EY’s life insurer confidence falls only moderately, despite weak economy

A survey released by EY today indicates that life confidence fell in the fourth quarter of 2015. The fall in confidence was moderate, falling eight index points.

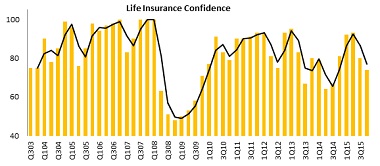

This left life insurance confidence at 74 index points in the fourth quarter of 2015, from 82 in the previous quarter. Long term average confidence is 82 index points, indicating that confidence levels are currently slightly weaker than average.

Life confidence levels

This is the 50th quarterly survey conducted to measure confidence in the life insurance industry, and the research is conducted by the Bureau for Economic Research in Stellenbosch.

Malcolm Rapson, EY’s Africa Insurance Leader says, “The weaker confidence levels are in line with weakening economic fundamentals. Confidence levels are down across most, if not all industries, and insurers face similar challenges.”

He adds that, “Life insurer confidence tends to still be relatively strong, certainly stronger than the other financial services segments. Even with the lower confidence in the fourth quarter, life insurers seem to be more optimistic about the outlook than other sectors. Only investment banking confidence is stronger, and even then, not by a significant margin.”

The survey results also indicate that lower confidence was in line with weakening income levels. Both premium and investment income flows were lower in the last quarter of 2015.

Weaker premiums are reflective of weakening employment numbers, with the economy only slowly recovering from a contraction in the second quarter, and with overall growth for 2015 likely to be around 1.5%.

Rapson points out that, “Through the first half of 2015, life insurer confidence was high, despite weakening mining and manufacturing activity, which would have impacted personal market growth. By the second half of the year, though, confidence levels started to fall, as the impact of rising unemployment and flat corporate activity started to impact on business volumes and increased interest rates affected consumers.”

The survey also found that the fourth quarter was the first time in a while where insurers faced declining premiums. Rapson makes the point that premiums last contracted in the life insurance market in 2009 – during the global financial crisis. He adds, “Life insurers have not faced significant premium pressure for the last seven years. This is a new risk for them to manage, and we shall have to see whether this endures into 2016, and how sustained these weaker premiums prove to be.”

Other survey findings include:

• Investment income remains flat.

• New business premiums are under pressure, which may imply that premiums could remain weak into 2016.

• Lapses continue to shrink, a positive sign, which indicates insurers are writing better quality volumes.

• Surrenders also continue to improve, meaning that insurers are holding on to larger sums from maturing policies, another positive for the industry.

• Expense growth remains strong, driven by a strong increase in the sales force.

Rapson believes that the favourable lapse and surrender trends are cushioning the life insurance sector from what could otherwise be even more difficult times. He says, “With flat investment income, and declining premiums, there is no doubt that revenue streams are under pressure. But life insurers have created a buffer in these improving metrics. It is more cost effective for insurers to retain policies on their books, and the improved metrics on these two measures is likely helping sentiment levels across the industry.”

Rapson concludes, “Although times are undoubtedly tough, life insurers still remain largely optimistic. Three out of every four life companies are indicating that despite the difficult economy and great uncertainty, they remain optimistic about the long term outlook. This, perhaps, bodes well for the upcoming financial reporting cycle. We saw earnings growth pressured in the first half of 2015, but overall, growth remained positive. We expect to see some squeeze on these financial metrics in the second half, but for the overall trend to remain positive, albeit at a slower pace.”