Retirement Annuity Cheat Sheet

Arno Olckers, Business Development Manager at Morningstar Investments Management SA

In the words of David Bergmann, “the tax tail should never wag the investment dog”. With that being said, it definitely won’t hurt to know and understand how a Retirement Annuity (RA) can minimise the amount of tax you pay and keep more of your hard-earned cash in your own pocket.

Similar to the fees and other costs you pay on your investment, tax is the cost that can often sting the most and combined, all these costs eat away at your return on investment. If not taken into consideration, taxes can bite off quite a chunk of your investment returns over time.

The ins and outs of the South African tax rulebook and guidelines are complex and very few of us truly understand or have the time to become experts in tax management or investment products. However, knowing some key information regarding a Retirement Annuity (RA) when planning your finances together with your financial adviser can result in a large benefit over time.

In addition to tax savings, the best way to maximise retirement savings is to start early, invest for the long term and make sure you have exposure to growth assets. This is where a RA can add value to an investor over time.

Let’s take a look at the fundamentals of a RA product

An RA is registered in terms of the Pension Funds Act and is a tax-efficient investment vehicle. It is ideal for self-employed individuals, individuals that do not have access to a pension or provident fund through their employer and/or who want to save for retirement (in addition to any existing pension and provident fund savings).

Some key features and benefits of a retirement annuity are set out below:

• You can only access your funds at age 55 when you retire from the product.

• The only two exceptions for an early withdrawal are due to ill health (such as a permanent disability) or if the total value of your combined retirement annuities at a particular service provider is equal to or below R7 000.

• Before 1 March 2021, investors could also gain early access to their funds in the event of them emigrating, however, new law now governs that you will have to wait three years before being able to access your funds.

• There is no tax on interest, dividends, or capital gains while you remain invested in the fund.

• RA investments are protected against creditor claims.

• Your contribution to an RA is tax-deductible, but only to a certain extent. Up to 27.5 % of your taxable income or gross remuneration, and no more than R350 000 is tax-deductible in a tax year. You can use this tax saving and top up your RA in the subsequent tax year.

• Your RA is not subject to estate duty tax.

• At retirement,you can access one third as a cash lump sum (subject to the retirement lump sum tax table) and two thirds must be invested in a compulsory annuity providing an income during retirement.

• RA’s are subject to Regulation 28, which sets limits as to the percentage of exposure a fund may have to certain categories of assets. At the moment a retirement annuity can only invest 75% in local or offshore equities, 25% in local or offshore property, while foreign investment exposure is limited to 30%.

What happens when I contribute more to my RA?

The following rules apply when it comes to the amounts you can contribute:

• You can contribute 27,5% of your total annual taxable income or gross remuneration to a retirement annuity, capped at R350 000 (i.e., the 27,5% may not exceed R350 000).

• Any contributions that exceed your allowable contribution limit will roll over to the next year.

• Every amount by which you over contribute annually will keep rolling over until you retire from your retirement annuity at the age of 55.

Excess contributions can then be used in two ways:

a. As a tax-free portion to withdraw at 55 together with your R500 000, or

b. You can use it in your living annuity and write off any income tax payable against the excess amount (remember, annuity payouts are still taxed within your marginal income tax bracket). (SARS outlines the withdrawal brackets on their website here.)

How will this work in practice? Let’s consider two examples for each option above1:

Option A:

You have R300 000 in excess contributions on record at SARS and have not taken any previous withdrawals or severance benefit packages. The market value of your RA is R3 million, and you choose to take one third in cash at retirement. All calculations were done using the 2022 tax year.

• The cash amount of R1 million will first be reduced by the excess contribution:

R1 000 000 – R300 000 = R700 000.

• This amount will be taxed in the retirement fund lump sum tax table:

(R700 000 – R500 000) x 18% = R36 000.

• If you had no excess contributions the tax you would have paid is R117 000, because you would be applying the retirement fund benefit lump sum tax table on the R1 000 000 and not R700 000.

• This is a tax saving of R81 000.

Option B:

For the second option, we assume you are 58 years old. You have one living annuity that is the only source of income at retirement and this income is R200 000 for the year. You also have R150 000 excess contributions on record with SARS.

• The amount of tax withheld (PAYE) from R200 000 is R36 000 – R15 714 (primary rebate) = R20 286.

You can only reduce your annuity income with the excess contribution when filing your tax return. The SARS refund you will receive is calculated below:

• R200 000 annual annuity income – R150 000 (excess contributions) = R50 000.

• The tax on R50 000 is R9 000 – R15 714 (primary rebate) = R 0.

• This means SARS will refund you the full amount of R20 286

These two examples highlight the benefits of overcontributing to your RA. The higher your excess contribution, the more savings you will have available at and/or during retirement.

Morningstar’s Retirement Annuity solution

Morningstar Managed Portfolios offers a local specialist range of portfolios designed to meet your clients' objectives. In creating and managing these strategies, we draw on our valuation driven asset allocation expertise and industry-leading research to build a sophisticated framework.

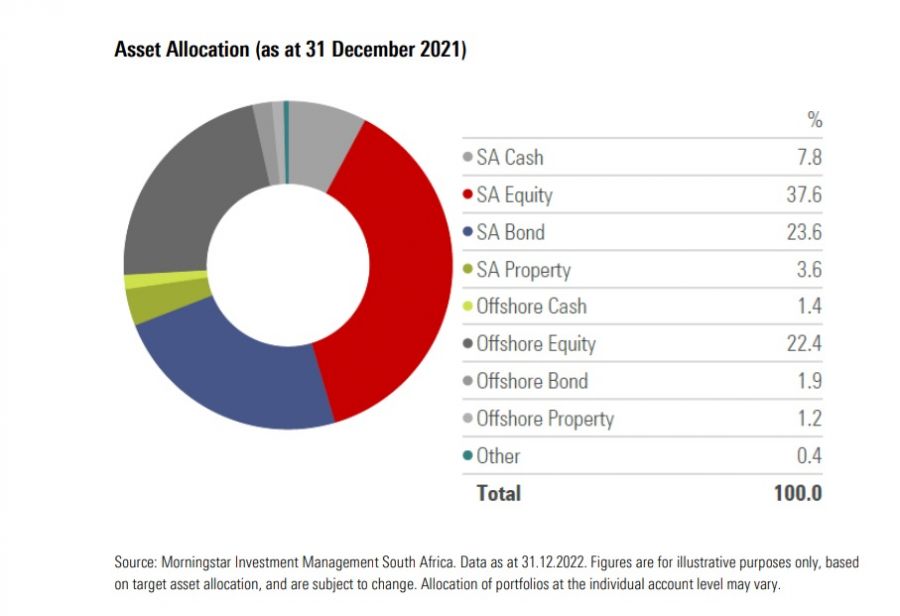

Morningstar offers four regulation 28 Managed Portfolios. The Morningstar Adventurous Portfolio is a multi-asset portfolio, aimed at providing investors with long term capital growth through managed exposure across equities, bonds, cash and offshore investments. The portfolio aims to generate a return of CPI + 5% per annum over any rolling seven-year period. The portfolio is suitable for high-risk investors and is limited to a maximum of 75% equity exposure.

The Morningstar Adventurous portfolio is available via the following platforms: Ninety One, Glacier, Allan Gray, Momentum Wealth, PPS, Stanlib, INN8, AIMS and Old Mutual Wealth.

Underlying Fund Managers:

• Ninety One Equity

• Fairtree Equity

• Aylett Equity

• Coronation Strategic Income

• Ninety One Diversified Income

• Nedgroup Inv Core Bond

• PSG Equity

• Ninety One Global Franchise FF

• Nedgroup Inv Core Global

• Nedgroup Inv Global EM Equity FF

In Conclusion

Households across the globe are increasingly expected to be responsible for more financial decisions, such as determining how much to save for retirement, how to invest savings, how to be tax-savvy and when to retire. It’s a tricky one – especially if no one in your household is a trained financial planner and/or adviser.

Within that reasoning, you might as well also be in charge of doing the plumbing and electrical installation for your home. While you might be able to fix a simple leak – it’s not as easy when your geyser bursts and floods your entire house. Ironically, it’s for this exact reason that you are also expected to have the correct financial planning and insurance in place.

When it comes to retirement planning, we encourage investors to speak to their financial adviser, who will be best suited to help them get the most out of their hard-earned savings and investments.