Saving for retirement tax-efficiently

Investing in retirement products not only offers tax benefits but is designed to offer a structured approach to saving towards retirement over the long term, along with features to help safeguard retirement savings.

Tax incentives were introduced by the government in the early 1920’s to encourage people to save towards their re¬tirement. There are several tax benefits associated with retirement savings. In this article we will discuss some of the ways to take advantage of the tax benefits associated with saving towards retirement through retirement annuities (RA).

Boost your retirement capital

A key consideration when saving for retirement is to ensure that you have enough funds to retire comfortably. By saving towards retirement in an RA, you can increase the absolute amount of your pension pot by topping up your RA.

One of the biggest advantages of topping up your RA is that you will have boosted your retirement savings over the long term, and the power of compound interest really takes full effect over time.

You can further boost your retirement savings by reinvesting the tax rebate received from SARS, when you include your RA contributions in your tax return.

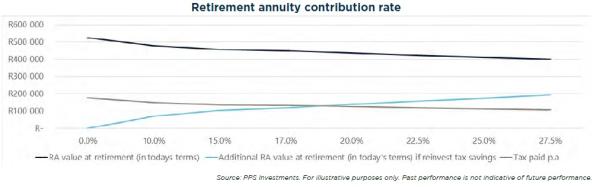

Top up your RA

When saving for retirement with an RA, you can claim back up to 27.5% of remuneration, or taxable income of up to R350 000, in a tax year. The tax deduction limit applies to the cumulative annual retirement contributions, regardless of whether you have saved in a retirement annuity fund, a pension fund, or a provident fund.

The tax benefit can be carried forward to reduce tax liability in future tax years if you exceed the 27.5% maximum contribution limit. Ultimately, the more you top up your RA contribution for the tax year, the higher the tax benefit.

Dividend, Interest and Capital Gains Tax benefits of an RA

In addition to the tax-deductible premiums, RAs are exempt from tax on dividends and interest, and no Capital Gains Tax is payable on growth earned in the investment.

The tax benefits extend to when you reach retirement, where you can make one tax-free withdrawal, which can be up to one-third of your investment as a lump sum and the first R500 000 is tax-free. Any lump sum withdrawal exceeding the R500 000 tax-free portion will be taxed according to the retirement tax tables. If you have more than one RA or retirement savings ve¬hicle, the withdrawal limit applies to your total retire¬ment savings amount.

Tax-free investments – another opportunity to save on tax

One of the most popular savings tools is a tax-free investment account (TFIA).

Since launching in 2015, tax-free savings and invest¬ments have become a popular choice. The tangible benefit of a TFIA is that individuals do not have to pay Income Tax, Dividends Tax or Capital Gains Tax on the returns from their investments. Individuals can invest up to R36 000 per tax year until they reach the life¬time limit of R500 000. TFIA’s can help boost your tax benefits and bolster your retirement savings.

Although tax-free investments are not designed to be your sole source of retirement savings, they do present an opportunity to boost your nest egg with a lump sum. Tax-free investments are not subject to Regula¬tion 28 (which limits the percentage allocated across assets or asset classes) offering more freedom around choosing investment options.

It is important to note that if you exceed the annual or lifetime limit you will face significant tax penalties that can impact the value of your investment. In addition to the tax benefits, tax-free investments should be part of any financial portfolio. Tax-free investments can be used as a strategic part of your financial, retirement and estate planning. Furthermore, it affords you the opportunity to diversify your portfolio exposure across asset classes (bonds, cash, equities, etc.) with no limits or restrictions, to suit your unique financial needs.

Carefully consider all retirement vehicles

Both an RA and tax-free investment are extremely tax-efficient vehicles to be considered in any retire¬ment plan. Your financial adviser will be best placed to provide you with more information on how you can access the PPS Retirement Annuity and PPS Tax Free Investment Account, and provide guidance aligned to your unique circumstances and retirement plan.