China and the United States, two giants with feet of clay

The global economy remains stuck in a “Japanese-style” trap of sluggish growth, despite ever more expansionary monetary policies.

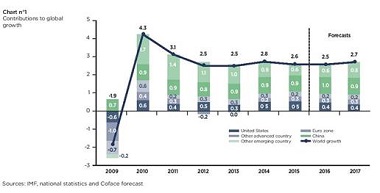

Unsurprisingly, global growth prospects have not improved since March. They have in fact deteriorated slightly with global growth forecast revised downwards by 0.2 pp to 2.5%, particularly because of the United States (see chart n° 1).

Few improvements are expected for 2017, since Coface expects global growth to remain lower than 3% for the sixth year running, and therefore stuck in a "Japanese-style" trap of sluggish growth.

Like in Japan since the middle of the 1990s, this lacklustre growth goes hand in hand with low-level inflation. Consumer prices are expected to rise only 2.9% worldwide on average this year according to the IMF, the lowest growth rate since 19801. For advanced economies only, inflation will probably be even lower than 1%, which is once again unprecedented.

This in turn is not encouraging central banks to tighten their monetary policy. No rate hike is on the horizon for the ECB or the Bank of Japan. The current slowdown in US growth is jeopardising the Federal Reserve's plan to raise its key interest rate. In the United Kingdom, the predictions of monetary tightening have been shelved and could even give way to expectations of rate cuts following the outcome of the British referendum.

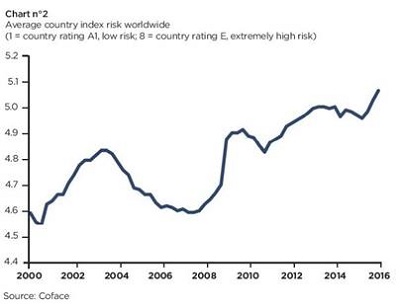

Companies are being negatively affected by this environment with low inflation limiting consumer pricing growth. Against this backdrop, company risk is increasing according to Coface’s country ratings, which measures the average credit risk in 160 countries.

The global average of these ratings show a marked increase in the risk level for companies worldwide. What is worse is that the current level is at a peak not seen since the early 2000s, the period when these country ratings were created (see chart n°2).

China: A short-lived respite

China partly explains this trend, with its country rating downgraded from A4 to B. The first quarter of 2016 briefly showed signs of a stabilisation in growth, due to vigorous credit growth encouraged by the central bank. The authorities are continuing to stimulate activity via accommodative monetary and fiscal policies, reflected by the stimulus measures that will increase the fiscal deficit to 3% of GDP in 2016 (versus 2.3% in 2015).

Nevertheless, the efficiency of such stimulus is increasingly limited and worsens the level of credit risk. The reason being overcapacity in many sectors (steel, cement, etc.). Moreover, Chinese companies' high debt levels explain why an increasingly significant part of new financing is not allocated to investment, but only used to refinance existing credit lines2.

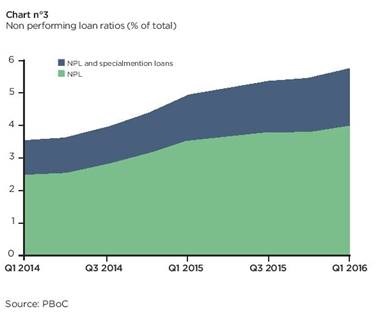

The IMF3 estimates that 14% of the loans taken out by Chinese companies can be considered as risky4, the most vulnerable sectors being steel (39%), sales5 (35%) and the mining sector (35%). And non-performing loans continue to grow, up 42% in the 2016 first quarter in year-on-year terms. When including "special mention loans", bad debts now account for 5.8% of total loans (see chart n°3).

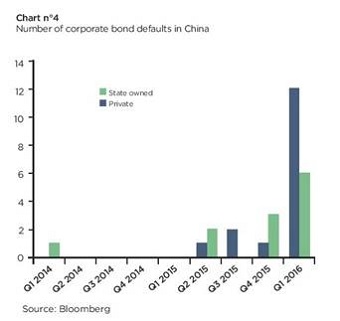

The Chinese authorities are therefore gradually realising that this expansionary monetary policy is not sustainable. Besides, the most recent activity indicators show a slowdown in growth in the spring linked to a reduction in allocated loans and microeconomic signals such as the rapid rise in the number of defaults in the local corporate bond market (see chart n° 4).

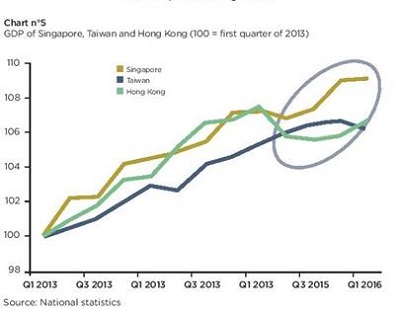

The rest of Asia continues to feel this Chinese shock wave. The latest payment survey undertaken by Coface highlights growing problems for companies, as more than 80% of the entities questioned recorded late payments in 20156. Businesses in the construction sector are by far the most affected by this lengthening in payment period. The most severely affected economies are Singapore, Hong Kong, Taiwan, South Korea and Malaysia.

Because these countries are very open and highly exposed to China7, they are facing a slowdown in growth and a rise in companies' credit risk. The high level of household debt (particularly in South Korea, Malaysia, Thailand and Singapore) could also weigh on activity. Their country ratings have therefore been downgraded. Conversely, the Philippines and Vietnam continue to post solid growth.

United States: Rise in insolvencies in the first quarter for the first time since 2010:

Growth is slowing in the United States, which is unlikely to exceed 1.8% this year and 1.5% next year. Companies are already feeling the effects of this contraction: the number of insolvencies in the US increased marginally in the first quarter of 2016 (+0.3%), for the first time in six years.

The decline in earnings is another tangible signal of the growing fragility of US companies: -6% year-on year in the first quarter of 2016, after an 11.5% fall in the fourth quarter of 2015. The fall in corporate earnings in the energy sector is, admittedly, not a surprise, but it does not explain everything. Excluding the energy sector, earnings keep falling (-7.9% year-on-year in the fourth quarter).

Companies are not the only ones to treading water. Job creation hit the lowest level in six years in May (at 38,000). And the decline in the unemployment rate (to 4.7% of the labour force) is misleading, insofar as it went hand-in-hand with a fall in the employment rate. In other words, the unemployment rate has fallen despite the small number of jobs created, as more discouraged job seekers, who have stopped looking for a job, are no longer included in the official figures.

Other bad news: the employment report confirms that the energy and manufacturing sectors are no longer the only ones loosing jobs. Sectors that until now have been in good shape, such as construction, seem to be running out of steam.

Only job creation in the healthcare sector prevented the US economy from loosing jobs in May. Household consumption growth will be slightly less vigorous than usual over the coming quarters, especially as the recent rebound in inflation (particularly in services such as leisure, rents and healthcare) is limiting growth in US consumers' purchasing power.

Europe: Investment is picking up, but political uncertainties are having a negative impact:

While growth slowed down in the United States, it accelerated in the eurozone in the first quarter (+0.6% quarter-on-quarter), fuelled both by household consumption and private investment. This good start should enable growth to reach 1.7% for the full year. The budgetary easing (especially in Spain) and, above all, the positive effects of the fall in the oil price on companies' margins as well as on household purchasing power are still at work. The ECB's low interest rate policy is also positive for companies.

The ECB's latest semi-annual survey on SME financing conditions in the eurozone published in June also highlights this trend. European small and medium-sized enterprises are less worried than in the past about bank lending conditions. For the third half-year in a row, they confirm they are seeing an improvement in the supply of bank loans as well as a fall in the interest rates offered. And for the first time, this improvement is also benefiting very small businesses. The most marked progress was in Spain, Ireland and Slovakia, whereas only Finnish and Austrian SMEs did not benefit from this improvement, according to the survey8.

Growth is expected to stabilise in 2017, amid a resurgence in inflation that is not offset by equivalent nominal wage growth, together with unemployment levels that remain high in most eurozone countries, despite the slight decline in their unemployment levels recently. And the risks linked to political uncertainties will also have to be monitored in the second half of 2016 and 2017. They are likely to weigh on growth, as they will lead households and companies to postpone certain consumption and investment decisions.

Various studies confirm this. In 2011, Aisen and Vaiga concluded that a higher degree of political uncertainty (measured by the number of changes of government) is associated with a lower per capita GDP growth, after studying the statistical relationship between these two variables in 169 countries between 1960 and 20049.

These results confirm those of Alesina (1996)10, according to which GDP growth in 113 countries between 1950 and 1982 was significantly lower when the probability of a collapse of a government was high.

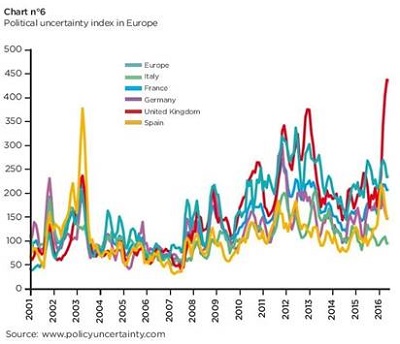

The EPU (Economic Policy Uncertainty) indicator11, which aims to measure the degree of uncertainty in terms of economic policy, confirms that this uncertainty is at a high level.

While it did not exceed 100 on average between 2001 and 2007, it has fluctuated between 150 and 200 since 2008 (see chart n°6). It even exceeded 400 in the United Kingdom in April and May, in the context of the campaign for the referendum on whether or not the country should remain in the European Union.

Because of the outcome of the UK referendum, it is unlikely that the degree of uncertainty will fall significantly in Europe in the coming quarters. Political consequences of the Spanish general elections in June, continuation of the Greek programme, regional elections in Germany in September 2016 and then May 2017, the constitutional referendum in Italy (autumn of 2016), general elections in the Netherlands in the first quarter of 2017, presidential elections and general elections in France in the spring of 2017 and, lastly, parliamentary election in Germany in September 2017.