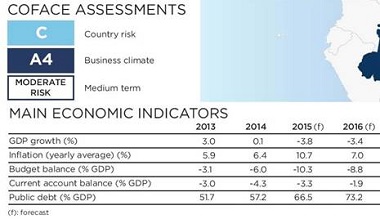

Brazil recession is expected to continue in 2016

Despite a moderate contraction in GDP in the first quarter of 2016 compared to previous quarters, the outlook for the Brazilian economy seems poor. Internally, household consumption, the main growth driver, should continue to be negatively affected by the high cost of credit, lower real wages due to high inflation and the rise in the unemployment rate, around 11% in April 2016.

Strengths

• 6th-largest economy worldwide

• Growing active population

• Varied and abundant mineral and agricultural resources

• Advanced manufacturing industry: aerospace, chemicals, pharmaceuticals and oil engineering

• Resistance to external shocks: creditor external position, considerable reserves

Weaknesses

• Lack of qualified labour/incomplete educational system

• Shortcomings in infrastructure (transport and energy)

• Insufficient investment

• High production costs (wages, energy, logistics and credit)

• Public expenditure high and inefficient

• Importance of corruption and inequalities

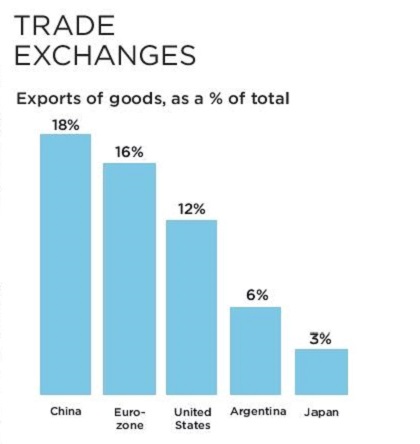

Unemployment is also affecting the country’s bank credit supply. The banking sector, exposed to household debt, is expected to experience an increase in non-performing loans contributing to a reduction in the supply of credit. Private and public investment should continue to contract due to the weakness of domestic demand and the pursuit of a fiscal austerity policy. Foreign trade is expected to be affected by the slowdown in Chinese demand and its impact on prices of minerals.

Export competitiveness should still be affected by the country’s weak transport infrastructure and rigid labour regulations, despite the gains related to the continued depreciation of the real against the dollar. Inflation is expected to decline in line with the weakness in domestic demand. This should nevertheless remain above the target set by the central bank (4.5%) due to the depreciation of the Brazilian currency. Rising unemployment and slowing consumer prices are expected to lead to the easing of monetary policy towards the end of 2016.

A primary deficit higher than expected in 2016

Adjustments to fiscal policy began in 2015, shortly after the re-election of President Dilma Rousseff, are having trouble being achieved. Inflation and the public deficit have continued to rise. The lack of a majority in Congress combined with the recession have also impacted the adjustment in public finances, which in turn has led to the decision by three rating agencies to downgrade Brazil to speculative grade.

The new interim government that took office in May 2016 has announced a higher than expected primary deficit estimated at nearly 72 billion BRL, or 2.8% of GDP. This increase is explained mainly by lower tax revenues expected during this year, but also due to the release of deferred payments under various programmes funded by the federal state.

The new government is now working on a fiscal adjustment plan that should be subject to the approval of Congress before next summer. Proposals such as reform of the social security system and tax increases are being considered. A widening budget deficit should result in a public debt dynamic that could reach 73.4% of GDP in 2016 from 66.5% in 2015 according to the government.

Improvement in the current account deficit driven by lower imports

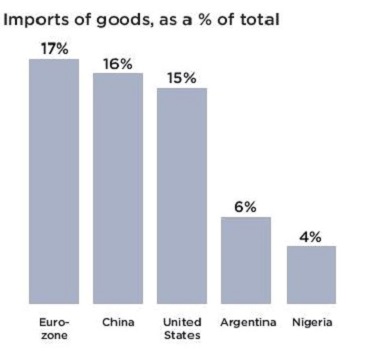

In 2016, the current account deficit is expected to improve due to weaker imports on the back of slower private consumption and investment, as well as the depreciation of the Brazilian real which has made imports more costly. Depreciation of the local currency would also help boost export competitiveness but exports will continue to be hit by low commodity prices. Trade in services and income balance (tourism. dividends. interest) will also remain in deficit.

The challenges of the Michel Temer’s new administration

In May 2016, the Brazilian Senate voted in favour of opening impeachment proceedings against the President Dilma Roussef with 55 votes in favour. This was 14 more votes than required.

Vice President Michel Temer now assumes the role of interim president while waiting the final decision of the Senate that should be held in August 2016. Barring unforeseen circumstances, two thirds of the vote in the Senate necessary for revoking the President should be achieved. Temer is expected to remain in power until the next elections in 2018, but he will face several challenges, including ensuring political stability due to his lack of legitimacy, not being elected democratically.

The success of his government will mainly depend on its ability to pass economic reforms to bring the country out of the current crisis and to restore credibility.