Retirement reform and tax changes: A timely boost for employees in an ailing economy?

Government has been reviewing and changing the rules that govern the retirement fund industry, to enable a uniform retirement system through the annuitisation of provident funds.

Annuitisation means to purchase a pension with a lump sum (in this case the lump sum that you have saved as a result of contributing to a retirement fund).

Along with aligning provident and pension funds, the new rules aim to protect post-retirement incomes and curb the risk of people depleting their retirement savings too quickly, after retirement.

The long-awaited reforms will come into effect on 1 March 2021, otherwise known as T-Day.

How will the new rules affect members of retirement funds?

From 1 March 2021, retirement benefits from provident funds and provident preservation funds will be governed by the same rules as pension funds. Currently, members of provident and provident preservation funds have the option to take their full retirement benefits as a lump sum when they retire. From T-day (1 March 2021), retirement benefits under provident funds and provident preservation funds will be subject to compulsory annuitisation, apart from the vested benefits from the period before T-day.

What are vested and non-vested benefits?

From 1 March 2021, retirement member shares will consist of two portions: Vested and non-vested member benefits. The vested member portion refers to retirement benefits and the interest thereon, up to 28 February 2021. When a member retires, these benefits will not be subject to annuitisation and can be taken in cash.

The non-vested member portion will reflect all retirement fund contributions and interest thereon from 1 March 2021 onwards. Upon retirement, this portion will be subject to annuitisation – unless the total amount does not exceed R247, 500. In such a case, then a member can take the full amount in cash when they retire. If the non-vested portion is more than R247,500, then a member can only take up to one third of the benefit in cash and must use the balance to purchase a pension.

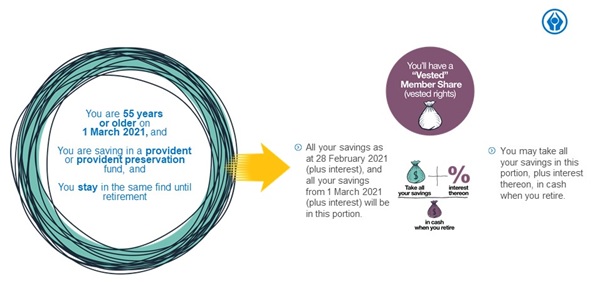

However, there are some concessions to the rules for members who are 55 years and older on T-day.

What are the concessions?

Those who are 55 years or older on 1 March 2021 and are saving in a provident or provident preservation fund, and stay in the same fund until retirement, will not be affected by the new rules. These members will be allowed to withdraw their full benefits (including the interest thereon) when they retire. This includes any contributions made to the provident fund after 1 March 2021.

Member 55 years or older on T-day saving in a provident or provident preservation fund and staying in the same fund

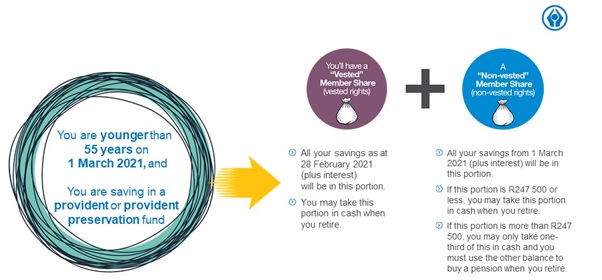

For those younger than 55 on T-day and saving in a provident or provident preservation fund, all benefits accumulated up to 28 February 2021 plus interest will be allocated to the vested member portion. Benefits allocated in the vested portion may be taken in cash upon retirement, resignation, termination or retirement due to illness. From 1 March 2021, all new contributions will be allocated to the non-vested portion of the fund. If the benefit amount in this portion is more than R247, 500, then only one third of the benefit can be taken in cash, and the balance must be used to purchase a pension.

Member younger than 55 years on T-day saving in a provident or provident preservation fund

If a member is 55 years or older on 1 March 2021, but transfers to a new fund after 1 March 2021, all contributions to the provident fund of which he/she was a member on 1 March 2021, plus interest, will remain exempted from annuitisation. At least two thirds of all contributions to the new fund (plus interest thereon) will however have to be annuitised, except if the value does not exceed R247 500.

How will reforms affect retirement fund administration?

T-Day reforms will have a significant impact on the administration of retirement funds. Although pension fund members are not affected by the reforms, they will be affected by the changes to retirement administration systems.

To process these changes, the Sanlam administration system has been configured to maintain two accounts for each member reflecting: vested and non-vested member shares. The vested (cash) portion will contain the member share as at the end of February 2021 and the interest thereon going forward. The non-vested (annuitised) portion will only contain the contributions and interest thereon, as at 1 March 2021 onwards.

Will the reforms improve financial wellbeing?

Although these measures could help to protect people’s retirement savings and ensure that they annuitise at least a portion of their savings, the reforms are not a silver bullet for the financial challenges faced by the majority of South Africans.

With the cost of living in South Africa on the rise, the need for cultivating a savings culture and saving enough for retirement, cannot be overstated. While the new rules aim to protect retirement savings and to ensure that people secure a pension in retirement, on their own, reforms cannot ensure successful outcomes. Improving financial literacy and communication will be central to ensuring that people are empowered to make informed decisions about their short and long-term savings towards a more financially secure future.

Click here for infographic...