Hong Kong: Concerns despite robust growth

GDP figures show that Hong Kong’s economy expanded by 3.8% Y-o-Y in Q2 (1.0% Q-o-Q). While this is lower than the 4.3% Y-o-Y in Q1, it beats economist estimates of 3.3% Y-o-Y (0.6% Q-o-Q).

Rising asset prices and strong consumer spending, backed by low unemployment, drove performance in Q2. The Hong Kong Monetary Authority (HKMA) raised its growth forecast for full-year growth to 3-4% from 2-3% previously. Asset price gains were led by real estate and equities. Home prices have continued to soar, reaching new highs according to an index compiled by Centaline Property.

The government has stepped in to curb speculation by ramping up mortgage requirements and restricting developers from borrowing for construction and land sales, but these measures remain ineffective. The Hang Seng Index (HSI) has gained more than 25% YTD and came close to breaching the 28 000 level on August 8. Meanwhile, the HKD hit its weakest level against the dollar, reigniting speculation of a change to the currency board. The HKD is one of the few currencies in the region that has devalued against the US dollar YTD, alongside the Philippine peso and Sri Lankan rupee.

It is expected that fiscal policy will support growth momentum in the coming years. In what may turn out to be a major policy shift, new chief executive Carrie Lam pledged to break away from previous financial secretary John Tsang’s “miserly” fiscal policy last week. The move will entail making use of Hong Kong’s massive surpluses to boost spending on public services and infrastructure, even if this entails going into deficit.

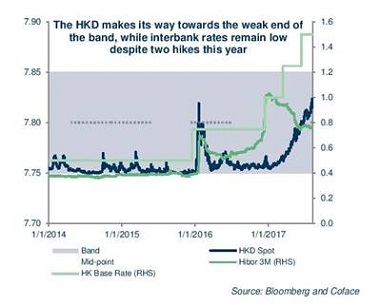

Improving momentum has not translated into HKD appreciation despite two interest rate hikes this year. This is because excess liquidity has continued to curb Hong Kong money market rates (Hibor), spurring carry-trades for the higher-yielding USD and CNY. The situation is different to the pressures experienced in January 2016. During that period, the one-year forward was trading above HKD/USD 7.85, as investors speculated that the HKMA would move away from the currency board.

Hong Kong has a fixed exchange rate and free capital flows but no independent monetary policy. Instead, it relies on the Federal Reserve of the United States (Fed) to determine interest rates. The regime is technically known as a “currency board”. Whenever the HKD nears the stronger end of the band, the Exchange Fund under the HKMA buys USD from licenced banks at a fixed rate of HKD/USD 7.75, leading to a build-up of FX reserves.

When the HKD creeps toward the weak end of the band, the Exchange Fund sells USD at a fixed rate of HKD/USD 7.85, depleting FX reserves. As a consequence, the monetary base expands/shrinks; a principle of currency boards which is enshrined in Article 111 of Hong Kong’s Basic Law.

Asset prices may have played a role in driving growth performance in Q2, but they remain vulnerable to shifts in liquidity. The latter remains ample for two main reasons: 1) the monetary base has expanded following from the Fed’s QE programme; and 2) the region experienced net capital inflows from mainland China. Mortgages remain cheap as they are based on the Hibor. Moreover, measures to restrict home purchases don’t impact cash-rich foreign investors. The HSI has experienced a six month rally as liquidity from the mainland made its way into Hong Kong equities through the new stock connects.

The PBoC tightened policy twice at the beginning of the 2017, but has since injected cash into the banking system to avert a sharp downturn ahead of the October Congress.

The HKMA may have started to become concerned about excess liquidity. It has announced the sale of HKD40b (EUR4.4b) worth of Exchange Fund Bills, aimed at draining liquidity from the interbank market. This may only be a fraction of the city’s HKD280b (EUR30.5b) aggregate balance, but they signal a nudge in the direction of higher local rates.

Risks

Coface expects the currency to continue to depreciate gradually, reaching HKD/USD 7.83 by year-end. However, a more hawkish Fed could drive this lower to around HKD/USD 7.85. While this scenario remains unlikely, the peg is here to stay, meaning that the HKMA would have to support the HKD via open market operations as per the rules of the currency board. This would translate into a smaller monetary base/depletion of FX reserves and lower liquidity.

Tighter liquidity is inevitable and it will lead to a correction in the city’s asset prices. This will impact equities (might have started already) and housing markets. Banks are especially exposed to the housing sector. A combination of falling housing prices and higher borrowing costs could impact bank’s balance sheets through deteriorating asset quality.

Expansionary fiscal policy could help to cushion some of the negative impacts of tighter liquidity. However, a more aggressive stance and shrinking FX reserves point towards worsening fundamentals for Hong Kong. The city has so far been characterised by its prudent approach to fiscal policy and budget surpluses. This may be about to change. Notwithstanding these caveats, the economy expanded faster than expected in the second quarter, leading to significant upside risks to our full-year growth forecast.