The Ultimate Power Couple: Saving and Investing

Debra Slabber

What are the best investments and where will I generate the greatest return, which areas of the market are the most attractive, what products should I buy, and which providers should I use?

Headlines, conversations and reading material are often centered around investment returns. These are all valid questions and certainly very relevant. While investment returns take center stage in conversations, it is only one side of the coin. The other side of the coin, that is often neglected, is your savings rate. For money to grow, it needs to be there, and saved, in the first place.

The magic really happens when you combine saving and investing, we could call it the “The Ultimate Power Couple”

Unfortunately, the harsh reality is that without savings, returns are impossible. The old saying “money doesn’t grow on trees” remains true. However, you can grow your money when you save and invest wisely. Working toward securing your financial well-being is one of the most important and rewarding goals you can have. The great part is you don’t have to be a genius to do it.

Successful investors all start with the basics. Only a small group of individuals stumble into financial security by, for example, inheriting a large sum of money or winning the lottery. For most individuals, the only and best way to attain financial security is to diligently save and invest and thereafter, wait patiently for their money to compound over time.

As uninspiring and boring as that may sound, there is something remarkable about it too. Regardless of how much you invest, if you just have the patience to let your investment compound and couple that with the discipline to continue saving through good, bad, and boring times, you will be amazed by the power of compounding over time. It is in fact, the eighth wonder of the modern world. In a way, it is the factor that levels the playing field for those who will not inherit or make millions with a tech start-up overnight.

The minimum requirement to save can be as little as R500 or even R100, depending on what vehicle you choose. You may ask, what if I don’t have any money left after spending? Once you start analysing what you spend your money on, you will be surprised how small everyday expenses (that you can do without) add up over a year. If you save as little as R200 per month, you can set yourself up to become a millionaire – more on this in our article “How to become a millionaire”. In the following article “How can I save when I have nothing left to save at the end of the month” we share some tips on how to find areas where you could save more.

Many people get into the habit of saving and investing by following the basic rule of thumb - always pay yourself first and spend what is left. The easiest way to get into a habit of consistent saving is to set up a debit order with your bank to automatically redirect money into a savings or investment account.

Lots of people do ask “what is the point of saving if my rate of return is sub-par”? I want to challenge that statement.

The amount saved is more important than the returns generated

At the end of the day, money can only grow if it is saved. We all want the best-performing investment portfolio but the reality is that performance is only one of the components on the journey to wealth creation. While you can’t control how markets will perform and/or your investments, you can control the amount you save every month. Investment returns are most certainly relevant and important, but so is the percentage that you save.

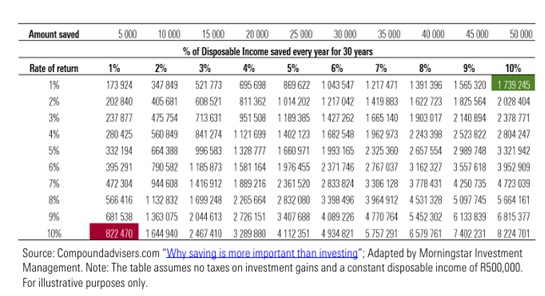

The table below shows you the end value of investing a certain percentage of your disposable income every year for 30 years.

• On the left-hand side, we show you the rate of return assumption, and at the top is the percentage you have saved of your disposable income.

• We use the assumption that the investor’s disposable income is R500 000, that it remains unchanged for 30 years and we have made no tax assumptions, to keep things simple.

What does this teach us?

• If you generate a 10% per annum return for 30 years, but you only save 1% of your disposable income (in other words, R5000) you end up with R822 000 – displayed in the red block.

• On the other hand, looking at the top right section - if you generate an investment return of only 1% but saved 10% of your disposable income you end up with R1.7 million (as displayed in the green block).

This shows how extremely important the habit of saving is; and that you can end up with a 111% higher ending balance if you save 10% compared to saving only 1% - even though the annualised investment returns were 9% lower!

In conclusion

Life is a constant balance between giving in to the ease of procrastinating or overcoming the pain of discipline. The same goes for our finances. Leave it up to chance, or act today and get your ducks in a row? What is life, if not the sum of a hundred thousand daily battles and tiny decisions that can shape the future of our financial success?

The key is just to start, and once you do, you’ll realise it’s a lot easier than it seems.