Asset Management confidence falls on the back of slower inflows

14 April 2014 | Surveys, Reports and Ratings | General | Chris Sickle, Ernst & Young

A survey released by EY today, indicates that confidence in the asset management industry fell somewhat in the first quarter of 2014, in line with a weaker stock market.

This is the 45th quarterly survey conducted to measure confidence in the asset management industry, and the research is conducted by the Bureau for Economic Research in Stellenbosch.

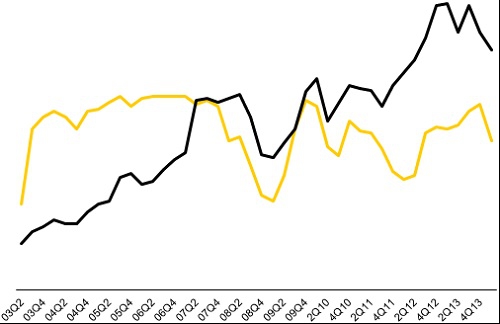

Overall confidence fell from a strong 96 index points in the fourth quarter to 77 currently. The weaker confidence was solely attributable to the sentiment of large managers. Asset manager confidence levels are below long-term average levels, and are no longer the strongest across financial services.

EY Asset Management Confidence JSE ALSI Index

Chris Sickle, Asset Management lead director at EY points out that, "the large asset managers experienced a tough first quarter. Inflows slowed sharply in the first three months of 2014, and it was primarily the large managers who bore the brunt of the slowdown.”

The survey found that small asset manager confidence was stronger, rising from 78 to 85 index points between the last quarter of 2013 and the first quarter of this year. Large manager confidence, by contrast, fell from 100 to 74 points.

Sickle says, "Inflows slowed across both institutional and retail business lines. Unit trust flows were considerably weaker than what they were throughout 2013, whilst on the institutional side, there was a major shift from large fund managers towards the small boutique managers. Private client funds were the only segment to buck the slowing trend, with a slight uptick in inflows. However this uptick is off a low base, and the absolute growth into this segment still remains below both institutional and retail flows.”

Sickle also points out that the first quarter of 2014 was a volatile one. "There was enormous uncertainty about emerging markets, particularly in January. More recently, these concerns appear to have eased, but the withdrawal of foreign investors from emerging markets undoubtedly impacted bond, equity and ultimately currency markets. In addition, local economic growth has remained weak into the first quarter, although this has not yet impacted corporate earnings significantly.”

Other survey findings include:

• Total income, whilst slowing, remained strong for both large and small managers;

• Demand for balanced funds and foreign exposure continues to be high, whilst demand for absolute funds are on the rise; and

• Higher expenses growth, with back office and IT cost growth remaining particularly high.

Sickle further adds, "It is not only asset managers struggling to contain costs. We see that across all financial services markets, there is sustained upward pressure on costs, particularly systems and IT costs. All financial services companies face similar pressures in that regulatory and compliance needs are rising, and with that, comes a greater need to ensure that the new requirements can be met. That often involves system enhancements, or at the very least, system changes, and this can prove costly to effect.”

Sickle concludes, "Asset management confidence remains well correlated with the stock markets, and we saw this relationship continue into 2014. Weak GDP growth has not thus far impacted bottom-line profits for the industry, although slower inflows were clearly visible in the first quarter. We have seen that stock markets and emerging market uncertainties have recently eased, and this may yet again encourage foreigners into the local equity market, which would once again boost confidence for asset managers.”