Step up your retirement returns

Carl Roothman CEO of Retail Business at Sanlam Investments.

How do you step up your clients’ returns while staying within the limits of Regulation 28?

In 2011 Minister Gordhan announced changes to Regulation 28 of the Pension Funds Act to make sure SA retirement savings are ‘invested in a prudent manner that not only protects the retirement fund member, but is channeled in ways that achieve economic development and growth’. In short, Regulation 28 is a mechanism the state uses to protect the investor against large, permanent losses by forcing the diversification of retirement savings across different asset classes.

So how is it possible to step up your clients’ returns while staying within legislative limits?

What are these limits?

Currently, Regulation 28 permits:

- 75% exposure to equities

- 15% exposure to hedge funds and private equity combined (10% maximum for each of these)

- 10% exposure to commodities

- 25% exposure to property

- 25% exposure to international assets

- 5% exposure to Africa.

The adviser’s challenge

As adviser you play a key role in ensuring the best possible retirement outcomes for your client. Your clients may vary in their investment needs, their risk tolerance and time horizon, but your younger and your most aggressive clients often pose a challenge: How do you maximise their long-term returns (which could otherwise be solved by allocating 100% to equity) while staying within the Regulation 28 limits (allowing only 75% equity exposure)?

Four levers for maximising retirement fund returns

1 Use the 75% equity allocation

Firstly, use the full 75% allocation to equities, provided your client has a sufficiently long investment horizon to stomach volatility. Over the past five decades and longer, equity has outperformed all other asset classes significantly. Over the long term, a higher allocation to equities can enhance portfolio returns considerably.

2 Add alternative and other investment allocations

Alternative investments, specifically fund of hedge funds (FoHF) and fund of private equity funds (FoPE), offer relatively uncorrelated returns in comparison to traditional asset classes like equity, bonds and cash.

3 Add more property

There is no maximum on the combined exposure of equity and property, meaning these two asset classes combined could theoretically take up the entire portfolio.

4 Use the Africa allocation

Additional geographic diversification is allowed through Africa exposure of up to 5% in addition to the 25% exposure to international assets generically. Total foreign exposure can therefore reach 30%.

Results of using the levers

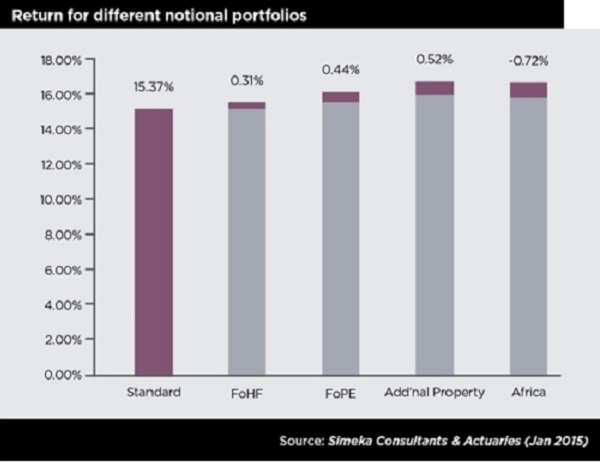

The chart below shows that the returns of a more typical Regulation 28-compliant portfolio could have been enhanced by more than 0.5% per year with the use of alternative asset class allocations over the last 15 years (measured toward the end of 2014).

An extra 0.5% per annum makes a significant difference over the long term. It is worth noting that the Africa allocation would have reduced the total return over this period, since this geographic collective performed very poorly over that time.

However, these phenomena move in cycles and over the next 10 years this allocation may even provide the best return of all the asset classes. The conclusion is that the long-term expected return can potentially be enhanced by even more than 0.5% per annum without paying too dearly in terms of the risk taken.

A word on risk

An investment with more inherent investment risk is expected to provide a better return in the long term in order to incentivise investors to allocate capital to it. However, that risk can, per definition, lead to losses. Bear in mind that the higher expected return is by no means guaranteed – particularly over shorter time periods (less than five years).

The revised Regulation 28 allows you, the adviser, a great deal of flexibility to adjust the risk profile and increase the potential returns of your client.

Part of this article is a reproduction of research that appeared in the Boabab newsletter. It is republished with the kind permission of Kobus Hanekom and Willem le Roux from Simeka Consultants & Actuaries.