Moody’s admitted structural problems in SA

Moody’s downgraded the outlook on South Africa’s credit rating from stable to negative to flag fiscal and economic risks. FAnews spoke to Sanisha Packirisamy, Economist at Momentum Investments and Reza Hendrickse, Portfolio Manager at PPS Investments, about the downgrade and what the likelihood of South Africa facing junk status is.

The challenges the government faces

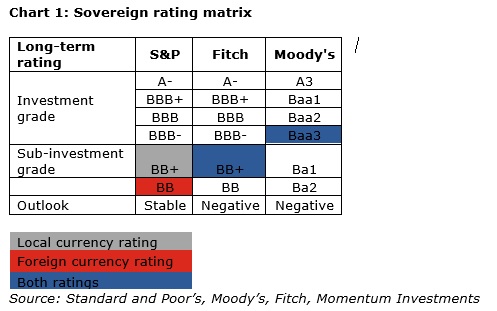

“Close to midnight on 1 November 2019, Moody’s announced its decision to keep South Africa’s credit rating in investment grade at Baa3, but flagged rising fiscal and economic risks to the sovereign by lowering the outlook on the country’s rating from stable to negative (see chart 1),” said Packirisamy.

The statement read that its decision “reflects the material risk that the government will not succeed in arresting the deterioration of its finances through a revival in economic growth and fiscal consolidation measures. The challenges the government faces are evident in the continued deterioration in South Africa’s trend in growth and public debt burden, despite ongoing policy responses.”

The fiscal strategy

“Moody’s admitted structural problems in South Africa, including high unemployment and income inequality among other social problems, are posing a greater risk (than previously assessed) to government’s ability to enhance trend growth prospects and adhere to fiscal consolidation plans,” added Packirisamy.

“Moody’s warned the medium-term budget policy statement did not yet represent a developed, credible fiscal strategy. While Treasury explained R150 billion additional cost saving measures were needed to balance the primary budget (main budget net of interest) net of support to Eskom by fiscal year 2022, this is largely premised on containing the public sector wage bill,” continued Packirisamy.

“In Momentum Investments’ opinion, this remains a challenging task. Treasury has acknowledged that the average government wage bill rose by 66% in the last ten years even after adjusting for inflation. Moreover, government confessed that expected savings on compensation announced in the 2019 national budget had been reversed. These measures included early retirement without penalties which were anticipated to generate savings of R12 billion,” said Packirisamy.

Given the further deterioration in the medium-term budget policy statement outlook, Hendrickse believes the odds of South Africa reaching an unsustainably high level of public debt have increased. “We therefore share Moody’s concerns expressed in their latest credit assessment. Moody’s have in fact been behind the curve in taking a more negative stance on the progressive deterioration of South Africa’s public finances. It has been two years since S&P became the second rating agency to rate South Africa as sub-investment grade. South Africa is in a difficult position, needing both higher growth and fiscal austerity to reverse course in favour of improvement. Given that the two are mutually exclusive, and require politically unpopular decisions, combined with our fiscal track record in recent years, a Moody’s downgrade is our base-case expectation.”

Junk status in due course

“A reversal in the lowering of the outlook from stable to negative would depend on South Africa’s success in stabilising the country’s debt ratios in the medium term through additional cuts to expenditure, an improvement in tax compliance and higher potential growth. Marked progress in eradicating corruption and improving the poor financial and operational standing of South Africa’s state-owned enterprises would further need to be seen for an improvement in South Africa’s rating to materialise,” emphasised Packirisamy.

“In contrast, a further erosion of South Africa’s fiscal and economic strength or signs of lower resilience to countering external financing shocks could exert additional negative pressure on the country’s rating. Moody’s noted the importance of the February 2020 national budget for further clarity on cost-containment measures contributing to its broader fiscal consolidation strategy,” highlighted Packirisamy.

“According to SBG Securities, there are no rigid timelines for Moody’s to resolve a negative rating outlook on a sovereign. Around a third of issuers have been downgraded by Moody’s within 18 months of being assigned a negative outlook. In Momentum Investments’ view, if no fiscal recourse and decisive government action are evident by the time of the 2020 budget, Moody’s will likely follow with a ratings downgrade to junk status in due course,” concluded Packirisamy.

Investment grade in the first half of 2020

“Although our initial view was that there would be roughly a 12-month period between a Moody’s negative outlook change and a downgrade to sub-investment grade, we have effectively been issued an ultimatum,” said Hendrickse.

“Moody’s is expecting to see a credible fiscal strategy to contain the rise in debt in the February National Budget Speech, or risk losing our investment grade rating. Given the magnitude of the task, which has arguably become even more demanding in recent years, and the fact that every Budget speech in recent years has predicted a worse than expected outlook, we consider the odds of a first half downgrade to be more likely than not,” added Hendrickse.

“It is highly likely for South Africa to face junk status. Two of the three major rating agencies already rate South Africa as sub-investment grade. Should Moody’s downgrade South Africa as we expect them to, then the country will officially be considered junk status. This will have an immediate impact on our eligibility in certain global bond indices and will affect our sovereign cost of borrowing. The important point though is investors are already being compensated for the risk of downgrade. Consequently, the decision to hold South Africa bonds is partly based on one’s assessment of whether government is committed to stabilising SA debt or whether things will continue to deteriorate,” concluded Hendrickse.

Writer’s Thoughts:

Dipping into junk status is bad enough but spending a sustained period in that investment grade category will be catastrophic for the country. We are our own worst enemy at the moment. We may avoid junk status, but for how long? Please comment below, interact with us on Twitter at @fanews_online or email me your thoughts [email protected].

Comments