Households “wealthier” now than in 2016

The Momentum Unisa Wealth Report Q1 shows that while households’ net wealth has increased since last quarter, it’s still lower compared to a year ago.

The real value of South African households’ net wealth increased slightly in the first quarter of 2017 (Q1 2017) compared to Q4 2016. Put differently, the combined real net value of all the goods households own (including residential property) and the money they saved and invested increased marginally in Q1 207 compared to Q4 2016.

However, the real value of households’ net wealth was lower compared to a year ago (Q1 2016). In fact, it was at the same level as three years ago (Q1 2014). This means that households lost three years of wealth accumulation. The consequences of this loss of real net wealth are far reaching, negatively affecting the economy and every household in the country.

Shrinking, or slow-growing real household net wealth, results in less confidence and more financially vulnerable consumers. This in turn causes slower economic growth and job creation, while it also slows the pace of transformation. It also means that households’ standard of living will be lower than it could have been during their working life and in retirement. It also inhibits their ability to improve their financial wellness.

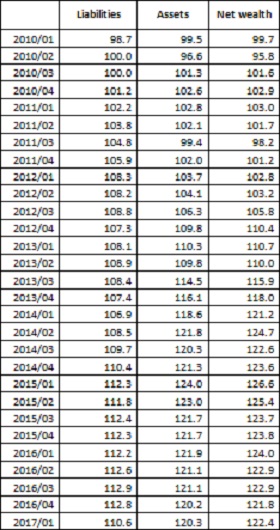

The Momentum/Unisa Household Wealth Index for Q1 2017 shows that the real value of household net wealth increased marginally in Q1 2017 compared to Q4 2016 – to R6 994.8 billion from R6 959.8 billion. This represents a 2.0% growth rate when measured at an annualised quarter to quarter growth basis. However, it is 1.3% or R91.3 billion lower than a year ago.

The small quarterly increase occurred for lots of right and some “wrong” reasons. On a macro level the right reason is because the real value of households’ assets increased to R8 370.2 billion - from R8 362.8 billion in Q4 2016. This is 0.4% higher than in Q4 2016. The main reason for the increase in the real value of household assets can be attributed to a better performance of their financial assets, which mainly is invested in retirement funds. For instance, the real JSE All Share Index increased by an annualised quarter to quarter growth rate of 2.1% between Q4 2016 and Q1 2017.

However, despite the quarterly increase, the real value of household assets was still R111.5 billion lower than a year ago (Q1 2016) - and roughly at the same level as in Q3 2014.

Contrastingly to assets, the real value of households’ liabilities – which should be subtracted from their assets to obtain their net wealth – declined in Q1 2017 compared to both a quarter ago (Q4 2016) and a year before (Q1 2016). This indicates that households are reducing the extent of their indebtedness, which is positive for wealth accumulation. In this respect the ratio of household liabilities to their disposable income shows a decline to 73.9% in Q1 2017 from above 75% in Q4 2016 and almost 76% in Q1 2016.

Households’ deleveraging has been ongoing for almost a decade as this ratio was around 90% in 2008. The consequences of the higher indebtedness continue to affect households’ cash flow as they allocate a larger share of their income towards the repayment of debt. This contributed to a slowing in the uptake of new credit and to the lower debt to disposable income ratio.

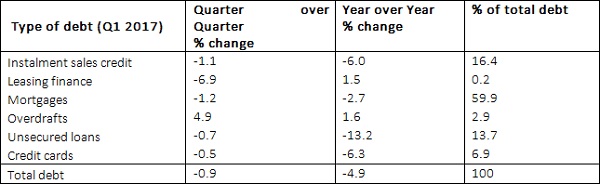

The uptake of almost all types of credit not only slowed, but actually contracted in real terms. The table below shows the quarterly and year-over-year changes in the different types of household credit. There was a strong pull back in the real value of outstanding unsecured-, credit card- and instalment sales debt, while real mortgages also shrank.

When debt for the purpose of accumulating assets shrinks – as is the case with mortgages to acquire residential property - it indicates the extent of financial pressure on consumers. It is also one of the “wrong reasons” for the quarterly increase in households’ real net wealth.

Change in the real outstanding value of different types of household credit

Sources: South African Reserve Bank. Momentum Client Engagement Solutions

Furthermore, when shrinking net wealth occurs despite shrinking debt – as shown by the year over year indicators - it indicates that household assets are not performing well in generating returns for households. For assets to generate wealth for households the economy must be performing and households need to engage in the right activities.

However, the economy has entered a technical recession in Q1 2017 due to among others a lack of confidence by private business and continual uncertainty caused by international and domestic political events. At the same time households have not been playing their part to improve their asset accumulation position. The majority of households are still not saving sufficiently for retirement and they also don’t do adequate budgeting and financial planning.

As long as such confidence is absent and households don’t play their part, the accumulation of wealth for purposes of a better life will remain an unrealised dream for most households.

Indices of real household liabilities, assets and net wealth