Bank of England interest rate hike: Risky bet if premature

On the 2nd November 2017, the Bank of England’s Monetary Policy Committee (MPC) raised the Bank Rate for the first time in a decade, from 0.25% to 0.5%. The Brexit vote has put the BoE in a dilemma: keep the rate at a record low after the emergency cut in August 2016 to support the economy, or raise the interest rate to keep a grip on inflation.

In recent weeks, monetary authorities have given clear signals that its tolerance for inflation further above its 2% target was declining and thus that an interest rate hike was approaching.

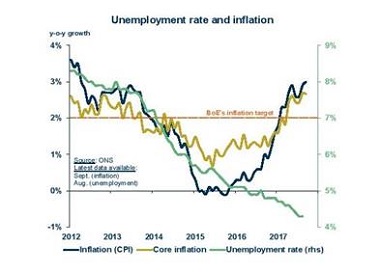

According to the BoE, the economy now looks to be close to running at full capacity as the unemployment rate fell to a four-decade low, and wages are likely to pick up and boost inflation pressures. The BoE’s hike aims at bringing inflation back to its target. The MPC stated that “any future increases in the Bank Rate would be expected to be at a gradual pace and to a limited extent.”

After the Brexit vote, inflation rose sharply because of the sharp depreciation of the pound after the vote. In September, inflation reached 3% y-o-y, its highest level since 2012, and “is expected to rise even further in October” according to the MPC.

According to the BoE’s latest research, currency depreciations in practice have almost double the effect on raising prices than its main models predict. In addition, the exchange rate pass-through effects took more time to materialise and are lasting longer than expected. Thus, “inflation is unlikely to return to the 2% target without some increase in interest rates”, Governor Carney said.

The most positive indicators are found in the labour market, with employment continuing to rise and the unemployment rate falling to 4.3%, a four-decade low. The labour market’s resilience, despite uncertainty and relatively weak economic growth, is remarkable. Monetary authorities fear second-round effects on wages due to higher recent inflation in this current context of a low unemployment rate.

Despite the Brexit headwinds, growth slightly picked up in the third quarter (+0.4% q-o-q after +0.3%) doing a bit better than expected. The economic activity has clearly been more resilient than expected since the Brexit vote, in particular thanks to dynamic private consumption in spite of decreased disposable income.

Risks

It is unclear how sustainable activity growth can be in the context of harder than expected Brexit negotiations. Recent shifts in the UK government’s position have increased uncertainty about the outcome of negotiations, which will probably be longer than initially expected. Combined with uncertainty, increased borrowing costs could affect an already sluggish investment rate even more.

In addition, business confidence could be hurt by such an economic environment. The MPC recognises that “there remain considerable risks to the outlook, which include…the process of EU withdrawal”. Some members of the MPC have suggested that this hike could be premature and thus contractionary.

Despite BoE concerns about secondary effects on wages, real earnings fell for the sixth successive month (-0.3% y-o-y in the three months to August) as prices are rising faster than wages. During the months following the Brexit vote, consumers dissaved so as to continue to spend in spite of a decline in their disposable income.

As a consequence, the saving ratio fell to a record low. Since then, consumers have had to cut spending and retail sales increased by only 1.5% y-o-y in the Q3: a four-year low. Although marginal, the symbolism of the interest rate hike could affect consumer confidence and thus lead to further spending adjustments, as around a quarter of borrowers have never experienced a rise in borrowing costs.

The increased cost of borrowing could precipitate a deeper adjustment in the construction sector. Combined with tighter mortgage lending rules, the higher mortgage costs could affect the real estate market. In Q3, the UK construction industry contracted for the second consecutive quarter. The construction PMI fell in September to its lowest since the Brexit vote. Moreover, while construction output remains high, new orders registered their biggest drop in five years in Q2.

Household debt remains high (146% of disposable income in Q2 with more than two thirds being mortgages) and is still growing. There were more than 15,000 individual voluntary arrangements (IVAs) to manage personal debts in Q3 – a record high. Moreover, 43% of mortgage borrowers are on variable-rate deals and will be immediately affected by the increased cost of borrowing. Therefore, although almost 90% of new mortgages are on fixed-rate terms, household finances could be jeopardised.

The automotive sector could also be affected. As about 85% of new car purchases used dealership car finance last year. As car loans have more than doubled since 2011, increased borrowing costs could hurt automotive sales.