Saving for retirement? How much is enough?

According to National Treasury, only six per cent of South Africans are able to maintain their current lifestyle as well as uphold their current income when they retire; echoing the fact that South Africans save very little.

Countries such as Denmark, Australia, Holland and Switzerland rank amongst the best in the world when it comes to pension systems; this is according to the Mercer Global Pension Index. Whilst South Africa is not included in this Index, one question begs an answer - where will South Africa feature when the proposed retirement reform comes into effect next year?

Nico-Louis Minnie, Head of Wealth Management Platforms at Liberty Investments explains that while the sentiment is valid, consumer education coupled with proper financial advice on how much to save towards retirement should continue to take place.

He says that the current system, that allows employees to cash in their retirement savings when they leave their employers or change jobs, has far reaching complications at retirement.

“The proposed reform aims to discourage withdrawals and change the thinking by promoting the preservation of consumer’s long term savings,” a welcome proposition, according to Minnie.

He says most South Africans are ill-equipped for retirement and adequate education around this is the only way to make people aware of what it takes to retire comfortably.

Liberty will be providing all financial advisers with brand new tools to clearly and intuitively articulate the retirement needs their clients may have; a first step towards this consumer education.

Using the chart below to illustrate a scenario, Minnie explains the amount a South African investor can expect to receive as a monthly pension (that keeps up with inflation in retirement) if he invests R1 000 per month until retirement.

For example, a 30 year old male can expect to receive a monthly pension of approximately R9 000 a month if he invests R1 000 per month until he reaches 60. “As you can tell from the illustration, the later one starts to invest, the more one needs to invest. There are also external factors one needs to be mindful of, such as our increasing life expectancy. We are living past the standard retirement age and our long-term plans must ensure that we account for this; and plan effectively to ensure we are able to maintain our current lifestyles well into retirement,” says Minnie.

Minnie says R1 000 a month therefore, does not seem enough given the lifestyle of a 30 year old high income earner of today.

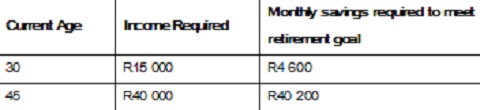

The scenario outlined below is what a client needs to save on a monthly basis in order to be able to draw the required pension. For example, in order for a 30 year old to receive a monthly pension of R15 000, he would need to invest at least R4 600 per month until he reaches the age of 60.

Both scenarios assume that there is currently no retirement provision

Ultimately, the sooner one starts to save for retirement the better.

“First-time job starters must be encouraged to put away as much money as possible. Salary increases or any cash windfalls should be injected into retirement savings as this will ensure maximum pension at retirement age therefore allowing you to maintain your current lifestyle.”

References: