pace with this demand, based on the mines that are operating today. Future mines might, but they still need to be developed, a complex process that takes a decade or more from start to finish due. Regulatory hurdles are often a bigger challenge than the engineering ones. Indeed, the reason there are always big commodity cycles is because of the long lags between demand rising and supply responding. Often, by the time supply responds, demand has turned and prices slump.

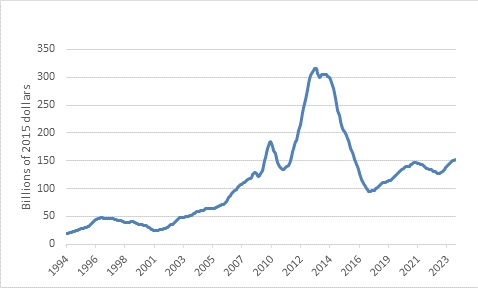

Anglo learned this lesson the hard way. In 2008, at the peak of the commodity boom, it paid $5 billion for Minas Rio, a Brazilian iron ore project under construction. When the mine finally started producing iron ore in 2014, market dynamics were very different and the iron ore price about 40% lower. The debt associated with this project (and others) posed an existential risk to Anglo in 2015 and before commodity prices turned somewhat. Other miners experienced something similar, and the result has been a sector that has been very disciplined in terms of capex spending on new projects. Adjusted for inflation, capex spending by listed mining companies remains stuck at 2009 levels.

Chart 1: Global real capital expenditure by listed general mining companies

Source: LSEG Datastream

When commodity demand does decisively turn, supply shortages could well be the order of the day. BHP’s bid is a powerful signal that the mining houses themselves are starting to position their businesses for such an outcome. Investors are starting to take note.

The biggest copper producing country by far is Chile, which produces as much as number two and three, Peru and the DRC, combined. But mining production volumes in Chile have barely grown over the past decade. Elsewhere in the world, it is also slow going, less than 2% per year according to the International Copper Study Group.

The industry was particularly spooked last year when protests against a copper mine in Panama – one of the largest in the world – led to the government withdrawing the licence of its Canadian operator, First Quantum. One of the factors behind the unhappiness of the Panamanians is simply that people don’t like mines in their backyards. This is one of the reasons why it can take years to get all the necessary approvals.

None of the above is to suggest that it will be a straight line up for copper or any metals related to the green transition. Market participants have long known copper or “Dr Copper” for its ability to diagnose the health of the global economy. Since copper is used almost exclusively in industrial applications, it is a useful cyclical barometer. In the short term it could still come under pressure from overcapacity in China, the leading smelter of the metal, for instance. However, short-term price fluctuations are not the story here, the long-term outlook is. While the copper price is already near record levels in nominal terms, adjusting it for inflation shows that it is not historically stretched by any means.

Click here to read more...