They call it “Big Data”

Big data is generally defined as large amounts of raw data – structured or not – that can be mined for information that may reveal certain trends and patterns. While this is important for all industries, it is particularly important in the financial services industry where massive amounts of data are gathered from clients on a daily basis. Without the ability to process and analyse this data from its raw form to draw out insights and patterns, there can be little value-add towards product innovation, service enhancement and the ability to cross-sell across business segments.

Globally, financial services organisations are still at various stages of making serious in-roads with big data. Understandably, global banks’ attentions have been diverted between achieving adequate capitalisation and driving growth. Further to this, effective big data strategies may be expensive to implement and as a result, both big data implementation and the subsequent realisation of benefits thereof have been pedestrian. That being said, stakeholders continue to debate big data strategies, on-board providers, and implement available bolt-on solutions as far as possible.

For now, financial institutions are focused on achieving three high level outcomes when it comes to big data:

1) Improving customer intelligence;

2) Reducing risk; and

3) Meeting regulatory objectives.

As with global banks, most large multinational institutions have been battling to meet these outcomes while Fintech start-ups and some mid-tier, regional banks have had more success.

Domestically, financial services company margins have not been declining as much from a low –yield environment as from increased competition with each other, Fintech startups, and global players like GAAF (Google, Amazon, Apple and Facebook). To compete more effectively banks and insurers are looking towards product and service innovations as drivers of growth and market share. Local players have already started employing big data to improve the cross-sell ratio between different product ranges across various divisions.

Local banks have been employing a variety of strategies in this space

Nedbank recently became the topic of an MIT Sloane case study on how data can be used by a bank to improve customer relationships. The company pioneered a commercial data service called Market Edge which packages credit and debit card information with geolocation, demographic and other transactional data to gain insight into customer behavior. Besides successfully commercialising and monetising the product, the bank has been able to gain new clients and retain existing clients on the back of its implementation.

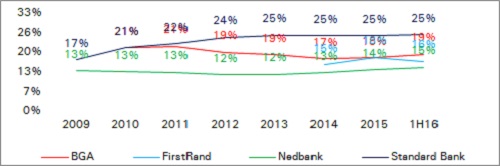

IT spend as a % of total spend for the big four banks

Pre-2014 FSR data not directly comparable with the peer group

Source: Deutsche Bank, Company financials, Ashburton

Over the last few years, Standard Bank has taken significant cost strain in upgrading its legacy IT system. That being said, it would be significantly easier to integrate new add-on technology onto brand new infrastructure.

In FirstRand, the focus has been on integrating the global objectives of reducing risk and meeting regulatory objectives. This has been done by optimising big data to better understand the life cycles of clients in order to drive the right kind of behaviour and propose the right products to meet the clients’ needs and retain them.

Outside of the banking space, Santam and Discovery use predictive analytics to manage claims ratios, and Transaction Capital’s SA Taxi has been making use of telematics to monitor customer behavior patterns to optimise credit origination, collections, insurance and repossessions.

Given that so many players in the financial services space are already taking advantage of big data, the opportunity cost of not investing in this concept now could be significant, especially since we anticipate the implementation and use thereof to evolve further over time.

We highlight a few interesting emerging trends:

• The Internet-of-Things (IoT): The internet has shifted into everyday life through the integration of everyday objects (e.g. your coffee machine or watch) with the internet. In financial services, firms could embed their services into various client touch points, seeking to offer advice or products in real-time.

• Robo-advice: Portfolio management and advisor applications can leverage off the core of big data platforms.

• Fraud and risk management through robotics: Real-time analysis and alerts.

• Regulatory and legal compliance: Platforms will be able to achieve the integration of traditional/legacy data stores with new information to meet volume and speed requirements, and provide additional detail.

The low-yield global environment and highly competitive domestic space has almost forced the industry to seek new ways of supporting margins and profitability, as opposed to the continued, unsustainable method of merely taking costs out of the system. This is a clever strategy and the expectation would be that leading firms in the big data and digital space should attract a premium rating in the market. For this strategy to really work, however, information technology (IT) spend needs to be focused on more sophisticated infrastructure and skills development needs to take priority.