Life insurance confidence weakens but remains nevertheless robust

A survey released by EY today indicates that life insurance confidence slipped in the third quarter of 2015. This was despite stronger profits growth and unfavourable domestic economic pressures.

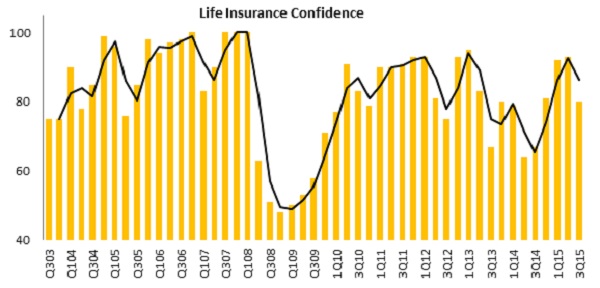

Overall confidence slowed from 93 index points in the second quarter of 2015, to 80 currently, in line with its long term average.

This is the 49th quarterly survey conducted to measure confidence in the banking industry, and the research is conducted by the Bureau for Economic Research in Stellenbosch.

Malcolm Rapson, EY’s Africa Insurance Leader at EY says, “Confidence levels in life insurance remain the most resilient across the financial services sector, despite the slip in the third quarter. Amongst financial services companies, life insurers have been the most immune to the impact of emerging markets turmoil experienced in the third quarter. This is vastly different to asset managers, who were visibly impacted by weak commodity prices and portfolio flows, which noticeably impacted their earnings and confidence levels.”

Thus far, he adds, “Subdued local economic conditions do not appear to have dampened the financial metrics of life insurers. For one thing, profits growth ticked up in the third quarter, on the back of stronger premiums.

During the recent financial reporting cycle, life insurers mostly reported single digit profit growth as a result of slower premiums and investment income flows.”

The survey findings indicate that circumstances may have picked up for the life insurance sector in the third quarter, despite weaker confidence levels. All of premium income, investment income and fees appear stronger than they were in the first half of 2015. Rapson points out that the only unfavourable metrics in the third quarter were surrenders, which rose sharply. “We think this could well reflect consumer pressure as a result of which they select not to extend policies and are cashing out instead. On the other hand, lapse trends remain favourable, with overall lapses shrinking for the fourth consecutive quarter.”

Other findings include:

- A sharp slowing in risk premiums, and a continued shrinking pool of investment related premiums.

- A continued reduction in the headcount, coupled with a higher sales force headcount.

- Sustained strong growth in operating expenses.

- A weakening in the value of new business written.

Rapson comments, “Weakening values in new business is symptomatic of less favourable economic and industry specific circumstances. It indicates that life insurers may be struggling to maintain profitability, which in turn suggests that their margins may come under pressure through the rest of 2015.”

He also points out that declining investment premiums have been a feature of the life insurance sector for a while now. Greater competition, particularly from financial services companies with widespread distribution channels, means that life insurers are increasingly faced with a wider range of investment products and suppliers that they have to compete with. Rapson adds, “Insurers have invested in building their reach and continue to do so, as the market becomes more sought after. But once again, this comes at a price, as margins are invariably pressured.”

In short, the life insurance sector remains well positioned to manage the current weak domestic market. However, it is difficult to know whether the positive turnaround in premium income will continue into the next quarter. Rapson points out that because investment income is a major component of life insurers’ earnings, and these came under pressure in the first half of the year, life insurers will likely start to feel the same impact of the very slow growth economy that other financial services companies are already grappling with.