Euro area: A still fragile recovery with political uncertainty ahead

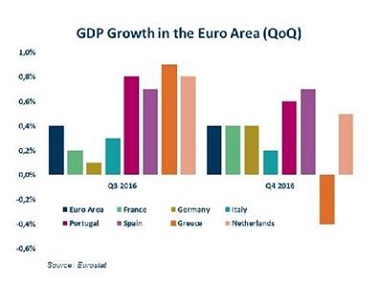

According to the second estimate released on February 14th, euro area GDP growth in the 4th quarter of 2016 rose 0.4% Q-o-Q, slightly below the consensus of 0.5%. With an average quarterly growth rate equal to 0.4% in 2016, the pace of growth remains stable.

Q4 to Q3 comparison reveals that Western Europe (Belgium, Germany, France and Austria) and Baltic countries (Latvia and Lithuania) performed well, with a positive change from quarter to quarter.

As regards Southern Europe, stability in Spain (0.7% in Q4 and Q3, Q-o-Q) contrasts with the slight deceleration in Italy (0.2% after 0.3% Q-o-Q) and in Portugal (0.6 after 0.8% Q-o-Q).

Greece unexpectedly registered a negative growth rate (-0.4% in Q4 Q-o-Q) after two quarters of expansion. Finland’s growth rate was also in negative territory (-0.5% in Q4 Q-o-Q). On average, Finland’s annual GDP growth rate reached 1.7% in 2016.

Domestic demand was the main engine of growth and is expected to remain so in the future. In particular, two major economies (France and Germany) showed encouraging results.

In France, GDP increased from 0.2% to 0.4% in the 4th quarter. Household consumption reached 0.6% Q-o-Q (after 0.1% in Q3). France’s capital formation also increased (0.8% after 0.3% Q-o-Q), supported by household investment and non-financial corporations (manufactured goods).

In Germany, growth reached 0.4% in Q4 2016. General government consumption expenditure was significantly higher, as well as capital formation (in particular in construction). Household consumption was on the rise too, but increased less relative to the two last components.

More generally, a certain combination of long-run conditions put growth on a solid base. First, the euro is still relatively weak, after a sharp depreciation in 2014-2015, which has benefited trade. Second, the ECB’s monetary policy remains accommodative, with the quantitative easing planned to continue until December 2017.

The European stock exchange did fairly well through 2016, which indicates a slight (but fragile) rebound in confidence. Latest PMI leading indicators were well oriented at the beginning of 2017. Overall employment has been on the raise (the rate of job creation being the fastest since February 2008), which points to a soft recovery in labour markets.

Risks

Inflation is on the rise, as oil prices slowly recover from their low levels over the past two years. Inflation is likely to sustain its upward trend in the future (0.2% in 2016 to 1.7% in 2017 according to the European Commission) but should still miss the lower band of the target set by the ECB (2%). However, core inflation is growing slowly (0.9% in January 2017).

With increasing inflation, real wages are not expected increase strongly in the future as they have in the recent past, and this will weigh on household consumption. Rising inflation may also erode businesses’ profit margins.

Political risk remains a hot topic in the coming months. Populist formations (such as the Front National in France, the AfD in Germany, the PPV in the Netherlands and, to some extent, Beppe Grillo’s 5-stars movement in Italy) are expected to perform well in the next elections and a victory for those parties is not excluded.

Such uncertainty triggers a wait-and-see approach by investors and affects confidence, as shown by the recent decrease of the ZEW index and increase of sovereign yields in euro area. However, financial markets’ behaviour is hard to predict as they seemed “tired” of political risk considering the lack of reaction during the recent “black swans” such as President Trump’s election and the referendum in Italy.

Important risks are still weighing on the euro area. The Maastricht Treaty has celebrated its 25th anniversary and latent issues undermine confidence in the European project. Among those, Prime Minister May’s decisions to opt for a “hard Brexit” in January 2017 could stir the divergences among Europeans and fuel further euroscepticism.

The debt crisis in Greece remains far from solved, amidst growing disagreement between the EU and the IMF. This revives fears of a hypothetical “Grexit”. The banking sectors are still fragile in Portugal and Italy, respectively burdened by 18% and 12% of non-performing loans in their total portfolios. In addition, the resurgence of protectionism in major economies (mainly in the US) could hamper trade worldwide. Finally, Europe has to cope with refugee crisis and terrorist attacks.