The Eurogroup agrees to resume negotiations with Greece over its bailout review

Eurozone finance ministers met in Brussels on February 20 to assess Greece’s progress in fulfilling the conditions of its €86-bn bailout. No final deal has been reached but finance ministers agreed to send again teams of experts to Athens to try to conclude an agreement on the bailout’s second review, the last mission broke down late last year. The Greeks had previously made concessions on new cost-saving measures.

Creditors suggested that they would now focus more on structural reforms than on austerity, thus accepting some fiscal easing in the medium-term if essential reforms are implemented in areas such as labour law, pensions and the tax system. According to European requirements, the Greek government is normally required to achieve a primary budget surplus of 3.5% of GDP from 2018 onwards.

Talks between Greece, its Eurozone creditors and the International Monetary Fund (IMF) over reforms, fiscal targets and debt relief have dragged on for months renewing fears of a new crisis in the Euro area. The completion of the second review should allow Greece to benefit from further Eurozone loans and meet its debt repayments.

Negotiations are being held while divisions remain between the IMF and European creditors. The IMF, which has not participated in the Greece’s third bailout, once again stated in its latest annual assessment, that Greece requires substantial debt relief from its European partners to restore debt sustainability (2016 Article IV

Consultation report – January 23, 2017). Europeans, especially Germany, are still opposed to it. However, Germany may reconsider its position after the September 2017 German federal elections.

Risks

A Greek payment incident cannot be ruled out if no deal is reached. The country has to repay $7.8-bn in the next five months, including $6.3-bn in July 2017 to the European Central Bank, the IMF and private investors, not to mention the refinancing of short-term treasury bills for $13.8-bn.

Some official relief has already been provided by European partners but it remains by far insufficient to restore debt sustainability in the long-term. Public debt, the bulk of which comprises official loans, has continued to rise, reaching nearly 184% of GDP in 2016, notwithstanding a large private-sector debt restructuring in 2011-12 and

flow relief from official creditors.

According to the IMF, policies underlying the ambitious medium-term primary surplus target appear unduly optimistic, although a good outcome was achieved in 2016, a

surplus of 2.3% of GDP.

Under the IMF baseline scenario, which assumes full implementation of reforms under the adjustment programme, debt is projected to reach around 160% of GDP by 2030 but become explosive thereafter due to the need to replace gradually a large amount of concessional debt with market financing.

Although there has been an impressive adjustment (primary and current account deficits have declined to around balance in recent years), the country has not managed to return to sustainable growth, with output having contracted by more than 25% since 2008.

Output started to recover in mid-2016 but GDP contracted 0.4% in the fourth quarter of 2016, which underscores the challenging state of the economy. Difficult negotiations with international creditors may have made consumers and investors more cautious. Moreover, in spite of a 5 percentage points decline since Q3 2013, double-digit unemployment rate, currently standing at 23%, is expected to persist

for several decades.

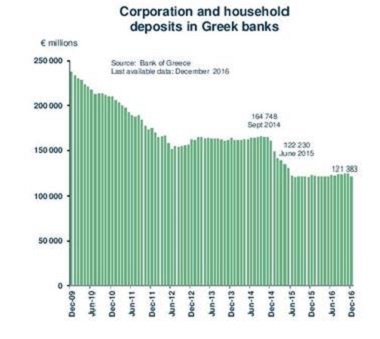

Waning confidence also seems to have been reflected in a decrease in banks’ deposits which fell to €121.4-bn in December 2016, from €124.8-bn in November although these figures would not be fully comparable according to the Bank of Greece.

Either way, the low level of deposits (see chart) does not bode well for an early lifting

of capital controls which continue to hamper export and import activities, although some steps to relax them have been taken. Moreover, the high level of non-performing loans (37% of total loans at the end of June 2016) weighs heavily on the recovery of credit.

The political situation remains fragile. The country has already experienced high government instability in recent years with five elections and a referendum in seven years. The government having been torn between the demands of creditors and its peoples’ needs to prevent social unrest.

The radical left Syriza party, allied with the nationalist right, only holds a three seat majority in parliament and early elections cannot be ruled out. Since the elections held in September 2015, Syriza’s support has declined significantly in polls. As of January 2017, the incumbent party lags 15.5 percentage points behind the New Democracy, the centre-right opposition party.