Life Insurance confidence remains strong, albeit weaker

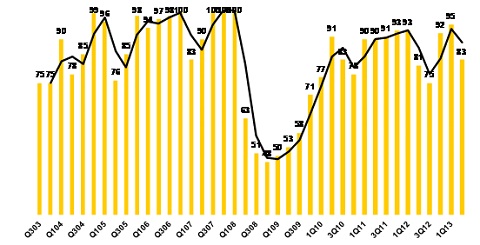

In a quarterly survey released today, EY reports that life insurance confidence remained relatively strong in the second quarter, although it did fall somewhat from first quarter levels. Confidence reading fell from 95 index points in the first quarter of

The sustained strong confidence was measured, despite visible evidence of a slowing economy, and less buoyant business confidence across South Africa. Tim Rutherford, Insurance sector spokesperson at EY comments that ‘there don’t appear to be any change to life insurers’ business prospects just yet. Unlike the banking sector, where lending growth has slowed and thereby resulted in much weaker confidence, life insurers are still reporting strong premium growth.’

This is the 40th quarterly survey measuring confidence in the life insurance industry. The research is conducted by the Bureau for Economic Research in Stellenbosch.

Life Insurance confidence levels remained strong in 1Q13

The survey, which covers a broad range of financial services companies, found that financial services confidence fell overall in the second quarter, led by retail banks, who are faced with weak lending prospects and concerns about rising bad debts. Asset management confidence fell more moderately, although investor sentiment remained weak through the period.’

Rutherford comments on life insurers’ continued strong confidence; ‘ recent quarterly updates from the life insurance sector indicates that the first quarter of 2013 was generally good. Our latest index results show that these buoyant conditions held into the second quarter of the year. This was led by sustained strong premium growth, coupled with visibly stronger investment income. Together, these two metrics provide for a strongly supportive business environment, despite the much weaker GDP growth numbers and rising labour strife through the quarter.’

The survey further found that bottom line profits continue to grow soundly for the industry, driven not only by the favourable inflows, but also by keeping a firm grip on lapses and surrenders. Rutherford points out that ‘ life insurers have more recently improved the quality of the business written. This plays a key role in driving earnings, as lapses can consume major management time in addressing and correcting. Lapse rates are less of a problem for the South African insurance market than they have been for a while.’

In addition to the benign lapses, surrenders also slowed during the quarter. Says Rutherford, ‘ again, this can be, and has been, a major drain on life insurers’ net client flows, as high surrender levels can easily offset new business written. This is something that all life companies have focused on for a long time, and the latest quarter’s results indicate that those efforts are resulting in slowing surrender levels.’ In addition, the expectation is that further improvements are likely going into the second half of the year.

Other survey findings include:

• Risk based business is growing considerably faster than investment product business.

• The strong premium growth came about despite a rationalized agent force.

• The focus on improving efficiencies across the industry has led to continued shrinking in the headcount – both sales and administration focused roles.

• Continued improvements in the value of new business written, indicating that margins are rising.

The gap between new risk premiums and investment premiums has widened in the last two years, with new risk based business growing three times faster than what investment based inflows are. Rutherford comments as follows ‘Life insurers have undoubtedly focused their efforts on risk based products, particularly after weaker results in the previous year,. This is strongly supporting the margin gains insurers are making, as evidenced by rising new business values.’

Rutherford concludes ‘despite the strong confidence, economic growth remains weak, and this is likely to pressure growth prospects further down the line. On the other hand, there is still a strong lower-income segment to tap into, where insurance penetration rates remain low. Life companies are all strongly focused on growing the uptake of insurance products in this market, and that may continue to provide the strong growth they have experienced in the first half of 2013.’