Worldwide country and sector risks

Europe remains the big winner in the world economic upturn.

World economic growth may not yet be at its highest (2.9% in 2017 and 2018 estimated), but there can be no denying that there are healthy signs. This quarter, once again, nearly all the revised country and sector risk assessments from Coface show marked improvements.

Europe promises a return to growth

The global economy is continuing its recovery, with the growth in world trade stronger than anticipated at the start of the year. Europe’s performance is buoyant and political risks (although having not disappeared altogether) are reducing. There are more positive signs in Brazil and Russia, and capital is once again flowing in some emerging countries. These positive trends have led Coface to improve several country ratings:

• Hungary (now A3) is demonstrating increased economic activity, supported by household consumption and renewed investments, due to flexible credit conditions and EU aid.

• Finland (now A2) has encouraging prospects in terms of corporate insolvencies (down 6% in 2016 and a further 19% in the first half of 2017) and growth (1.3% in 2017, with 1.7% expected for 2018), within a more favourable external context.

• Cyprus (now A4) is registering dynamic growth and has improved its controls of its banking and public finance sectors.

• Belarus (now C) is benefiting from the upturn in activity in Russia and Europe, which is favouring both exports and household consumption.

Nevertheless, the outlook is not improving for Europe’s major English-speaking countries, as illustrated by lacklustre savings rates and wage dynamics in the USA and the UK. This is being compounded by the lack of visibility around President Trump’s policies and the outcome of Brexit negotiations.

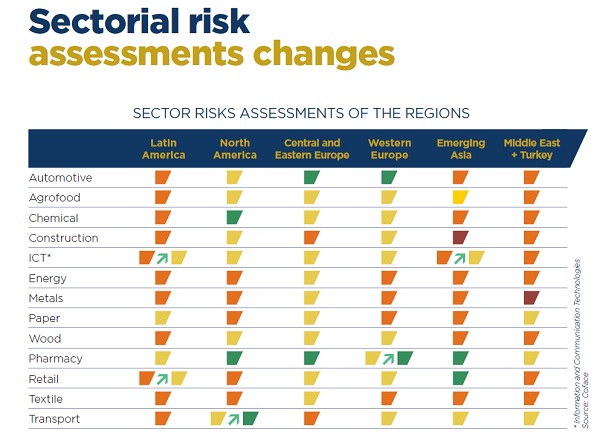

Industry and industrial channels linked to consumption are benefitting most from the upturn

Within this more buoyant global economic environment, several sectors of activity are rebounding. Industry is the biggest winner due to its pro-cyclical character. Following from marked improvements in the metallurgical and automotive industries in several of the world's regions during the first half of 2017, other sectors are following suit:

• The pharmaceuticals industry is proving to be the lowest-risk sector in the world. In Western Europe, and particularly Italy, France and Germany, the risk is now judged "low" on account of well-oriented production and demand. Corporate insolvencies are also low.

• North America’s transport sector is benefitting from public investment, hence its placement in the "low risk" category.

• The ICT sector is back on track in emerging Asian countries, China and Latin America. This dynamic illustrates the healthier condition of household consumption. In Brazil this positive trend follows a two year downturn in consumption. The risk is now rated "medium" in these regions and countries.

• Latin America has been the subject of another improvement, with retail joining the "medium risk" category at regional level and in Brazil, thanks to household consumption (aided by a reduction in inflation and the unemployment rate).

In two major emerging countries, Russia and South Africa, the agrofood industry is confirming its exit from crisis. The sector’s risk is now assessed as "low" in both countries, but for different reasons. In Russia, local businesses are benefitting from the food embargo on Western products, while South Africa’s excellent harvests have provided welcome relief this year.

Coface country assessments (160 countries) are ranked on an eight-level scale, in ascending order of risk: A1 (very low risk), A2 (low risk), A3 (quite acceptable risk), A4 (acceptable risk), B (significant risk), C (high risk), D (very high risk) and E (extreme risk).

Coface sector assessments (13 sectors in 6 geographical regions, 24 countries representing almost 85% of the world's GDP) are ranked on a four-level scale: low risk, medium risk, high risk and very high risk.