Disposable salaries and pensions bounce back strongly in March

Dr Caroline Belrose, head of information services at BankservAfrica.

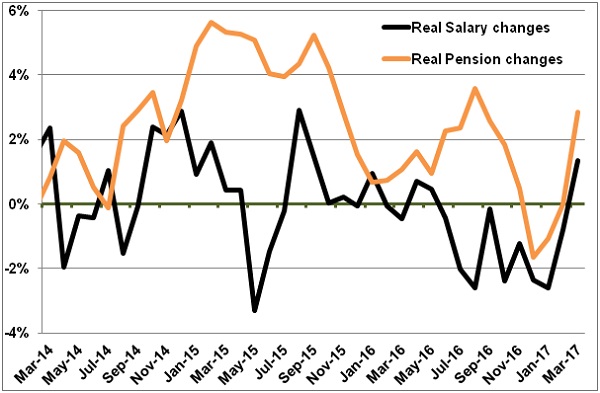

For the first time in 10 months, March reflected a real take-home pay increase above the rate of inflation. BankservAfrica’s latest Disposable Salary Index (BDSI) also showed that March’s take-home pay increase after inflation was the strongest in 18 months with an improvement of 1.3% on a year-on-year basis.

The change in March from the 0.8% decline in February is a very strong indication of the positive growth in take-home salaries. Last month’s data is also a marked improvement from January which experienced a real year-on-year decline of 2.6%. This means that the real bounce over the last three months is nearly 4% - a very positive data trend for employee and consumer spend in the economy.

March’s improvement can be owed to a number of factors including the lower rate of inflation, higher gross salary increases based on last year’s higher inflation and the low year-on-year base in March 2016.

There also seems to be a movement of employees out of the lowest payment level. Those receiving less than R4 000 per month in their bank accounts have averaged just 13.9% of the total amount over the last six months.

This may have to do with less annulment orders following the recent successful court case against debt collectors who were found to be abusing these orders.

Additionally, with real-term household debt declining over the last 40 months – as indicated in the South African Reserve Bank credit data – may also be due to debt collected at firm level and before the payment of salaries into bank accounts on the decline.

Against these factors are the increased personal income taxes and the many employees who are still not getting salary increases in line with inflation.

Should this take-home salary trend continue over time, improved retail sales and general consumer expenditure can be expected.

The average disposable salary of R14 098 in real terms is still someway off from its high in September 2015 where it stood at R14 172. As such, consumers are likely to still feel somewhat restrained in their spending. Further pressure is likely from the recent sovereign credit rating downgrade, which may affect consumer debt confidence levels. Consumers may hold onto the money with the concern that the increased risk will impact them down the line.

Still, the March BDSI data is at least evidence of a green shoot in the South African economy. The dramatic events from the last month may however have a different outcome in the BDSI in the months to come.

Graph 1: After inflation changes in take-home salaries and bankable pensions

Source: BankservAfrica and Economistscoza

Private pensions also improve

Bankable pensions have resumed their upward trend, increasing by 2.8% in real terms to R6 575 per month on average in March 2017. This is the strongest showing since August 2016 in percentage increase terms.

While it is difficult to explain the reason for the increases in private pensions, this may in part be due to pensioners drawing down their pension quicker as there is not much evidence of equity market nor foreign investment growth in Rand terms.

Higher interest rates may be playing a small positive role in the increase in private pensions but even this would not be enough to help increase nominal private pensions increase by 9.1%.

As BankservAfrica has about 80% of all the estimated private pensioners going via their payment system, a steady 4.7% increase in the number of private pensioners was observed. This is the highest increase in the number of private pensioners.

New pensioners are also likely to enter the system with a higher pension as those with defined benefits would have higher salaries than their predecessors and the increase in the number of employees saving for pensions over the last few decades would make for higher payments – at least initially.

The total amount of pensions paid increased by13.9% on a year-on-year basis and in nominal terms.

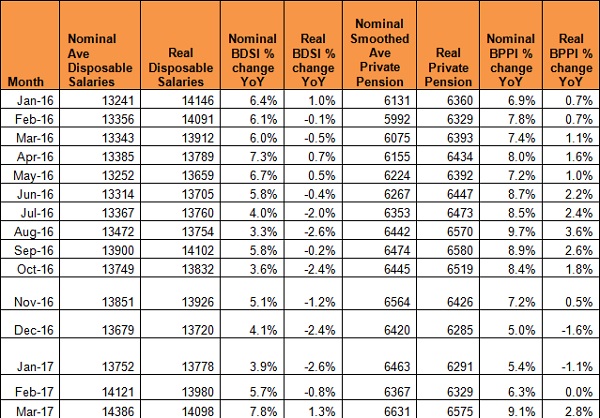

Table of disposable salaries and private pensions

Source: BankservAfrica and Economistscoza