The cost of delay: Sanlam Benchmark reveals South Africans plan too late

The 45th Sanlam Benchmark Survey, released today, has found that South Africans believe retirement planning should begin around age 35, however on average they seek financial advice just 20 months before retiring.

The Sanlam Benchmark is South Africa’s most referenced and comprehensive retirement industry research. The 2026 study reveals a striking disconnect between intention and action. While South Africans believe their mid-30s are the right time to begin planning for retirement, the survey shows that, on average, retirement fund members only start engaging with their retirement fund 3.4 years prior to stopping work. Additionally, only 57% received professional advice about retirement.

By then, many of the decisions that shape retirement outcomes have already been made.

Kanyisa Mkhize, Chief Executive Officer of Sanlam Corporate says retirement confidence is not built in the final years before retirement. It is built over decades of a working lifetime through the decisions people make along the way: preserving their savings when they change jobs, increasing contributions where possible and managing debt. “Retirement planning also does not stop when someone leaves work. The first few years after retirement are critical, because that is when a lifetime of savings is tested against the reality of living costs, healthcare needs and longevity.”

Mkhize says, “The Sanlam Benchmark tells us that people understand when they should start planning, but the reality is that many are making retirement decisions in a very difficult economic environment. As an industry, we must recognise the financial pressure many members are under. We need to work together with employers and advisers to help members plan earlier, access better advice, preserve more of their savings and increase contributions where they can.”

The reality before retirement... and the reality after

The survey reveals two very different pictures of retirement.

• Before retirement, many South Africans are still trying to build financial security while navigating job moves, rising living costs and growing debt.

• After retirement, decisions made early in a career, and along its lifespan, become impossible to undo.

Pensioners who take a cash lump sum at retirement now deplete it within an average of just 14.6 months - a decline from the 30 months reported between 2011 and 2016. Within four to five years of retiring, half can no longer maintain their pre-retirement standard of living, one in three experience financial strain and 47% carry debt into retirement.

Healthcare has become another defining pressure. While 33% of retirees remain on the same level of private medical cover, 44% have either downgraded their cover or abandoned private cover entirely and now rely on the state.

South Africans are changing - and retirement planning needs to change with them

This year's Benchmark also challenges many of the assumptions that have traditionally shaped retirement advice.

Younger South Africans, often viewed as risk-takers, are becoming increasingly conservative in their financial outlook. Nearly nine in ten say they would rather have guaranteed retirement income than potentially higher investment returns. At the same time, many are navigating career interruptions, debt and short-term financial pressure that make long-term saving difficult.

Generation X (ages 46 – 61), traditionally seen as being in their peak earning years, is carrying some of the country's greatest financial strain. Many are supporting both children and aging parents while approaching retirement themselves, often with significant debt.

Meanwhile, retirement itself is being redefined. Far from slowing down, today's retirees are increasingly digitally connected, financially active and economically engaged. Sixty percent supplement their retirement income through other sources (compared to 47% in 2024), while more than 90% regularly use digital platforms and online banking.

"The old assumptions about age no longer hold," says Mkhize. "Young people are looking for certainty, people in mid-life are under unprecedented financial pressure, and many retirees continue working because they need to. Retirement planning has to reflect the way South Africans actually live today, not the way they lived twenty years ago."

A retirement system transformed - and new opportunities remain

The Benchmark reflects on how dramatically South Africa's retirement landscape has evolved over the past two decades.

The industry has consolidated significantly, with fewer but stronger stand-alone retirement funds, substantially lower administration costs and improved governance. The introduction of the Two-Pot System has also transformed how members engage with their retirement savings. Eighty-four percent of standalone funds and 80% of umbrella funds report increased member engagement since its implementation.

Anna Siwiak, Head: Product Development at Sanlam Umbrella Solutions, says increased member engagement is encouraging because it creates an opportunity for the industry to work together and make a real impact on retirement outcomes. "People are paying more attention to their retirement savings than they have in years. Our challenge now is to help them use those moments of engagement to make better long-term decisions - not only when they need to access money, but throughout their working lives."

One of the clearest opportunities lies in contribution levels.

Average contributions in umbrella funds currently sit at 14.09% of pensionable salary (8.00% from employers and 6.09% from members), compared with 17.44% in standalone funds (10.69% from employers and 6.75% from members) - both well below the maximum tax deductible contribution level of 27.5% of taxable income. While few people can immediately increase contributions to that level, Siwiak suggests that gradually increasing retirement savings by one or two percentage points as salaries grow can significantly improve retirement outcomes over time.

“Affording even small increases in contributions can be a challenge, especially in today’s economic climate. That is why a robust retirement strategy, anchored in career-long financial advice, is so critical. Advice is not a one-off event at retirement - it is the ongoing guidance that helps members preserve savings when they change jobs, manage debt before it spirals, and make confident choices about healthcare and longevity. When advice is embedded across the member journey, even modest contribution increases become part of a stronger, more resilient financial plan,” says Siwiak.

The research also highlights preservation as one of the biggest opportunities to improve retirement outcomes. Although 26% of funds and 19% of umbrella sub funds have seen preservation improve since the Two Pot system was introduced, the majority remain concerned that members still withdraw rather than preserve their savings when changing jobs.

Siwiak adds that when changing jobs, members often receive withdrawal forms instead of meaningful financial guidance at one of the most important financial decision points of their lives.

Confidence through the ages

This year's Benchmark Survey is built around the theme Confidence Through the Ages.

Its central finding is simple: retirement confidence cannot be built during the last few years of a career, nor can it end on the day someone retires. It is created - and protected - through decisions made across an entire lifetime.

"The conversation about retirement should begin around age 35 because that's when time is still your greatest asset," says Mkhize. "But it shouldn't stop at retirement either. The first years of retirement are just as important, because that's when decades of planning are put to the test."

The study surveyed 76 standalone retirement funds, 130 umbrella fund employers, 30 pensioners who retired four to five years ago, 600 consumers made up of 200 employed, 200 approaching retirement and 200 living in retirement. It comprised two studies conducted by research houses BRDC and Alltold.

_____________________________________________________________________________________________________________________________________________

Sanlam Benchmark Survey: When a ‘small bet’ becomes a big problem

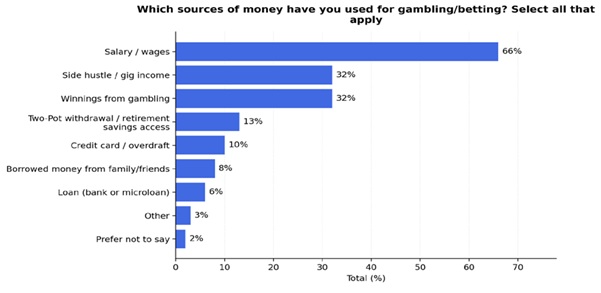

In South Africa, gambling is often spoken about as harmless background noise - a Lotto ticket bought in passing, a quick weekend bet, a small indulgence in a difficult economy. But that framing is becoming harder to defend according to the 2026 Sanlam Benchmark Survey which found 50% of respondents in the online consumer portion of the study had spent money on gambling, betting or lottery activities in the last three months. With 66% using salary and wages as the source of funds.

Nzwa Shoniwa, Managing Executive: Sanlam Umbrella Solutions, says this suggests that for many people, gambling is no longer simply about entertainment. “It is increasingly bound up with financial pressure, short-term coping and the trade-off between immediate relief and long-term security.”

The 2026 Sanlam Benchmark - the country’s most comprehensive retirement fund industry research - surveyed 76 standalone funds, 130 umbrella fund employers, 30 pensioners who retired four to five years ago, and 600 consumers who are nearing or in retirement.

Shoniwa says the Benchmark found participation to be notably higher among those still economically active, especially for the more frequent, more digital and potentially riskier forms of gambling. “Retirees are not untouched, but the intensity is lower. The bigger risk is the pre-retirement habit that chips away at financial resilience over time.”

Entertainment on the surface, financial pressure underneath

The majority of respondents, 58%, still describe gambling as entertainment. But that headline number does not tell the full story. The survey shows that 38% gamble to generate additional income, while others cite stress relief or trying to recover losses. That shifts the picture considerably.

Among working South Africans, gambling is more closely tied to cash-flow pressure. Among retirees, it is more often seen as a possible income top-up. In both cases, gambling starts to move away from recreation and closer to coping.

The digital shift matters

Lotto and scratch cards still dominate, with roughly 72% of those who gamble saying they spend money there. But the bigger shift is happening elsewhere. Online sports betting and casino gambling now account for more than a third of activity each. That matters because these formats make repeated spending easier, quicker and less visible. Retirees tend to stay closer to Lotto-style play. Working South Africans are more likely to be in the higher-frequency online space, where small, regular spending can quietly crowd out saving over time.

The frequency data reinforces the point. The most common pattern is gambling a few times a month (33%), with weekly or near-weekly participation also significant among people who are not yet retired. In a low-savings environment, modest but repeated spending can do real damage over time.

This frequency dynamic is critical. As the report notes, the real financial risk lies in “small regular leaks”, modest but consistent spending that gradually crowds out savings. In an environment where many households already face budget pressure, repeated discretionary spend, even at low levels, can accumulate into meaningful long-term financial erosion.

Gambling is not being funded with spare cash

Perhaps the most sobering finding is where the money comes from. In many cases, gambling is not funded from “extra” income. It comes straight out of salary or wages, which 66% of respondents say they use to gamble, with some also drawing on side-hustle income, credit, borrowed money and even two-pot retirement withdrawals. That should immediately reframe the conversation: this is not only leisure spend, but money that might otherwise support financial resilience.

Financial stress is the backdrop

These behaviours do not happen in isolation. They sit inside a much wider story of financial strain. In last year’s Benchmark survey, more than 80% of respondents said they were experiencing financial stress. That pressure does not only affect household budgets.

It also affects mental health, decision-making and workplace wellbeing.

That is why this should matter beyond the gambling conversation. Persistent financial anxiety creates conditions in which short-term choices can override long-term interests. It also helps explain why employers are seeing rising absenteeism linked to stress, anxiety and mental-health strain in the benchmark findings over the past two years.

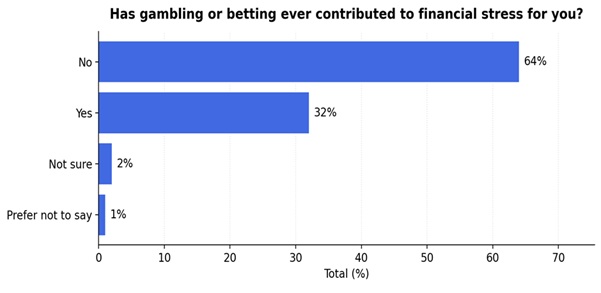

A full 32% of respondents say gambling has contributed to financial stress. That is a sizeable minority, and in some cases an early warning sign of deeper financial vulnerability.

- 32% of respondents say gambling has contributed to financial stress.

Not just a gambling story: Financial strain becoming a workplace issue

Shoniwa believes the findings should prompt a broader rethink by employers, funds, advisers and policymakers. “The bigger issue here is not morality, but financial behaviour under pressure.”

The Sanlam Benchmark 2026 findings suggest that gambling is becoming one of the ways financial strain shows up in everyday life, with implications not only for savings and retirement readiness, but also for mental health, workplace performance and household stability. That makes this a stronger case for holistic employee wellbeing solutions, especially those that bring together financial education, mental health support and accessible employee assistance programmes.

He says investing in employee wellbeing should not be seen as a soft benefit or a peripheral HR intervention. In a low-savings, high-stress environment, it is part of protecting the health of the workforce and, by extension, the resilience of the economy.

“When employees have access to support that helps them manage stress, debt, anxiety and difficult financial choices earlier, employers are not only investing in the people who work for them. They are contributing to a more financially stable, mentally healthier and ultimately more productive society. That is the broader lesson in the data: financial vulnerability does not stay confined to the individual. It carries consequences that ripple outward into workplaces, families and the country’s long-term wellbeing,” Shoniwa says.