Tax-efficient ways to save for retirement

Only 6% of South Africans will be able to retire comfortably, according to National Treasury. Further to this, the Just Retirement Insights survey conducted by Just SA estimates that there is a 22% shortfall between expectations and actual retirement provisions based on current annuity rates.

Some of the major reasons for inadequate retirement savings include lack of proper retirement planning, longevity and health risks.

Proactive retirement planning, in consultation with a qualified financial adviser, could provide you with opportunities to maximise any pre-retirement benefits available, such as tax-efficiencies.

Let’s look at some of the tax-efficient options available to save towards your retirement.

Maximise Retirement Annuities tax benefits

Retirement annuities (RA) provide ongoing tax benefits over the full term while you are saving for retirement, offering tax exemptions on contributions (up to certain limits) and on investment gains.

One way to boost your retirement savings and score added tax rebates is to increase contributions by topping up your RA in a tax year. If you do not have a RA, you could acquire one before the end of the tax year to take advantage of the tax benefits.

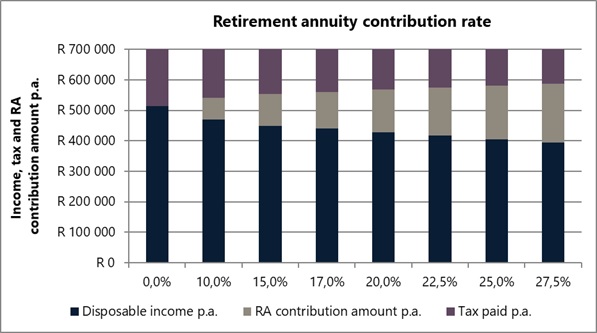

If you save for retirement in an RA or an employer provident or pension fund, you can claim back up to 27.5% of remuneration, or taxable income up to R350 000, in a tax year. The tax deduction limit applies to the cumulative annual retirement contributions, regardless of whether you have saved in a retirement annuity fund, a pension fund or a provident fund. If you exceed the 27.5% maximum limit of your income, it can be carried forward to reduce tax liability in future tax years.

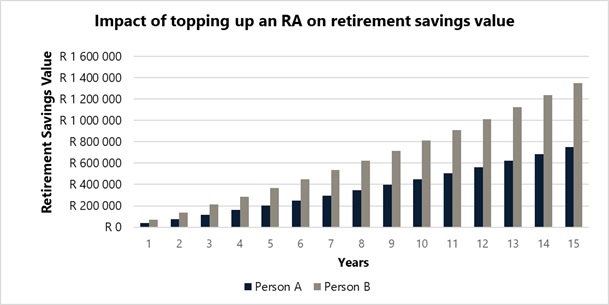

Boost your retirement savings by 80% when you top up your RA over 15 years

The biggest advantage of topping up your RA is that you will have boosted your retirement savings over the long term, and the power of compound interest really takes full effect over time. In terms of tax benefits, the more you top up your RA contribution for the year, the higher the tax benefit, but you will have a lower immediate disposable income, as a result.

The graph below shows the impact of topping up your RA, and the resultant decrease in taxes due.

One way to mitigate the decrease in disposable income is to top up your retirement annuity with a windfall, such as a bonus or inheritance.

By using your annual bonus to top up your RA, you could potentially save up to 80% more than someone who does not. Because you’re using your bonus to top up, you will not feel the impact too heavily on your disposable income.

Additional tax benefits of using an RA

Structured as a tax-efficient vehicle to save towards retirement, you’ll essentially only pay tax when you retire and start drawing an income from the RA. If you did not claim any contributions during the RA term, you can deduct this at retirement.

When you retire, you can withdraw up to one-third of your RA and the remaining benefit will need to be invested in a product to provide you with a retirement income, for example a living annuity. You’re allowed one tax free lump sum withdrawal of R500 000 before you retire, across all retirement products.

Further to this, you don’t pay capital gains tax (CGT) on the return on your investment with an RA.

Augment retirement savings with a tax-free investment account

Another tax-efficient way to supplement retirement savings is through a tax-free investment account.

It offers an investment option with zero tax on investment income or growth and no Dividend Withholding Tax (DWT). You can invest up to R33 000 per tax year until you reach the lifetime limit of R500 000.

While it is not designed to be your sole source of retirement savings, it presents an opportunity to boost your nest egg with a lump sum. It’s important to note that if you exceed the annual or lifetime limit there are significant tax penalties that could erode the value of your investment.

Recent research conducted with financial advisers revealed that nearly 50% of their clients use tax free investments for retirement. Both an RA and a tax-free investment are extremely tax-efficient vehicles to be considered in any retirement plan.

It is recommend that you discuss the best combination of RA top up and tax-free investment as part of your broader retirement plan, which should be aligned to your risk profile and time horizon, with your financial adviser.