Six savings tips for volatile times

Adriaan Pask, Chief Investment Officer at PSG Wealth

There is so much uncertainty in the world today – from the two-year-long fight against the pandemic and consumers’ battle against war-induced fuel hikes, to investors trying to interpret global recession concerns or South Africans’ struggle with Eskom.

Considering these, you may well think the safest place for your money is in a shoebox under the bed. However, no matter how volatile markets get, the shoebox is never an option.

This is according to Adriaan Pask, Chief Investment Officer, PSG Wealth who shares six easy-to-follow tips on investing and saving during turbulent times.

Tip #1: Understand the arena

When you’re in a difficult situation, it’s easy to view the past in a rosier light. We tend to forget that markets don’t move steadily, progressing without any dips. There is an inherent cyclicality to markets as they blow hot and cold. More often than not, today’s winners will be tomorrow’s losers, and vice versa. Not all asset classes move in union, making it a rarity for all portfolio assets to underperform simultaneously.

Tip #2: Be vigilant

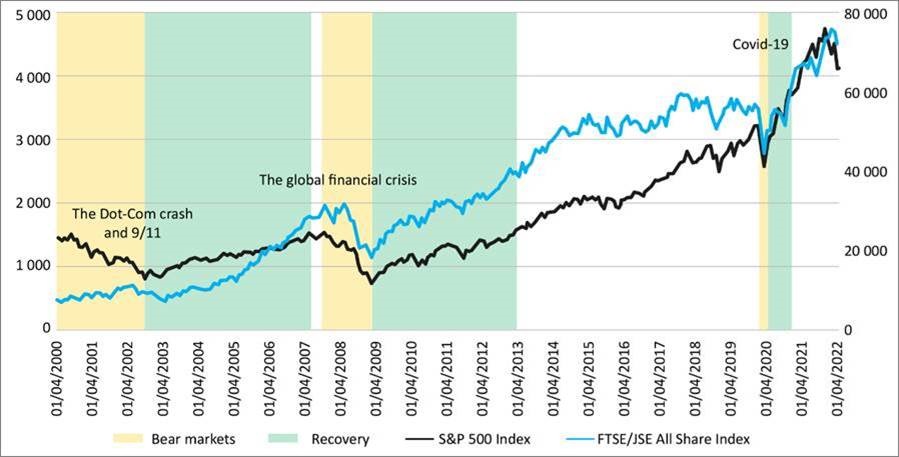

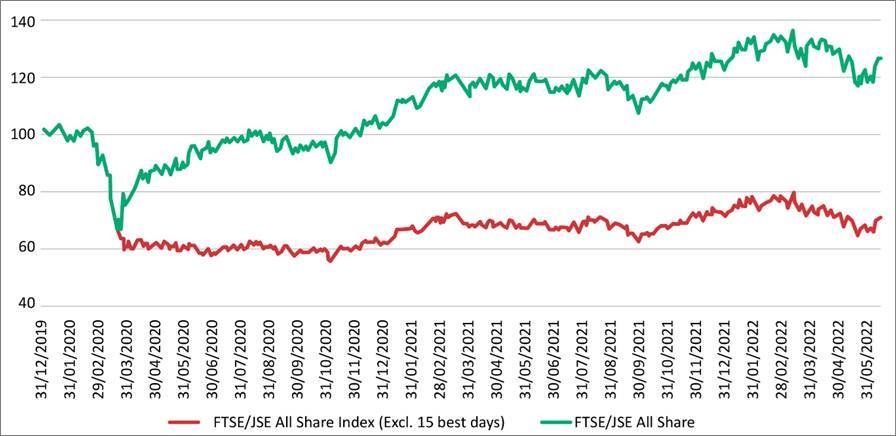

A golden lining to market drawdowns is that entry points become more attractive and affordable. And as markets are cyclical in nature, the bounce-back is inevitable. Graph 1 shows the last three major recessions/market drawdowns for the FTSE/JSE All Share Index (ALSI) and the S&P 500. Interestingly, the bounce-backs are significantly longer than the declines. To make the most of the recovery, you need to already be in position when the market turns. Graph 2 shows the best 15 days since the Covid-19 fall, and if you missed those, you would definitely have suffered a substantial loss.

Remember, you should always be vigilant about what you choose to invest in – just because a company is cheap doesn’t mean it’s a good investment.

Graph 1: JSE All Share versus S&P 500 since 2000

Source: PSG Wealth research team

Graph 2: Time in the market versus timing the market

Source: PSG Wealth research team

Tip #3 Act with calm

Don’t beat yourself up if you start to panic when you see the sea-saw of markets – especially when there are big declines (or even gains). However, remember that it’s dangerous to act while in this panicked state. Impulsive financial decisions can destroy the value you’ve been building. When taking financial action, you should do so rationally, logically and calmly. This is where a financial adviser plays a critical role.

Tip #4 Stick to your plan

The biggest risk to any savings plan is not having enough money when you reach your end goal. More than market volatility, the two biggest aspects that affect the end goal are time and investment contributions. For example, when investors pull back on risk appetite during market volatility without increasing their contributions to counter the reduced growth, they inflict severe losses on their investments. You cannot dial back on growth and not simultaneously understand the responsibility you, as the investor, will have to make up with additional contributions to your savings.

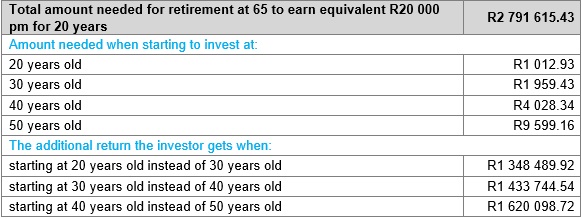

Table 1 illustrates the correlation between time in the market versus contributions. Assuming a set 6% interest rate, with the aim to retire at 65 and draw R20 000 a month for the next 20 years, an investor would need roughly R2.79 million at retirement. An investor who starts putting away about R1 000 a month at the age of 20 will save around R1.34 million more than the person who starts saving R1 000 at age 30. Thus, to counter this loss, the 30-year-old will need to increase their monthly contribution to almost R2 000. The lesson to understand from this is that less time you spend in an investment product, the more you will need to contribute at a later stage to make up for the shortfall.

Table 1: Retirement scenarios

Source: PSG Wealth research team

Tip #5 Diversify

Financial author Sam Beckbessinger asked which is better – investing R10 000 in one company or R1 000 in 10 companies? The answer is clear that if the R10 000 company performs poorly, so does your investment. However, if you construct a diversified portfolio that is tactically over- and underweighted in specific areas, you can hedge against mistakes made in the market. In this way you manage the greater risks while still achieving your investment and savings goals.

Tip #6 Don’t go solo

In times of stress and uncertainty, Pask adds that you need to know who you can turn to. He says that a trusted financial adviser is qualified to create an investment plan suited to your specific needs, and can advise you on the best way forward (or remind you of your investment plan) during market turmoil. “So, rest assured that you can upcycle and/or recycle your shoe boxes as desired, without tasking them with safekeeping your savings or investments,” concludes Pask.