Euro area: Sluggish and disparate recovery

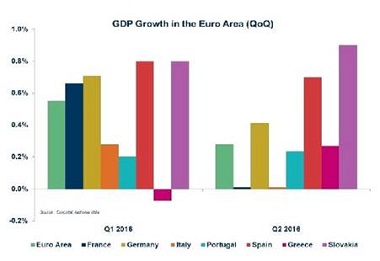

Euro Area GDP growth in the 2nd quarter of 2016 was 0.3% (Q-o-Q compared to Q1), indicating a significant slowdown in the area’s economic recovery compared to real GDP increasing 0.6% in the previous quarter. Activity increased 1.6% annually after rising 1.7% in the first quarter.

German GDP rose much faster than expected in Q2 (+0.4% Q-o-Q after +0.7% in Q1) that was boosted by exports and consumer spending while investment decelerated. Growth was flat in France and Italy after +0.7% and +0.3% in Q1 respectively as industry and domestic demand flagged in both countries.

Portugal also recorded weak growth (+0.2% in both Q1 and Q2 of 2016). In contrast, Slovakia recorded 0.9% growth in the 2nd quarter after 0.8% in Q1, reflecting strong growth in central Europe.

Spain’s real GDP expanded 0.7% Q-o-Q (+0.8% in Q1) with domestic demand again the main driver. Due to an increase in tourism, economic growth picked up in Greece to reach 0.3% in Q2 (-0.1% in Q1).

Weak domestic demand seems to be main factor explaining why the Eurozone saw its growth halved between Q1 and Q2.

1. Weakness in domestic demand: Investment dampened growth, in line with the fall in construction output (-1.8% Q-o-Q), was boosted by mild weather in the first quarter (+1.0% Q-o-Q). Industrial production was low in May and June in the Eurozone. Subdued growth in private consumption also dampened GDP growth in the area.

Euro Area retail sales increased in the second quarter but remained below expectations at +0.1% Q-o-Q after growth of 0.7% in Q1. In the context of steady employment growth and low inflation, private consumption is expected to remain a significant growth driver.

2. External trade contributed positively to Eurozone GDP growth: While Q1 soft net exports held back growth, in Q2 these were supportive, reflecting a fall in imports. Although exports fell by 0.2% Q-o-Q in the second quarter, the reduction in imports was more important (-2.4%).

3. Important divergences within the zone: Growth in Germany, the euro area´s largest economy, in Q2 was faster than expected, as consumption by both the private and public sectors put in strong performances and exports increased while investment cooled off.

In contrast, the slowdown in France was bigger than expected. Italy’s poor performance was the result of weaker exports, increasing uncertainties related to the political backdrop and the situation with some banks, leaving little room for growth the second half of 2016.

Risks

Euro Area growth could stabilise this year, with annual growth for the area likely to reach 1.7% in 2016 after 1.6% in 2015.

1) Brexit could eventually hurt. It is expected that Britain’s exit from the EU will hit the British economy. A slowdown will spread to the continent, notably through trade channels. Business confidence has shown resilience. In July the EU Commission’s Economic Sentiment Index, for the Euro Area as a whole, picked up 0.2 points to 104.6, contrary to market expectations of a drop of 0.9 points. National surveys for Germany, France and Italy also posted an increase.

2) Potential measures to sustain activity may come from monetary policy, given the lack of fiscal leeway in most countries. The ECB could provide the additional support needed to try to boost the recovery and push inflation to its target of 2%, even if the impact of these measures seems less important, whether or not the ECB acts again on interest rates and quantitative easing. The ECB may focus more on assets purchase rather than reducing its already-negative interest rates which are weighing on bank benefits.

3) Rising political and security risks in the Euro Area. Over the next 12 months Europe will witness several elections: The German regional elections, Italian referendum, presidential election in Austria, parliamentary elections in Lithuania and the Netherlands and the French presidential elections. Spain is still lacking an empowered government. Concerns about the rise in populism, given the region’s subdued growth, the migrant crisis and discontent over Europe policies, may lead to non-growth economic policies to satisfy voters. Terrorists attacks and constant threats could weigh on consumer confidence.