Making the most of tax-free investments

Introduced in March 2015, tax-free investments have now been available to investors for three years. While this remains a relatively short history in terms of investment horizon, we are now able to see more clearly how investors are benefiting from the tax savings they offer.

While many investors have contributed on a monthly basis throughout the year, some are investing their maximum allowance at the beginning of each tax year, thereby gaining an additional year of tax savings and associated boost to their investments.

It is difficult to determine which types of tax-free investments would offer an individual the most benefit. This is because the savings will vary across individuals and different types of investments. The actual tax savings compared to normal (non-tax-free) unit trusts is dependent on a combination of factors, the primary two being: 1) your marginal income tax rate; and 2) the type and quantum of income and capital gains earned in your selected unit trust. Obviously, the higher your marginal income tax rate, the more you will save in these vehicles. At the same time, fund returns are taxed according to their source of income.

Which tax-free investments offer the most benefit?

Despite the above, we can draw some generalisations. It is particularly beneficial to hold listed property companies in the form of REITs inside a tax-free investment because there is effectively no corporate or individual tax on the investment returns. So if your primary motivation for investing is to maximise your tax savings, you may want to consider including listed property in your tax-free investment. However, this choice is dependent on many other factors as well, not least whether it is suitable for your overall portfolio.

While it may seem like holding cash inside a tax-free investment is also very attractive, because it does offer relatively high tax savings, it may in fact be the least appropriate asset class to choose for your tax-free investment over the long term. The primary concern of investing in cash (and other short-term assets) is that it earns after-inflation annual returns of 1%-2% over the long term. This is substantially less than the 6%-8% annual real return provided by growth assets like equities and listed property.

Being free of all taxes, the returns on these longer-term investments, re-invested and compounded over many years, will likely be much more powerful than cash. The potential long-term total investment return of cash is low, making it less appropriate as part of a long-term investment strategy.

An example of tax savings

To illustrate possible fund returns and tax savings over time, let’s see how much tax savings would accumulate to an investor in the 45% income tax bracket if they had been able to invest tax-free over the past 15 years and selected the Prudential Enhanced SA Property Tracker Fund tax-free unit trust. They are able to invest the full annual allowance of R33,000 every year for 15 years, which means that they would have contributed a total of R495,000 over the period. This is very near the current maximum R500,000 lifetime limit. I have used the highest possible tax bracket and allowable contribution expressly to try to provide an indication of what could be the upper limit of the tax saving for individuals.

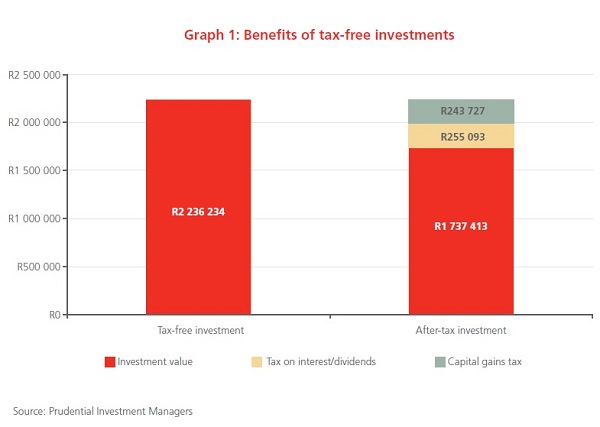

Graph 1 shows that the R495,000 investment in the tax-free fund would have grown to a total of R2.23 million by the end of 2017. By comparison, the same investment in the non-tax-free version of the Prudential Enhanced SA Property Tracker Fund (the identical fund but not the tax-free vehicle), and at the same fees, would have grown to R1.98 million, with R255,000 paid in taxes on interest and dividends (and with no annual exemptions applied). Then, when the investor decides to sell all or part of the non-tax-free investment, they will have to pay CGT of around R244,000 on these gains, reducing the investment value to R1.74 million and thus making the tax-free unit trust even more attractive.

The investor would therefore have notched up an extra R500,000 at the end of the 15-year investment horizon solely as a result of the tax-free benefits of this vehicle. This is a substantial bonus for anyone to add to their retirement income.

A holistic view

While this article focuses mostly on understanding the potential tax savings offered by a tax- free investment, don't forget the basics when it comes to making the most of investing: develop an appropriate long-term investment strategy; and remember to invest tax free for your children. By using tax-free investments in combination with other investment vehicles and allowances as part of a holistic, long-term investment plan, you can optimise your family’s overall investment portfolios quite substantially – and these tax savings together with an optimal investment strategy could have a significantly positive impact on your long-term returns.

Prudential will be participating in the Allan Gray Investment Summit in Johannesburg and Cape Town in July 2018. Visit www.investmentsummit.co.za for more.