Don’t choke on your retirement with the wrong annuity

Retirement is a goal that most people aspire to with dreams of walks on the beach and long games of golf.

Sadly the reality is that for more than 90% of South Africans retirement is more a nightmare than it is a dream. The reasons for this alarming statistic range from a lack of preservation, insufficient contribution rates, low pensionable salaries and inappropriate investment choices.

An important factor to ensure that individuals have a comfortable retirement is the annuity that they select at the time of retirement.

Do I have to buy an annuity at retirement?

Once you reach retirement age and you were part of a retirement fund, you are faced with the question of what to do with your retirement savings that you have accumulated over your working career. By preserving your benefit every time you've changed jobs, contributing adequately and selecting an appropriate investment strategy, your retirement savings can be quite significant.

If you have been part of a pension fund, you have the option to take up to one third of your retirement benefit as a lump sum in cash, with the remaining two thirds being used to buy an annuity. However, if you were a part of a provident fund you have the option to take up to 100% of your benefit in cash. These rules are specified in the Income Tax Act and are not set by the insurance company. When deciding on the amount of the retirement savings benefit to take as a cash lump sum, you should bear in mind that this lump sum will be subject to tax.

What annuities do I have to choose from?

Once you have decided how much of your retirement savings you wish to use to buy an annuity, you are faced with the choice of which annuity to buy. It is a common misconception that there exists only one annuity type. The reality is that there is a myriad of annuities to choose from, each with their own pros and cons. You should speak to your financial adviser to determine the most appropriate annuity for you to meet your particular needs.

Many individuals select an inappropriate annuity for their specific circumstances and as a result they are left in an uncertain financial position that could have been avoided if they had understood the options available, the pros and cons of each and worked with a licensed financial adviser to make the correct choice.

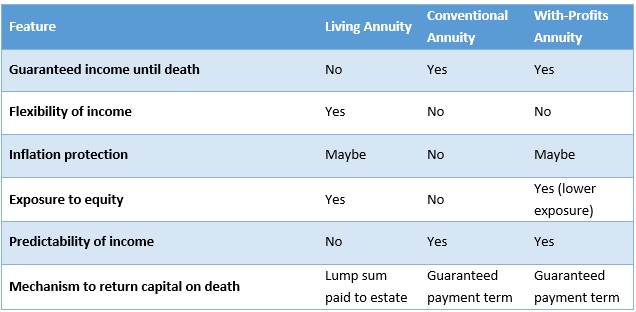

Living Annuity

These annuities are very popular in South Africa and while they certainly have a place in the retirement landscape, you should take time to understand the versatility of the product along with the risks that you face.

Living annuities provide you with significant flexibility and customisation since you can decide on the underlying portfolios that you wish to invest in and the level of income you wish to receive per month, known as the drawdown rate. However, the drawdown rate is limited to between 2.5% and 17.5%. This ability to customise your investment portfolio introduces you to investment risk because you will bear the full responsibility if the underlying portfolios that you chose perform poorly.

The flexibility in terms of the drawdown rate is also a risk because a living annuity provides no income guarantee. Therefore, when your retirement savings are depleted, you will effectively receive no further income. This can happen if you live longer than expected or when the underlying portfolios perform poorly. On the other hand, if you die and your retirement savings are not yet depleted, the remaining money will form part of your estate.

Conventional Annuity

Conventional annuities differ from living annuities. They offer limited flexibility and customisation but you do not take the investment risk, the risk of selecting the appropriate portfolios to invest your savings in, and the risk of outliving your savings.

With a conventional annuity the income is guaranteed for life, regardless of how long you live for. You do not have to worry about running out of your retirement savings or funds if investment performance is poor or if you live longer than expected. Unlike with a living annuity where the remaining funds are transferred to your estate when you die, a conventional annuity does not transfer any funds to your estate.

The income that you will receive depends on the cost of the annuity. The higher the cost, the lower the income. The cost of a conventional annuity is broadly determined by the following factors:

Age: The younger you are, the more expensive the annuity is because you have a longer life expectancy.

Gender: On average females live longer than males and therefore an annuity will cost more for a female than for a male.

Interest Rates: The higher the interest rates, the cheaper the annuity and the higher the level of income. If the interest rates change after you bought your annuity, the income that you receive will not change.

Annuity features: While conventional annuities are referred to as a broad category, there are many types of conventional annuities, each with their own distinct differentiating features such as guaranteed periods or increase agreements.

A guaranteed period is the period of time for which the annuity will pay an income, regardless of whether you are alive or not. The longer the guaranteed period, the more expensive the annuity.

The annuity agreement can also specify the increases payable. Therefore, the annuity could be level where your income remains constant throughout; a fixed increase annuity where your income increases every year by fixed amount, for example, 5% or an inflation-linked annuity which increases your income by inflation every year.

With-profits annuity

A with-profits annuity is a third annuity type that is very similar to a conventional annuity. Much like a conventional annuity it guarantees you an income until you die and it also does not pay the remainder of your retirement savings over to your estate upon your death. The difference between the two is that unlike a conventional annuity that specifies the increases up front, either a fixed percentage or inflation, the increases under a with-profits annuity are uncertain and not guaranteed.

The increases under a with-profits annuity are determined by the performance of the underlying investments and the mortality experience of the group of pensioners or policyholders. This means that if the mortality experience of the group was higher than expected and investment performance was better than expected, the increase in income will be high; but if the mortality experience of the group was lower than expected and investment performance was poor, then the increase in income payable to annuitants will be low, if any.

It is important to remember that once an increase has been declared it cannot be taken away. This new level of income, after the bonus has been declared, becomes guaranteed for life and your income can not drop to a lower income. Most insurance companies apply techniques to smooth the level of the increase in income so that members do not experience very volatile increases. With a with-profits annuity you take some of the investment and mortality risk but not all of it as is the case with a living annuity. Therefore, with-profits annuities are typically cheaper than conventional annuities.

What do I need to do?

The choice of which annuity to purchase is an important one and should never be underestimated. You need to be aware of the various types of annuities that are on offer along with their features and risks. To make the right choice you should always get advice of a licensed financial adviser to assist you in navigating the gambit of choices you face as you approach retirement.