Nigeria and South Africa: Out of recession, not yet out of trouble

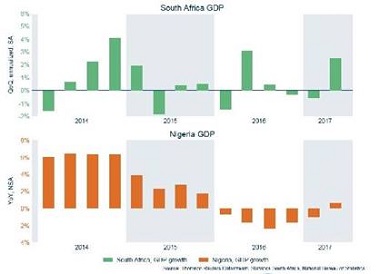

As expected, quarterly national accounts data published by national statistical agencies in Nigeria and South Africa indicated that both countries have emerged from recession.

In Q2 2017, Nigeria GDP grew by a dismal 0.6% year-on-year, after five consecutive quarters of contraction. Over the period from March to June, South Africa grew at an annual rate of 2.5% quarter-on-quarter. Nevertheless, positive figures are mainly a result of Nigeria and South Africa bouncing back from very poor performance. Exposed to internal and external headwinds, Nigeria and South Africa’s economic woes are not over; the recovery is still fragile.

Both in Nigeria and South Africa, agriculture is the main positive contribution to GDP growth in Q2 2017

After an El Niño-induced drought afflicted South Africa in 2016, agriculture, boosted by better rainfalls, recorded a 13% y-o-y growth. This figure is in line with the latest forecast from the Crop Estimates Committee, which indicates a possible 108.8% increase in maize output, the main crop, for the 2017 season. An increase in crop output is also the main reason for the solid performance of the Nigerian primary sector.

Nigeria and South Africa also rebounded thanks to improved performance in the extractive industries

The latter were in the doldrums in 2016 because of low commodity prices. Terrorism in the Niger Delta targeting production facilities created disruptions in Nigerian oil supply. Hence, a rebound in oil output after six consecutive quarters of contraction in oil GDP supported an exit from recession. In South Africa, the mining sector - struggling with low profitability for years - benefited from higher commodity prices in order to step up output and confirmed the recovery initiated in Q1 2017.

In South Africa, the return to positive territory is also attributable to wholesale and retail activities resilience

Statistics South Africa estimates that household final expenditure contributed 2.8 percentage points to Q2 2017 GDP. Easing inflationary pressure supported the recovery in trade activities, which recovered to 0.6% after it contracted by 5.9% in Q1.

Similarly, most sectors, except for construction (-0.5% q-o-q) and government services (-0.6% q-o-q), benefited from a positive base effect after bleak performance recorded in Q1 2017. Improved headline growth in Nigeria is also a result of particularly poor performance recorded in the reference period, namely Q2 2016.

Risks

Widely anticipated, the return to growth in Q2 2017 of sub-Saharan Africa’s two biggest economies could prove short-lived. Data reveal that growth is still heavily reliant on sectors vulnerable to external headwinds, namely agriculture and extractive industries:

1. Agriculture output remains exposed to climatic variations, which could accelerate with global warming.

2. The recovery in commodities prices is fragile. In particular, fading demand for metals and crude oil from China could hamper the recovery.

3. Still exposed to supply disruptions, Nigeria is unlikely to gain much from its oil sector as they agreed to cap production as part of the OPEC effort to address the oil market imbalances. Hence, Nigeria is unlikely to obtain further upside from its main export.

In addition to external headwinds, domestic challenges remain:

1. On a medical leave most of the year, Muhammadu Buhari’s ability to govern remains in question, as the country critically needs to diversify an economy overly dependent on oil revenues. Increased dollar inflows and a new foreign exchange window for investors and exporters eased the pressure on the Nigerian naira.

Nevertheless, multiple exchange rates continue to deter investment. Still under tight liquidity conditions, the government’s reluctance to let the naira float is still an obstacle to regain investors’ confidence.

2. In spite of the rebound in Q2 2017, prospects for the South African economy are still bleak. A high cost base and uncertainty surrounding the introduction of a new mining charter could weigh on a mining sector, which has been crucial in the rainbow nation’s return to positive growth.

Weak real wage growth and consumer confidence data indicate that the resilience of consumer spending, another driver of the recovery, could prove short-lived. Plus, political turmoil could still weigh on an already low business confidence with a nail-biting ANC conference in December 2017, where Jacob Zuma’s success or is to be decided. In addition, whoever succeeds Zuma will have to find solutions to reignite growth in order to rein in a record 27.7% unemployment rate, while curbing a rising public debt burden.