Think in reverse about your retirement savings

There is a major gap between expectation and reality when it comes to saving for retirement. Many South Africans don’t consider that they need to replace their current income once they retire from work. According to Ferdi Booysen, Head of Client Solutions at Old Mutual Wealth, this is why it is important to first determine what amount of income you want to receive from your retirement funds, in order to determine what you need to save now to be able to maintain your desired standard of living during retirement.

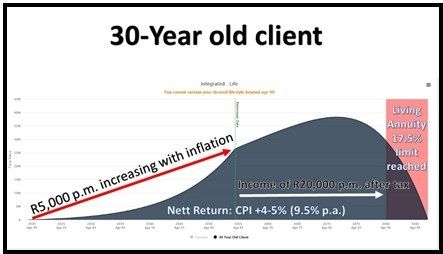

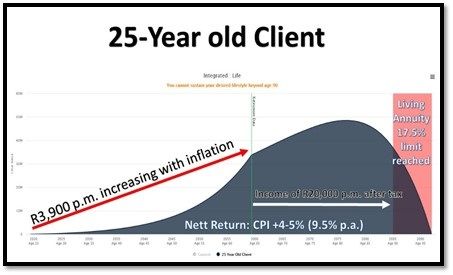

For example, if you decide you want to receive an income of R20 000 per month after tax for 25 years (increasing with inflation every year) you can then ascertain how much you need to put away each month to achieve this lifestyle goal. A 30-year old, who wishes to retire at 65 and wants to sustain the above mentioned after-tax income until age 90, would need to contribute R5,000 p.m. to a retirement annuity (increasing with inflation every year). If he/she started contributing 5 years earlier (at age 25), this amount reduces to R3,900 p.m. (22% less) based on our assumptions*.

South Africans are unfortunately known for not being proficient savers and there are many reasons for that, says Booysen. “The economic situation in South Africa places a lot of financial pressure on the middle- and lower-income classes, which means that basic expenses like food and shelter will always take precedent over long-term savings. In turn, some higher-income earners often live beyond their means in trying to keep up with their peers and therefore not save as much as they should,” he explains. Financial advisers can play an important role in bridging the retirement expectation gap by assisting their clients to visualise their retirement with their current requirements in place and help them see their ideal situation. Booysen notes that when you partner with a financial adviser, the adviser can talk you through and model different scenarios to make it easier to understand the bigger picture. “The adviser should be able to clearly demonstrate how your decisions impact on whether you will be achieving your long-term goals. It is also vital to understand what risks you must take in relation to the risks that you are willing to take,” he explains.

The old way of looking at risk saw clients filling out a long questionnaire to assess their risk appetite, but this only captured their risk appetite at a certain point in time, says Booysen. “It is not necessarily a true reflection of what the client is willing to achieve. People have different appetites for risk with different parts of their wealth, during different phases of their lives.”

“Visualising what your retirement will look like with current provisions is not the easiest thing to do on your own. This is why it is extremely useful to create a lifetime cashflow model or view that includes short-, medium- and long-term financial goals. For this to be demonstrated visually it is advisable to speak to a financial adviser. At Old Mutual Wealth we use a modelling tool called Integrated Wealth Planning, which creates a clear image of savings over time and you can see in real time how your life decisions will affect your financial position in the long run.”

“When you start with the end-goal in mind, you are more likely to achieve the end-goal as you know exactly what path to follow. When you have determined your end-goal and know what you need to do to get there, it is extremely important to stick to your plan and not deviate from the path. However, life happens and there might be some unexpected events that lead to unexpected expenses. A financial planner should be able to assist you to rework the plan after an unexpected turn of events to get you back on your road to the end-goal within good time,” concludes Booysen.