The hidden dangers in retirement planning shortcuts

Planning for retirement, which might very well be the biggest investment individuals make, can be daunting. Individuals are not only taking responsibility for accumulating enough capital during their lifetime and investing it correctly, but also for ensuring their accumulated capital can sustain them for the remainder of their lives.

It is no surprise that many people (and sometimes even professionals) rely on rules of thumb to navigate their road to retirement. But there are hidden dangers in relying on mental shortcuts alone.

Understand that your goals may change, as well as your journey to these goals

A well-known rule of thumb to a comfortable retirement is to save 15% of your salary from the time you start working. However useful, this guideline has limitations. Most industries pay more based on work experience, and many people improve their skill sets to fast-track their career and consequent income. Above-inflation increases in income can leave gaps in your retirement planning where you may not be able to achieve a desirable replacement ratio after retirement.

Imagine Joe who starts working at age 25 and saves 15% of his monthly salary. Assuming that his current gross monthly salary is R10 000, this will allow him to enjoy a monthly income of R6 700 (from age 65, in today’s money terms), further assuming a living annuity drawdown rate of 4%. The R6 700 represents a 70% income replacement ratio, i.e. the living annuity will provide him with an income of 70% of his final salary at retirement.

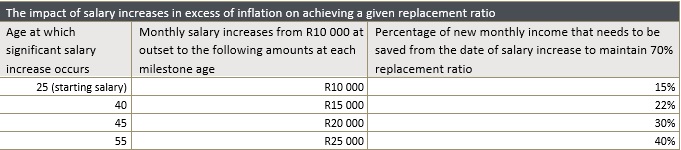

At 40 his salary increases from R10 000 to R15 000. To retire on 70% of a R15 000 monthly income, he will need to increase his monthly savings from 15% to 22% from age 40 onwards. Effectively, his salary increases in excess of inflation must be used to augment his retirement savings. The table below shows how the savings percentage required escalates, based on salary increases at different ages.

Assumptions above: Retirement fund investment grows at 5% in excess of inflation of 6%. There’s a 4% living annuity drawdown in retirement.

At this point, his retirement plan has mainly been derailed as he has most likely experienced ‘lifestyle creep’ and his relative disposable income is now less. Later, as Joe becomes a victim of his own success by earning two and a half times his starting salary at age 55 (in current money terms), he would have to start saving 40% of his income to generate an annual income of 70% of his final salary.

Should Joe want to be able to retire comfortably, he’d need to save closer to 25% of his income over his lifetime, which will increase his likelihood of achieving a replacement ratio closer to 70%, if salary increases are in excess of 2% above inflation. Or he could adjust his expectation of retiring on 70% of his final working salary to a more achievable figure.

How to reach 70%:

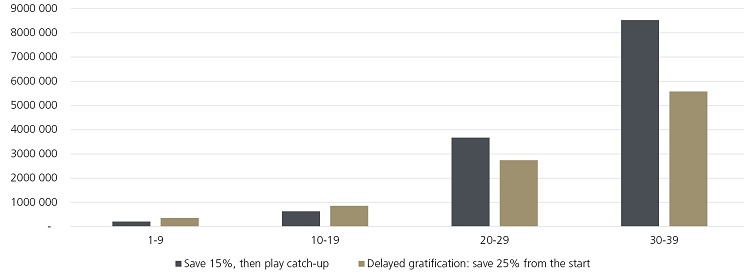

The graph below compares the absolute contribution amounts paid when:

• saving 15% of Joe’s income and increasing contributions to remain on track to achieving a replacement ratio of 70% (‘playing catch-up’ - as per the table)

• saving 25% of his income consistently over his working years

Investment contributions over Joe’s lifetime

Source: PSG Wealth

25% is the new 15%: making compound interest your friend

In the above example, saving 25% of Joe’s income allowed compound interest to work in his favour. Compounding needs time and, in this scenario, allowed him to save over R3.5 million in contributions over his accumulation phase, compared to starting with a 15% savings rate and then playing catch-up. Further, Joe would benefit in terms of tax relief as well (claiming up to 27.5% of the greater of remuneration or taxable income, up to a maximum of R350 000 per year). If Joe had started with a 15% savings rate, he would lose out on maximising this tax relief exactly when he needed it most – the last 10 years of his working career (compared to saving 25% from the outset, and throughout his career).

Forming habits is key

It is difficult to be disciplined and continue living below your means as your salary increases, but prioritising. savings means avoiding living beyond your means. Revisit and visualise your goals regularly to remain committed to achieving them.

Working with a qualified financial adviser will help articulate the nuances in your own income story, and can help you avoid the pitfalls of simply relying on rules of thumb when it comes to retirement planning, while factoring in your financial plan overall.