Retiring comfortably requires planning

Duane Littler, Executive of Business Development at PPS Investments.

Investing enough, starting as early as possible and select¬ing an optimal retirement savings vehicle are critical in working towards a comfortable, self-sufficient retirement. This becomes even more pertinent in light of some emerg¬ing trends that have a growing impact on retirement sav¬ings – longevity, healthcare costs after retirement as well as the prospect of an earlier retirement.

Longevity: With medical advances and greater awareness of healthy lifestyle choices, people are living longer which means that their retirement savings need to last longer. How much longer will people be living on average by the time you retire, and what impact will this have on your retirement plans? The improvement in longevity over time means that you must review your retirement plans regularly to ensure that you are still on track for the retirement you desire.

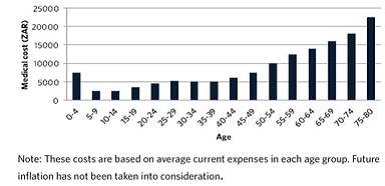

Healthcare costs: More and more healthcare-related costs are being passed on to individuals after retirement. Many companies no longer subsidise medical scheme contributions for pen¬sioners, and many pensioners have been forced to reduce their medical scheme benefits in order to be able to afford the contributions. As the graph below shows, the average an¬nual cost of medical care increases with age, so your retire¬ment plans should allow for this expense or for the cost of comprehensive medical scheme cover after retirement.

Early retirement:

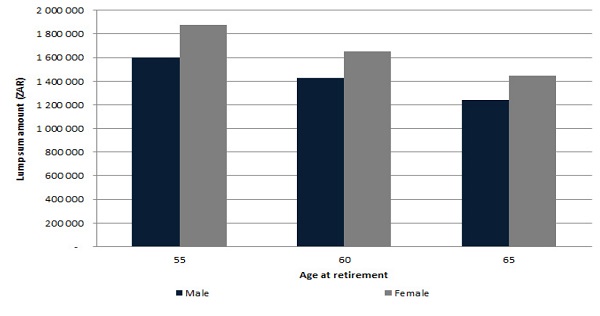

Many South Africans are offered the option by their employer to retire at an earlier age. This has the same impact as increasing longevity in that your retirement savings need to last for longer, but in this instance you also have less time to grow these funds. As the below graph shows, the funds required to retire at age 55 or 60 are significantly higher than if you were to retire at age 65. This makes an early start to retirement funding even more important.

Sadly, research shows that only about six percent of all South Africans can afford to retire financially secure. The rest either have to keep working, be supported by welfare, de¬pend on their families for financial support or significantly drop their living standards after retirement. This begs the question: How much do you need to save for a secure retirement?

So, how much do you need to save for a secure retirement?

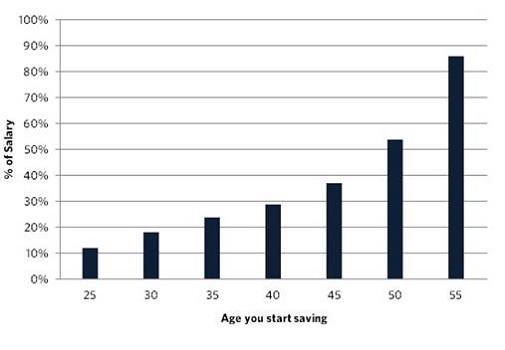

To maintain your pre-retirement standard of living, a general guideline often used to plan, is based on an income of approximately 75% to 80% of your salary in the year before retirement or a capital amount of roughly thirteen times your last working year’s salary.

The following graph illustrates what percentage of your in¬come (based on certain assumptions) you will have to save before retirement, starting at various ages, in order to be able to retire at age 65 with an income of 80% of your sal¬ary in the year before retirement. This income will escalate at the rate of inflation each year.

The message is clear. The earlier you start saving, the better your chances of enjoying a financially secure retire¬ment.

Why is an RA an appropriate investment vehicle to use for retirement savings?

Whether you work for a large corporation and have a com¬pany retirement fund, or are self-employed and need to make your own retirement provision, a retirement annuity fund can be the ideal vehicle to use to secure or to boost your retirement funding. Here’s why:

Tax benefits: The contributions that you pay towards a retirement annuity fund are tax deductible within certain legis¬lated limits. In addition, the investment returns achieved on the assets held within a retirement annuity fund are tax free.

Protection from creditors: The investment in your retirement an¬nuity fund cannot be attached by creditors or used as collateral, so your retirement is safe, even if something happens to your business.

Ad hoc payments: You have the flexibility to make ad hoc contributions to your retirement annuity fund, so that you can maximise your tax deductions based on your actual annual drawings from the business.