Why it pays to start saving early

Francis Marais, Senior Research & Investment Analyst at Glacier by Sanlam.

Saving is often very much at the back of any young, recently employed person’s mind. Unemployment amongst young people is high. In fact that is an understatement - it is frighteningly high - with official figures for young people sitting at roughly just over 50%. Therefore landing that first job is an achievement in itself! Rightfully it is a cause for celebration. But beware, do not throw caution to the wind. If you want to celebrate by showing off your new-found financial independence by indulging in elaborate purchases such as expensive clothes, phones, perfumes or cologne and that very first car, you might want to think twice. In most of these examples some short-term debt usually accompanies these purchases in the form of clothing accounts, credit cards or vehicle financing.

While some celebration of your new-found freedom and independence is certainly warranted, now is the time you should start saving even more than at any other point in your life. Why, you might ask? Let’s look at a hypothetical example of two people who recently started their very first job.

Thando versus John

Thando, 25, recently started her first job and she cannot wait for her first paycheck. However, she recently read about the many South Africans who cannot afford to retire. She decided to visit a financial adviser who advised her to start saving R1000 per month into a tax-efficient investment such as a retirement annuity. While it represents quite a big chunk of her current salary, she is satisfied and feels empowered as she is taking control of her own, future financial independence. She continues saving R1000 diligently for the next 10 years. But, due to unforeseen circumstances, she has to stop contributing the R1000 monthly. However, the investment continues to grow and generate investment returns.

John, who graduated with Thando, was also lucky enough to find his first job, right after graduation. He, however, enjoys the smell of new cars and has had four different, fairly expensive cars over the last 10 years and likes wearing expensive clothes. At age 35, and married, he decides to engage the services of a financial adviser, who subsequently advises him to seriously start saving for his retirement as he has not yet made any arrangements for his retirement. Due to his very expensive lifestyle, he can only afford to save R1000 monthly and decides, based on the advice of his financial adviser, to also open a retirement annuity. His decision to approach a financial adviser was a clever move and he continued saving his R1000 over the next 25 years until he eventually retired at age 60.

The outcome

The above example is clearly hypothetical and saving R1000 per month is not enough, but will suffice for the purposes of illustration.

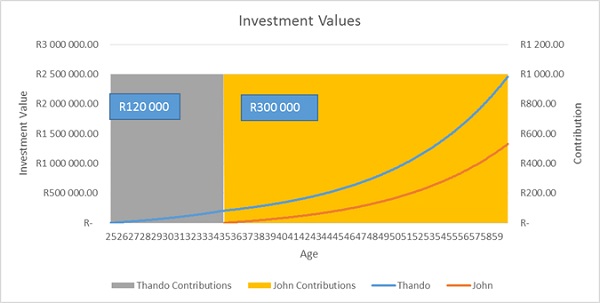

Let’s assume that both Thando and John’s investment grew on average at 10% per year. Who do you think had the largest sum of money at age 60? You might be surprised to learn that it is in fact Thando, who only contributed R120 000 in total (R1000 X 12 months X 10 years), who had the largest sum of money and not John, who contributed almost three times more: R300 000 (R1000 X 12 months X 25 years). The graph below indicates how Thando’s investment (blue line) grew in comparison to John’s investment (orange line).

How is this possible?

The answer is compound interest. Albert Einstein apparently referred to this phenomenon as the eighth wonder of the world. Those who understand it earn it (like Thando) and those who do not understand it, pay it.

The beauty of compound interest is that it works for you. For instance, if you invest R1000 in year one and are able to realise a return of 10% in that year, after the first year your investment will be worth R1100 (R1000 plus the R100). During year two, you will not only earn a return on the original R1000, but also on the R100 that you made during year two.

The longer compound interest has to work its magic the better, so the sooner you start saving, the better. Therefore, the mere fact that Thando started so much earlier so save, allowed her investment returns to start working for her and by year seven, the return she was receiving on her investment was already matching her contribution, i.e. R1000. By the time she stopped contributing to her retirement annuity, her investment was delivering a return of R1698-71 per month (exceeding the monthly contribution), and this is the reason why John could never catch up with Thando.

At the age of 60 therefore, Thando had an amount of R2 478 228-93 saved, while John only had R1 338 890-35 saved.