University fees - Will you be ready?

Hugo Malherbe, Product Development Executive at PPS Investments.

While university qualifications can be powerful tools for enhanced career growth and earning potential, education comes at a significant and ever-increasing cost. According to an analysis done by PPS Investments, if your child was born this year, by the time they reach the age of 18, university fees for an average four-year qualification could be as much as R1.2 million.

“The cost of education is increasing each year at a level greater than inflation. This means that each year a larger proportion of your annual income will be required to cover educational expenses - even if your annual earnings increase in line with inflation,” says Hugo Malherbe, Product Development Executive at PPS Investments.

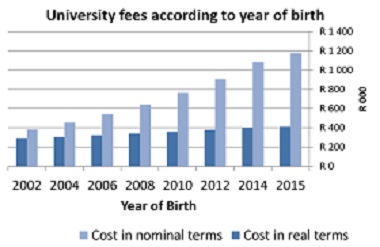

Source: INET bridge

“In practical terms, if your child was born in 2002 and they start university at the age of 18, their fees are likely to be around R400 000 for a standard four-year qualification. However, for a child born in 2015, fees for the same qualification could be just under R1.2 million,” he says. This excludes study material, living expenses and accommodation. This may of course vary depending on the qualification or institution and may increase if they study further or specialise.

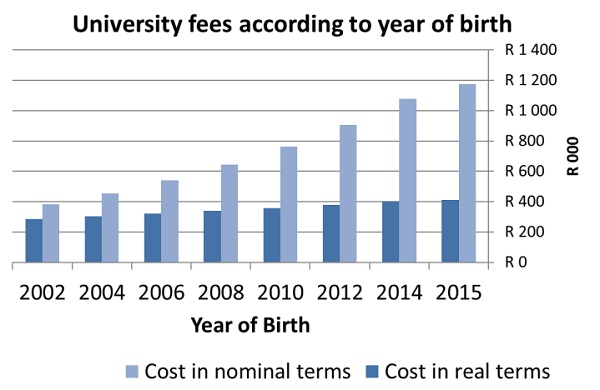

Source: PPS Investments research

“The reality is that few people can afford not to save for education. At the current cost of education, most parents will need to save far in advance to finance these considerable amounts,” says Malherbe.

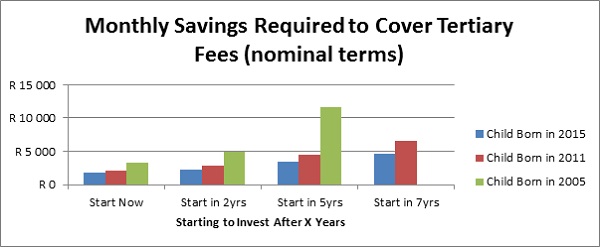

The younger your child is today, the more expensive their education is likely to be once they finish high school. And the longer you wait, the more exponentially this amount grows. Starting sooner will reduce stress levels and the burdens on your pocket in the long run.

Source: PPS Investments research

If you start saving a portion of the required monthly savings at least you will be able to cover a portion of the total cost. This is a far better alternative to young graduates having to start their careers with large interest-bearing student loans.

There are many investment vehicles which allow you to save for this purpose including endowment plans and discretionary investment products - and in some but not all cases - the recently promulgated Tax Tree Savings Account (TFSA). These support disciplined investing by allowing you to set up regular debit orders or save a lump sum.

A unit trust investment offers flexibility and no maximum investment limit. You can decide how long you want to invest and can make withdrawals from their investment more freely. With an endowment plan, one withdrawal is allowed during the investment term. This is generally a suitable option to consider if you have a marginal tax rate above 30% or have other discretionary savings.

Another option is a TFSA. Investors have a maximum contribution limit and if they withdraw they’re unable to replenish these amounts. Investors need to consider carefully before using this savings vehicle for education due to the limited contributions and marginal tax benefit for first time savers. The TFSA should ideally be used for longer term or additional retirement savings.

Whatever you decide, the most important factors are suitable advice to help you make an informed decision based on needs and starting to save as soon as possible.

While the data in this article was based largely on prevailing numbers available, this will vary depending on the institution, the qualification and the investment return achieved.