Bank confidence remains stable despite the weak economy

A survey released by EY today indicates that banking confidence once again remained flat in the banking sector in the third quarter of 2014. Investment bank confidence was once again softer, whilst retail bank confidence was marginally stronger.

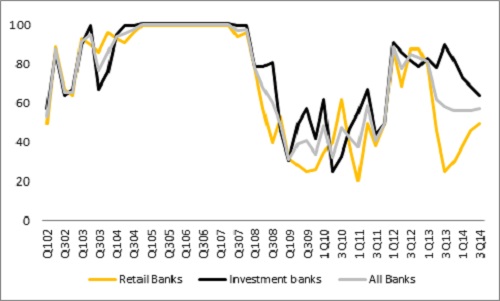

Overall banking confidence remained virtually unchanged, at 57 index points in the third quarter of 2014. This is the fifth consecutive quarter where bank confidence has remained constant, and in a tight range with Retail banking and Investment banking confidence levels continuing to move closer together.

Bank Confidence Index Levels

This is the 51st quarterly survey conducted to measure confidence in the banking industry, and the research is conducted by the Bureau for Economic Research in Stellenbosch.

Comments Emilio Pera, Africa Financial Services Sector Leader at EY, “Bank confidence is quite resilient, considering the weak South African economic environment in which our banks operate. GDP growth was only marginally positive in the first half of the year, and is unlikely to lift meaningfully in the second half of the year.”

He continues, “On the other hand, and despite the weak growth fundamentals, banks recently reported financial results for the first half of 2014. Given the constraints, their results have been remarkable. For the big 4 South African banks, revenue was up in double digit territory, as were profits. Confidence levels through that period are very much where they are now.”

Pera believes that the stronger than expected profits growth is at least partially explained by improving impairment costs. “We notice that impairment charges contracted through the first three quarters of 2014. This is in line with the recent reporting season, where in some cases, the earnings growth was clearly supported by lower impairment charges.”

As a result of lower impairment charges, banks are not tightening credit standards as much as they were in 2013. This is particularly true for retail banks. Whilst there was a marginal tightening in credit standards in the retail banking sector, the level remains benign overall, and in line with the favourable impairment trends.

The survey also found that the confidence gap between investment banks and retail banks is narrowing. Exactly one year back, confidence levels between investment and retail banks was at an all-time high, but we subsequently saw a sharp fall in retail banking confidence levels, whilst Investment banking confidence levels remain strong. This has gradually narrowed, although investment banks still remain more confident than their retail peers.

Pera further adds, “The gap between investment and retail bank confidence has dropped from 65 points a year ago to only 14 points currently. This was driven by both falling investment banking sentiment, and slowly recovering retail bank confidence. We have seen market conditions for investment banks softening in the first half of the year. Although they are growing more rapidly than their retail peers, they nevertheless face tougher competition and less abundant opportunities.”

Other survey findings include:

- Sustained stronger interest income flows in the third quarter, both for retail and investment banks.

- Continued weaker non-interest revenue growth trends.

The higher interest income is likely driven by rising interest rates and moderate advances growth. Pera comments, “The recent bank reporting cycle indicates that interest income was the strongest earnings contributor in the first half. Non-interest revenue, by contrast was in single digit territory. This resonates with banks having less pricing power than they held in the past, due to increased competition coupled with the fact that low GDP growth means that employment growth remains weak, which in turn results in fewer new potential clients coming on stream.”

Pera concludes, “Whilst it appears from a confidence perspective that banks are still not altogether satisfied with prevailing conditions, the recent results reporting season illustrates that banks have nevertheless managed to grow profits well above expectations. Over the longer term, a 1% rise in GDP corresponds to a 5% lift in bank profits. We saw bank profits growing at double that pace in the first half of the year. It remains to be seen whether banks are able to sustain that solid growth if the economy remains weak in the second half of the year.”