Willingness of SMEs to offer retirement funding solutions is not translating into action, says new report

Clement Chinaka, Managing Director at Old Mutual Corporate.

According to the inaugural Old Mutual SME Employee Benefits Monitor 2015, the vast majority of South Africa’s small and medium enterprise (SME) decision makers (79%) and staff (90%) believe that the company should be making the provision of retirement funding to staff a business priority.

However, with 66% of SME decision makers and 47% of staff reporting that retirement funding provision was not on their company’s agenda, and 58% of SME decision makers and 63% of staff believing that the company have not provided adequately for the long-term wellbeing of staff, it is clear that the recognition of the company’s role in providing for the retirement needs of their employees is not translating into action.

The Monitor surveyed 514 SME decision makers and 503 staff employed by SMEs in operation for more than five years, with an annual turnover of between R2 – 200 million and employing more than 10 staff.

Clement Chinaka, Managing Director at Old Mutual Corporate, says the purpose of the Monitor was to gauge levels of preparedness for retirement amongst SME employers and their staff and their attitudes towards employee benefits. “Little research exists as to whether SMEs are financially empowering their staff through the provision of employee benefit offerings, and to what extent. We believe the findings of the Monitor will be invaluable to all stakeholders in South Africa’s future,” says Chinaka.

Speaking at the SME Monitor launch in Johannesburg today, Doug Clothier, General Manager: SME at Old Mutual Corporate, says that it is concerning that many SMEs don’t offer any employee benefits.

Contributing approximately 50% to South Africa’s GDP and accounting for roughly 60% of the labour force, SMEs have been praised as holding the key to South Africa’s continued socio-economic development.

However, with less than half of smaller companies (those that have a turnover of less than R13 million per annum) offering retirement funds, it is clear that SMEs need to do more if we are to address the long term financial security of South Africans, says Clothier.

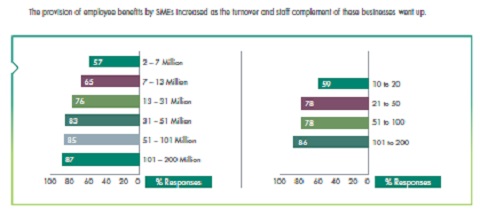

He adds that one of the key findings of the Monitor was that the size of the SME plays a large role in whether or not it offers some form of employee benefits to staff (see Table 1). “Our findings show that the percentage of SMEs offering some type of group employee benefits rose significantly as revenue and staff numbers increased.

“This isn’t a surprising outcome as at the start of a business owners are primarily concerned about survival. The challenge is to convince SME decision makers that it is possible to implement employee benefits in the early stages of their lifecycle. It is imperative that these perceived barriers be removed if we are to address the savings crisis in South Africa,” says Clothier.

Some of the reasons given for not offering benefits include affordability by the business; the view that the business is too small or that employee benefits are too administratively intensive.

Table 1: The provision of employee benefits by SMEs turnover (pa) / size

Employee benefits can have positive spinoffs

The Monitor found that drivers that push SMEs to provide employee benefits include company cash flow (can they afford it), the mind-set of owners (social responsibility for wanting to make provision for staff), the need to attract and retain skilled staff, external pressure (such as legislation or unions) and the stage of the business.

The majority of SME decision makers (64%) and SME staff (69%) believe that employee benefits offered by a business play an important part in attracting employees. “Benefits provided to staff increase the value they derive from working for an employer, thereby making the business a more attractive place to work. But these benefits can also strengthen the commitment of staff to their employer as they feel more valued within the business,” says Clothier.

Shifting priority from precautionary savings to long-term view

When SME staff were asked which employee benefits are important retirement funding (92%) and medical cover (82%) ranked as the two most important, followed by funeral cover (17%). Clothier says that it is positive that 57% of SME staff ranked retirement fund as the single most important benefit.

“Although medical aid and funeral cover can provide more immediate and tangible benefits, retirement funding needs to remain a priority for an employer. The long term financial security of staff requires that they save towards their retirement over their full working life, and it is therefore important that employers implement retirement plans for their staff. What is encouraging is that many staff in SMEs recognise this.”

The findings also revealed a clear gap between the need for preservation of retirement benefits when an employee leaves their job and actual preservation activity. While 88% of SME decision makers and staff surveyed agreed that preservation of retirement savings is important, 50% of SMEs believe that most staff will take all or most of their benefit in cash when they leave their job.

When those SME staff who are not adequately prepared for retirement (54%) were asked who they will rely on financially, over half of the respondents said they will rely on Government and family (each source being indicated by 26%), followed by 16% stating a combination of children and government.

SMEs have the opportunity to improve saving levels

“SMEs can play a large role in improving financial security at a national level. While the findings of the Monitor revealed employee benefits and retirement funding is a priority for SMEs, not everyone is doing it. It is therefore critical to communicate to SME decision makers the value of implementing these benefits, as well as removing perceived barriers to implementation,” concludes Clothier.

To view the full Old Mutual SME Employee Benefits Monitor 2015, please visit www.oldmutual.co.za/SMEMonitor