A false economic dawn: consumers are ‘back in the dumps’ and it’s going to get worse

Momentum/ Unisa CFVI Q2 2018 RESULTS

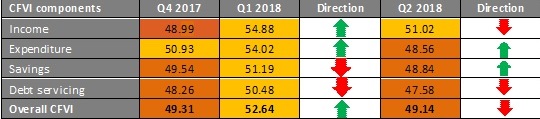

The previous (Q1 2018) Consumer Financial Vulnerability Index (CFVI) release showed that consumers were experiencing lower levels of consumer financial vulnerability during Q1 2018 compared to Q4 2017. This improvement in the financial situations of consumers was ascribed to a ‘new dawn’ brought about by Mr Cyril Ramaphosa being inaugurated as President. The expectation of millions of South Africans at that stage was that the political ‘new dawn’ would quickly translate into an economic ‘new dawn’ characterised by higher gross domestic product (GDP) growth rates, faster job creation, higher investor and business confidence translating into higher economic activity, and lower levels of consumer vulnerability. However, this ‘Ramaphoria’ did not last long and was replaced by “Ramageddon”. This pessimism is also evident from the Q2 2018 CVFI results, which show a deterioration in the income, expenditure, debt, savings, and overall vulnerability scores from Q1 to Q2 2018 (see Table 1). The deterioration in the different CVFI sub-indices and main index are as follows:

• Income vulnerability: down 3.86 percentage points.

• Expenditure vulnerability: down 5.46 percentage points.

• Savings vulnerability: down 2.35 percentage points.

• Debt vulnerability: down 2.90 percentage points.

• Overall financial vulnerability: down 3.50 percentage points.

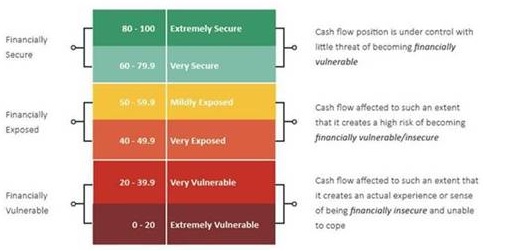

Table 1 provides an overview of the changes in the quarterly scores of the CFVI and its sub-components during Q2 2018 and the two preceding quarters. The measurement scale shows that during Q2 2018 consumers’ income was deemed to be under threat, hence the sharp decrease. This had a knock-on effect to the other three sub-indices that declined to below 50 points, reflecting a very exposed position.

TABLE 1: QUARTERLY OVERVIEW OF CFVI AND ITS SUB-COMPONENTS

Economic and political events impacted consumers’ cash flow perceptions during Q2 2018

Consumer financial vulnerability (at the micro-level) is to a lesser or greater extent being influenced by the prevailing macro-economic environment. Economic aspects impacting on consumer financial vulnerability during Q2 2018 included inter alia:

• Retail sales growth stagnated during the period Q1 2018 to Q2 2018, i.e., the real seasonally adjusted three-month retail growth rate from March 2018 to June 2018 was -0.5%.

• Real gross earnings per worker in the formal sector of the economy declined in Q2 2018 compared to Q1 2018 and were only 0.2% higher than a year ago.

• While the labour force grew by 0.4% over the period Q1 to Q2 2018, the number of employed only grew by 0.1%. Unemployment grew by 1.7% over this period while the unemployment rate (official definition) increased from 26.7% in Q1 2018 to 27.2% in Q2 2018. It is of special concern that during this period, employment losses were especially large among the African and coloured population groups. This is despite active labour market policy measures such as employment equity and BBBEE policies being in place to further their employment, i.e. employment among the African economic active population declined by 0.4% while their unemployment rate increased by 1.5%. Among the coloured population, employment declined by -0.8% during the period Q 1 2018 to Q2 2018 while the unemployment rate of this group increased by 0.8%.

• Headline year-on-year consumer price inflation (CPI) rates for Q2 2018 were on average 4.1% compared to 4.5% during Q1 2018. This quarterly increase in CPI gave rise to even less spending space for many cash-strapped households.

• Household credit extension increased by 1% during Q2 2018 compared to 1.3% during Q1 2018.

• The average South African Reserve Bank’s (SARB) leading indicator score for Q2 2018 was 106.3 compared to 106.6 for Q1 2018, which is indicative of economic contraction for this period. This assumption is being confirmed by available GDP figures showing negative quarterly GDP growth rates during the first two quarters of 2018.

• The average rand-dollar exchange rate weakened from R11.84 on 31 March 2018 (Q1 2018) to R 13.72 on 30 June 2018 (Q2 2018).

A closer look at the CFVI Q1 2018 Results

Why are consumers vulnerable?

The key informants contacted for the purpose of the Q1 2018 CFVI survey indicated various reasons why consumers were vulnerable during Q2 2018. Such reasons include inter alia:

• High levels of unemployment and retrenchments;

• An increase in Value-added taxes (VAT);

• Low levels of education among the South African population;

• South African consumers generally do not save;

• High fuel prices;

• Increases in living costs;

• Consumers generally live beyond their means and take up too much debt;

• A large percentage of South Africans are poor;

• Consumers are buying a lot of stuff they do not really need;

• The sluggish economic environment puts too much pressure on household finances;

• Increasing the cost of essential consumption items such as transport, electricity and food;

• A very volatile economic environment;

• A large percentage of credit-active consumers have adverse credit records;

• Households generally do not conduct financial planning and budgeting;

• High medical costs; and

• Income not increasing while price inflation is high.

When it comes to consumers in general, the key informants who participated in the Q2 2018 Consumer Financial Vulnerability survey believe that a mixture of low financial literacy and capability levels as well as bad consumer financial behaviour are the underlying reasons for consumers being financially vulnerable, namely:

• About 50% of key informants believe that consumers are generally not financially literate.

• About 65% believe that consumers do not plan their finances.

• About 66% opine that consumers are not living within their means.

• About 64% believe that consumers do not demonstrate self-control when it comes to spending and taking on new debt.

• About 68% believe that consumers generally do not consider the risks when taking on more credit.

• About 74% opine that consumers are not good at expanding their incomes.

When key informants were asked whether they believe that economic conditions will worsen over the period Q2 2018 to the end of Q1 2019, about 48% indicated that it will become worse. Furthermore, about 47% of key informants believe that the financial position of consumers will also worsen over this period. Of even greater concern is the fact that about 83% of key informants believe that unemployment will increase even further during this period.

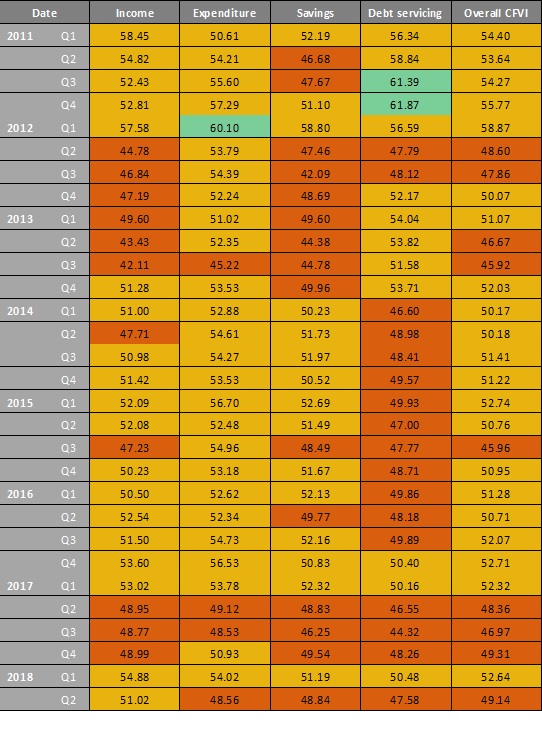

TABLE 2: SCORES OF THE CFVI AND ITS SUB-INDICES, 2011 TO 2018

TABLE 3: MEASUREMENT SCALE OF CONSUMER FINANCIAL VULNERABILITY INDEX

About the Index

The term ‘Consumer Financial Vulnerability’ implies that consumers experience a sense of financial insecurity or an inability to cope financially. In essence, the CFVI identifies the specific financial sub-component(s) that consumers on average feel are causing stress to their cash flow positions. Therefore, it provides a window into the psyche of consumers and how vulnerable they feel about their income, expenditure, savings, and debt servicing capabilities. Insights into consumers' financial positions are vital to determine the extent to which economic growth and government programmes translate into the improved financial stability of consumers. As a quarterly indicator, the CFVI fills an important information gap in South African data on consumer finances as viewed by consumers in the sense that it regularly provides updates on the state of consumers’ financial vulnerability. The results of this release of the CFVI stem from research conducted by Unisa on behalf of Momentum. The results of this release of the CFVI are based on a selection of 112 key informants from relevant industries (including credit industry institutions, retailers providing credit and municipalities) that are in a position to gauge consumers’ financial perceptions.

Compiled by:

Prof. Carel van Aardt, Bureau of Market Research, Unisa

Mrs Jacolize Meiring, Department of Taxation, Unisa

Prof. Bernadene de Clercq, Department of Taxation, Unisa

Mr Johann van Tonder, Researcher: Financial Wellness, Momentum