High-risk culture of dis-saving on the rise in SA

Andrew Davison, Head of Investment Consulting at Old Mutual Corporate Consultants.

The financial danger of accessing your retirement savings early.

As South African households are forced to tighten their belts as the country sinks into a recession for the first time in eight years and awaits further downgrades by ratings agencies, consumers may be further tempted to dip into retirement savings ahead of time. However, the impact on retirement savings, in the long run, could be devastating.

Andrew Davison, Head of Investment Consulting at Old Mutual Corporate Consultants, says that the recently released 2017 Old Mutual Corporate Retirement Monitor shows a dramatic increase in the number of fund members who intended drawing cash from their retirement savings should they change jobs (35% compared to 19% four years ago).

Davison says there are several factors influencing this behaviour. “These include the current economic downturn, increased debt levels, an increase in retrenchments and the tendency to change jobs more frequently.”

He adds that in light of the current economic landscape and subsequent strain it is placing on consumers financially, South Africans may be more inclined to spend their retirement savings when they should instead be reinvesting it for when they most need it, namely retirement.

The Retirement Monitor’s findings also revealed that, when changing jobs, fewer members are choosing to switch to a retirement annuity (falling from 12% to 8%) or opting to place their retirement savings in a preservation fund (decreasing from 6% to 3%).

“Unfortunately, the decision to access retirement savings early to alleviate current financial strain has a huge impact on future finances, one that retirement members often fail to take into account, or are simply not informed about.”

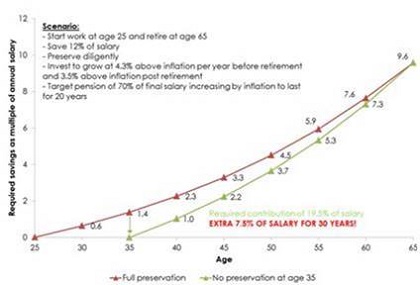

Davison gives an example. “If at the age of 25, Joe Soap had started contributing 12% of his salary towards his retirement savings, and he earned returns of 4.3% above inflation per annum on average, he would have accumulated savings of almost ten times his annual salary at retirement. This is based on the assumption that he has a 40-year working lifespan.

“His accumulated savings with interest would be sufficient to provide a retirement income of approximately 70% of his final salary. If his savings continued to earn after-inflation returns of 3.5% a year after retirement, he could enjoy annual increases in pension roughly in line with inflation and his retirement savings could potentially last for another 20 years, or until he turns 85,” he explains.

Davison notes that by the age of 35, or 30 years before retirement, Joe would already have saved 1.4 times his annual salary. Let’s say that Joe now finds a new job. Two things are likely to influence Joe’s decision on what to do with his retirement savings. The first is that Joe still feels he’s a young chap with no real reason to worry about retirement just yet. The second is that 1.4 times his whole annual salary does look attractive and there are so many things on which he could spend such a large amount of money!

“Although it might seem that he still has enough time to catch up on his savings strategy, if he cashed out at this point, the impact on his savings would be significant,” Davison explains.

He adds that if Joe cashed out at the age of 35, he would now need to catch up because his retirement needs haven’t changed but he’s reset his savings to zero. He still needs to get to 9.6 times annual salary at age 65. He would thus have to start saving an additional 7.5% of his salary or a total of 19.5% of his salary towards his retirement savings to be in the same position at retirement.

“This additional 7.5% savings amount is not feasible for most people – and it is this recovery gap that people tend to underestimate when accessing their retirement savings relatively early in their life journey.”

If Joe made the same decision to withdraw his retirement savings at the age of 45, Davison says the amount required to catch up would increase to 35% of his salary, which is a significant chunk of his income. He would also not be able to claim all of it as a tax deduction as the maximum annual limit is 27.5% of salary.

“The reality is that while it may be easy to justify accessing your retirement savings by saying that you will catch up, very few people can afford to put away such a huge chunk of their income, least of all those who are already in a financial position that requires them to access their savings in order to survive,” he says.

Tax penalties for early withdrawals:

Davison says that National Treasury has recognised the growing impact that this culture of “dis-saving” is having on the South African economy. In addition to imposing existing heavy tax penalties for early withdrawals of retirement savings, they are also looking at other ways to dis-incentivise this behaviour. These measures include requiring compulsory preservation in all but a few extreme circumstances, such as severe illness or retrenchment.

“In a nutshell, if you change jobs and withdraw a lump sum from your retirement savings, only the first R25 000 is tax-free.” Also, you only get this R25 000 tax-free allowance once in your lifetime. The next time you choose to withdraw your retirement savings, you will pay tax on the full amount. The rate of tax can be as high as 36% for larger amounts.

“However, these tax payments don’t apply if you choose to leave your savings untouched until you retire,” adds Davison.

What employers can do:

Malusi Ndlovu, head of Old Mutual Corporate Consultants, says one of the ways employers can encourage preservation (saving your retirement investments instead of cashing them in) is by making available suitable default options for retirement fund members.

Ndlovu points out that, 45% of members want the fund to recommend an option or to provide a range of pre-selected options. “The reality is that 61% of fund members actively choose the default portfolio in a retirement fund because they either trust that it is appropriate, or they are not confident enough to make their own choice,” he concludes.