Life insurance confidence rises after a weak third quarter

22 January 2014 | Surveys, Reports and Ratings | General | Malcolm Rapson, EY

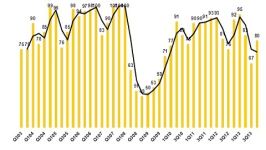

EY today reports that life insurance confidence rose in the fourth quarter, following two consecutive quarters of falling confidence in the prior two quarters. Confidence levels rose from 67 index points in the third quarter of 2013 to 80 in the last quarter. Life insurance confidence is no longer the strongest in the financial services sector, which is now led by Asset Management.

This is the 42nd quarterly survey measuring confidence in the life insurance industry. The research is conducted by the Bureau for Economic Research in Stellenbosch.

Life Insurance confidence rose in 4Q13

The survey, which covers a broad range of financial services companies, found that overall financial services confidence was unchanged in the fourth quarter, with stronger asset management confidence offsetting weaker investment banking confidence.

Malcolm Rapson, EY’s Africa Insurance Sector Leader points out that the stronger confidence seems to be aligned to higher premium growth trends. "We notice that in the third quarter, confidence fell on the back of much weaker premium growth. In the fourth quarter, confidence rose once more, again in tandem with higher premium growth although premium growth did not reach the same levels as in the first and second quarters of 2013.”

He adds, "Whilst insurers also earn a considerable portion of their income from investment returns, premium income is one key indicator of the underlying health of the business. In the third quarter, new business premiums were rather weak. However, overall premium growth was in line with second quarter levels, after slowing in the third quarter.”

He continues, "Increasingly, life insurers are writing larger volumes of risk related policies, the core of their business, whilst investment related business has slowed somewhat over the longer term. This is in line with greater competition in the traditional savings products market and the impact of lower interest rates, and the life insurance industry has re-energised efforts in the profitable risk market.”

‘Even so’, he adds, "There was a drop in risk based product profitability in the last quarter of 2013. However, this follows a few consecutive years of strong risk profitability growth, and it is difficult to read from a single quarter whether risk profitability will remain under pressure going into 2014.”

Other survey findings include:

• Unfavourable lapse rate developments in the fourth quarter

• Sharply higher surrenders, as measured by the value of paid-up policies

• Contracting investment income growth, for the first time in over two years

• A shrinking headcount, which is helping keep cost growth under control

• Sustained strong profits growth through 2013

Rapson points out that the slower investment income was unexpected. "Generally, stronger stock markets support stronger investment returns, but this pattern was not observed in the last quarter of 2013. Whilst investment returns shrunk marginally, this follows a record three years of growth in investment income. Overall, investment income for the year will still be considerably ahead of 2012 levels, given the overall increases reported in the first three quarters.”

Profits continued to grow strongly in the fourth quarter, aided by stronger premium growth and sharply improving expense trends. Comments Rapson, "Profits grew at their strongest pace in over two years, despite lower investment income. We think this follows a sustained effort on the part of life companies to improve efficiencies and manage their cost base more carefully. These initiatives typically have a considerable time lag before the results are felt. Life companies have been shrinking their in-house employee base for over two years now, and this is undoubtedly benefitting their bottom-line profits growth. The positive market returns have also contributed significantly in improved results.”

Rapson concludes, "Overall, the life insurance sector is in good health, although there are some worrying signs, especially the up-tick in lapse rates, and sharply lower new business premiums. However, the uptick in lapses and terminations follows a positive trend of five quarters of declining lapses and terminations, so it will be interesting to see if the last quarter uptick continues into 2014. Life insurers reported consistent profits growth through 2013, and for the most part, this was supported by strong growth in both premium and investment income. This bodes well for the upcoming financial reporting season, and we anticipate continued strong rises in profits from most life companies.”