The power of preservation

Thandi Ngwane, head of strategic markets at Allan Gray.

Withdrawing your retirement savings when you resign could cost you far more in the long run. Thandi Ngwane from Allan Gray explains how you can protect your nest egg.

Here is a common scenario: you resign from your job. Finance sends you a form to choose what you would like to do with your retirement savings, but offers no further advice and don’t put you in touch with a financial adviser.

Your options are to make a full cash withdrawal, transfer the savings to a preservation fund or your new employer’s retirement fund or a combination. You think of your debt or if you have been dismissed, the anxiety of being without an income weighs heavily on your mind. You start thinking that a cash lump sum could come in handy – without really understanding the effect on your future income in retirement. Before you know it, you’ve filled out the form with an instruction to withdraw your full benefit in cash.

It is a decision many have taken. A 2015 survey done by Sanlam found that 77% of people leaving their jobs were taking their retirement savings as a cash lump sum.

About 63% of them use the money to pay off debt and 57% use it to cover living expenses while looking for a new job.

Phakama Mlangeni* (33) withdrew her retirement savings when she resigned from her job of eight years to fund a study break. She thought she had a good plan in place: pay off her credit card and revolving loan, pay her fees for two years and draw a small income for living expenses.

Unfortunately, it didn’t work out that way. After paying off debt and her fees, the money she had left ran out eight months later. In no time, she found herself back in debt to cover her living expenses while studying.

How to get back on track

A retirement income equal to 75% of your final salary is a reasonable figure to aim towards to live comfortably in your ‘golden years’.

Phakama is determined to get her retirement savings back on track when she starts working again in two years’ time after completing her studies. She will be 35. After using an online retirement calculator, she realises she will have a 44% shortfall in her retirement income – or put simply, she may not have enough saved for a comfortable retirement if she lives beyond the age of 80.

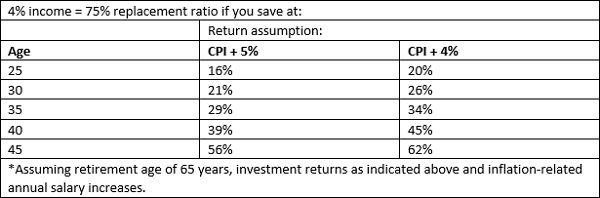

The table below shows she will have to put away 29% of her income towards her retirement as opposed to just 16% (assuming she started contributing at age 25) if she had not taken the withdrawal. Putting away almost 30% of her income may be unrealistic, so she may need to look at what else she can do to still achieve her goals.

Retirement savings rates needed to ensure 75% Replacement Ratio*

Phakama started a small business as a personal stylist and shopper during her career break. If she is able to continue running her business part-time while working, she could use the additional income to top up her retirement savings.

She could also delay her retirement by another five years to age 70 if possible. In this way, she will get a 10-year boost in her retirement savings through capital growth and compound interest – where the interest on the investment earns even more interest. If she does this, her income after retirement could be sustained for 35 years until she is 105, as opposed to just 81 years old if she retires at 65.

The first R500 000 of the cash lump sum you take at retirement is tax-free. However, any withdrawal you make from your savings before retirement reduces this benefit. To avoid a huge tax bill at retirement, Phakama should avoid taking a lump sum in excess of her tax-free allowance as it will be heavily taxed. If she has no need for the lump sum portion at retirement, a better option would be to transfer the full investment into an income providing investment such as a living annuity, where it can continue to grow, tax-free. While she will pay tax on her income from her living annuity, this will be at her marginal tax rate.

Your best options

Sadly the implications of withdrawing your savings are often not fully explained. And if you have suddenly lost your job, your retirement savings may be your only source of funds to cover your living expenses while you look for a new job.

If you have no choice but to tap into your savings, rather take only what you will need until you start working again. If you have already lined up a new job or have other sources of income when you leave your company, avoid taking a cash lump sum for ad hoc spending. Rather transfer your savings to your new employer’s retirement fund or a retirement annuity or a pension or provident preservation fund. By doing this, you would keep the tax benefits of your original fund and your investment returns are not taxed.

*Not her real name

Allan Gray will be presenting at the Allan Gray Investment Summit in Cape Town and Johannesburg on 17 July and 18 July 2018 respectively. To find out more, visit www.investmentsummit.co.za.