Is there any tax benefit in saving over the annual tax deductible amount towards retirement?

Carrie Furman, tax specialist, Allan Gray

One of the key benefits of investing for retirement using a retirement fund is the generous tax deduction for contributions, subject to a maximum of 27.5% of the greater of your taxable income or remuneration, with an annual ceiling of R350 000.

While most of us may find it difficult to get anywhere near these limits in the midst of all of our monthly expenses, from time to time we may be lucky enough to get a bonus or another windfall, or perhaps our expenses adjust down as our children complete their studies or our homes are paid off. Under these circumstances, is there any benefit in contributing beyond the maximum annual tax deductible amount to a retirement fund?

The answer is yes. Retirement fund contributions can help to reduce your tax bill in more ways than one.

They can:

• Reduce your tax bill in the current tax year

• Reduce your tax bill in the next tax year or in future tax years (any unused portion carries over indefinitely)

• Reduce your tax bill when you withdraw or retire from a retirement fund

• Help you to get tax back from SARS on your living annuity income when you file your tax return

• Reduce the tax bill on cash your beneficiaries may choose to take from your retirement fund or living annuity on your death

These are explained in more detail below.

1&2. Reduce your tax bill this year and in future years while you earn

Contributing in excess of the maximum annual amount can benefit you in future years. This is because these excess contributions carry-over to the following tax year, and may reduce your taxable income during the next tax year, even if you don’t make any new contributions in that year. If you still make additional contributions in the next tax year, those contributions and the carry-over amount from the previous tax year are added together and are subject to the 27.5% annual limit again, with any excess carrying over to the following tax year. Carry-over can happen indefinitely throughout your lifetime.

3. Reduce your tax bill when you withdraw or retire from a retirement fund

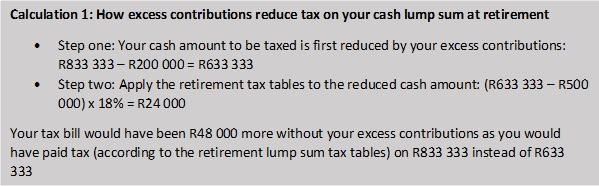

If you choose to take a cash portion from your retirement fund, the taxable amount of this cash lump sum may be reduced by any excess contributions SARS has on record for you. Your fund may ask you for a copy of your latest ITA34 (Notice of Assessment) from SARS to attach to your tax directive application. This is because the ITA34 contains the excess amount of contributions that SARS has on record for you at the time you filed your most recent tax return. If this amount is still available (and has not been used between when you filed your latest tax return and when your tax directive is applied for), it may reduce the tax you pay on the cash you are taking from the retirement fund.

It is important to note that the tax bill on your retirement cash lump sum takes all previous taxable cash lump sums you have received into account, including severance benefits and cash lump sums withdrawn from a living annuity (which is allowed if the value of your account falls below the prescribed limits).

Calculation 1 illustrates how SARS calculates your tax liability on the cash amount when the fund applies for a tax directive, and how excess contributions are taken into account. This calculation assumes that you are retiring from your Allan Gray Retirement Annuity and that the following applies:

• You have not taken any previous taxable lump sums, therefore the R500 000 that is made available to you during your lifetime at 0% tax is still available on retirement. This R500 000 amount is built into the retirement lump sum tax tables (see “Step two” in the calculation below). If you had taken previous taxable lump sums, you may not have the full R500 000 available, as the lump sum tax calculation takes the accumulated value of all previous taxable lump sums into account when you withdraw or retire.

• You have R200 000 of excess contributions on record with SARS.

• The market value of your Retirement Annuity (RA) is R2.5 million and you choose to take one-third in cash (R833 333)

The Income Tax Act states that the amount of tax to be withheld, as determined by SARS and indicated on a directive, is final. It’s a good idea to ask your fund to submit a simulated tax directive application to check whether you and SARS are on the same page regarding the excess contributions you believe are on your record before you submit the actual election to the fund. This gives you the opportunity to clear up any discrepancies and is important because a tax directive cannot be cancelled once applied for. You can also contact SARS to check what previous taxable lump sums, if any, they have on record for you.

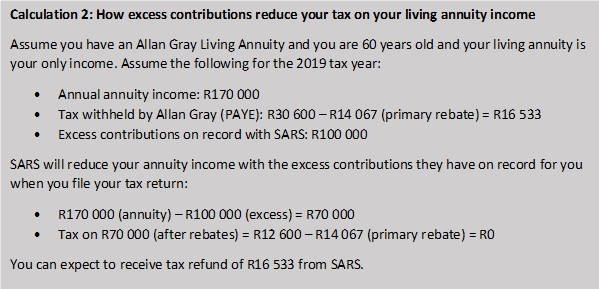

4. Get tax back from SARS on your living annuity income when you file your tax return

If you have tax-deductible contributions that you did not use when you retired from the fund or as a current year tax deduction, these benefits will still remain available to you when you receive your living annuity income and can reduce the taxable portion of your annuity income, as shown in Calculation 2.

5. Reduce the tax bill on your death

If your beneficiaries choose to take a cash lump sum from your retirement fund or living annuity when you die, that lump sum is taxed in your hands (SARS considers this as received by you on the day you pass away) and it is taxed according to the retirement lump sum tax tables. This means that the calculation takes any previous taxable lump sums you have received into account, and the taxable portion of the cash your beneficiaries take can also be reduced by any excess contributions remaining on your death. The calculation here works the same as in Calculation 2. One tax directive is applied for in your name for the total amount of cash all of your beneficiaries have chosen to take, and the after-tax amount is then split proportionately between them.

However, it is important to note that excess contributions cannot carry over to reduce the tax your beneficiaries pay on living annuity income, even if they choose to use your death benefit to open an annuity in their own name. This is because annuity income is taxed in their hands, whereas cash lump sums from a retirement fund or living annuity are first taxed in your hands and then paid over after tax to the beneficiaries. In short, excess contributions cannot carryover to different people and only belong to the person who made the contributions. Your beneficiaries will, however, be able to reduce the tax they pay on annuity income using excess contributions they have on record with SARS from the contributions they have made to retirement funds themselves.

Excess contributions are beneficial

There are many tax benefits to saving towards your retirement, whether you receive those benefits now or in the future, and whether it be in your lifetime or on your death. You should therefore not be deterred from contributing as much as possible towards your retirement, even if your contributions fall above the maximum annual tax deductible amount.