Retirement is changing. Are you ready?

We can expect a number of changes from March 2015 and beyond. And the landscape around these changes is a complex one. Increasing longevity means one’s savings need to last longer and government’s proposals around retirement reform aim to encourage investors to act in their own best interests.

Retirement reform objectives include:

• Ensuring that all employees contribute to some form of retirement savings vehicle;

• Ensuring that these savings are preserved for retirement funding only;

• Ensuring that people are able to save through reasonably priced investment products; and

• Ensuring that investors have a sustainable income for life, post-retirement.

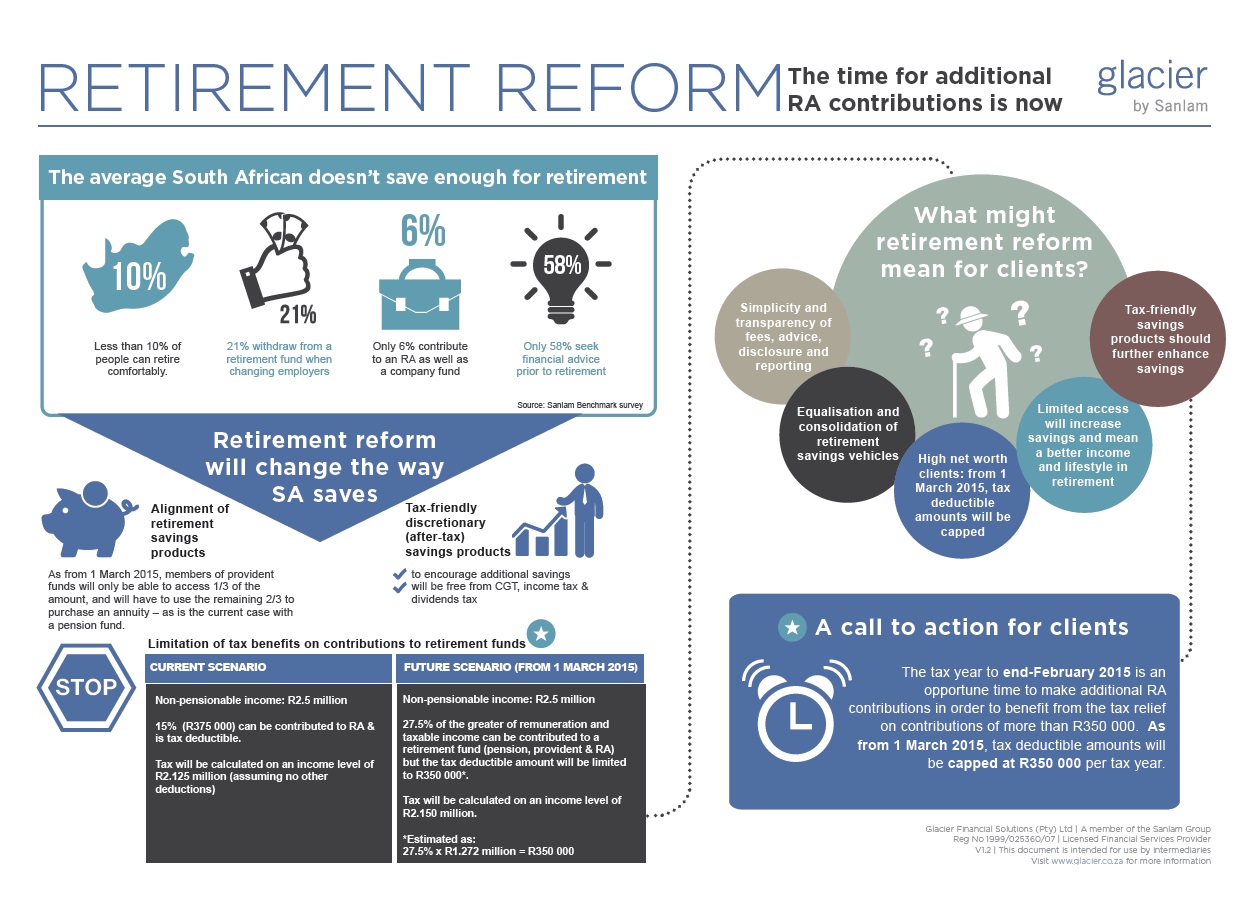

South Africans, generally, do not save enough for retirement. A large proportion tend to cash in some or all of their retirement savings when changing employers. This is evident in the low savings rate of the country - various studies estimate that less than 10% of people can retire comfortably. To increase the level of retirement savings, Government believes tax incentives can play a valuable role.

New savings products for a new landscape

From 1 March 2015, Government is expected to introduce tax-friendly discretionary (after-tax) savings products, designed to encourage additional savings, over and above compulsory retirement savings.

The intention is that these savings vehicles will not attract capital gains tax or tax on income and dividends. However, there will be an initial annual contribution limit of R30 000 and a lifetime limit of R500 000. These amounts will be inflation-adjusted on a regular basis. Once this product has been launched, the current interest exemption (R23 800 for persons under 65, and R34 500 for persons 65 years and older) will no longer be adjusted for inflation.

A new alignment of retirement savings products

Also on 1 March 2015, the deduction of contributions and the lump sum payable in respect of pension and provident funds will be aligned. Benefits will also be treated the same way for contributions made from this date. Currently, members retiring from a company are able to withdraw 100% of their contributions in a provident fund. From 1 March 2015, the member can only access one-third of the amount and will be compelled to use the remaining two-thirds to purchase an annuity – as is the case with a pension fund. Members can still withdraw all contributions (and the growth thereon) made to a provident fund prior to this date.

If the total amount in the provident fund, pension fund or retirement annuity (RA) is less than R150 000 at retirement, then the member may withdraw the full amount in cash.

The new cap on tax benefits on retirement fund contributions

In an attempt to simplify current tax incentives, employer contributions to retirement funds will become a fringe benefit in the hands of employees for tax purposes.

As from 1 March 2015, employees can claim a tax deduction of up to 27.5% (currently 15% of non-retirement funding income) of the greater of remuneration and taxable income on contributions to a pension fund, provident fund or retirement annuity. A ceiling of R350 000 per tax year will apply, and unused deductions may be rolled over to the following year.

Remember that members can continue to make tax-deductible contributions to a retirement annuity even beyond the age of 70.

Your last chance

The R350 000 tax deductible ceiling means that investors have a last opportunity – between now and 28 February 2015 – to make additional ad-hoc contributions to their retirement annuities to enjoy the tax benefits. Excess contributions can be carried forward and as of 1 March this year, can even be utilised after retirement. Let’s look at an example:

Suppose a client’s non-pensionable income is R5 million. 15% (R750 000) of this income can be contributed to an RA and is tax deductible. (Investors may contribute more than this, although the amount above 15% will not be tax deductible). Tax will be calculated based on an income level of R4.25 million, assuming no other deductions. This translates to a massive tax saving.

From 1 March 2015, the tax deductible amount will be calculated as 27.5% of the greater of remuneration or pensionable income but the amount which is tax deductible in the same year as the contribution is capped at R350 000. Under the same scenario, the taxable income will be R4.65 million - decreasing immediate tax advantages dramatically.

Retirement annuities (RAs) have many other benefits which make them an attractive retirement savings vehicle:

• The returns within the RA are not subject to income tax, capital gains tax or dividends tax.

• The lump sum payout at retirement (a maximum of one-third of the capital) or on death, may be tax-free within certain limits that apply to lump-sum payouts from retirement savings products.

• On death, any benefits paid out from an RA are free of estate duty.

• An RA can be used to provide for medical expenses since the income after age 65 will effectively be tax-free if used to fund these medical expenses.

The 2014 Sanlam BENCHMARK Survey identified a few key habits of financially healthy retirees, defined as those earning R25 000 or more per month in retirement:

• Start early - Affluent retirees save for 33.2 years on average, the rest save for about 29 years.

• Save as much as possible – Financially healthy retirees save 8% (excluding employers’ contribution) of their salary, whereas the average is only 7.3%.

• Don’t rely on the company – 37% of financially comfortable retirees have an RA in addition to their company pension fund.

• Leave your savings alone – Only 12% of affluent retirees dipped into retirement savings when they switched jobs – 21% on average did.

• Widen your nets – 98% of affluent retirees have an extra source of income compared to 68% on average.

• Use the pros – 88% of affluent retirees consulted a financial adviser before retirement and 72% after retirement. The average is 58% before retirement and 34% thereafter.

As always, we recommend that investors consult with a qualified financial intermediary who will be able to ensure that their investment portfolio is in line with their risk profile and investment objectives.