Retirees: Why your return may not be quite what you realise

Many pension fund members faithfully contribute to a pension fund with clear expectations of the quantum of return they will receive upon retirement. However, according to statistics from the Pension Funds Adjudicator’s (PFA), the complaint most often received from fund members is that the fund payout does not correlate with promises made by their broker or the product provider. The amount of money that ultimately appears in their bank account is often much less than anticipated.

Rowan Burger, Head of Alternative Products at Momentum Employee Benefits says: “I am concerned that 57% of complaints received by the PFA’s office are from members unhappy about the amount of the benefit paid, especially considering we are coming off five years of the best investment returns we are likely to see in another decade. Imagine how much worse it could have been if the market did not beat inflation!”

Burger explains that at the root of this expectation gap is poor member communication. There are a number of key misunderstandings trustees critically need to address.

One key cause is that fund contributions are calculated as a percentage of pensionable salary rather than of total earnings. Most employers determine pensionable salary at between 70 - 85% of total cost to company salary, leaving a gap of 15 - 30%. Contributions are therefore a lot lower than most members realise. This contribution is further reduced by almost a third once death and disability insurance costs and administration fees are deducted.

“Let’s say you are earning R100 000 per annum with a 15% of salary contribution to a pension fund. You may think you are on the right track, but the reality is that your contributions are equating to 15% X R80 000 (pensionable salary), which leaves you with R12 000. So while you may be expecting R15 000 yearly savings, once fees are deducted you are left with around R9 000 in retirement savings, explains Rowan.

“For the sum to be R15 000, you would require a return of 66.7% on your contributions each year – a once-in-a-lifetime outcome.

“Investment performance is often blamed, but this is generally not the cause. When members see strong returns from equity markets, they are disappointed to discover their pension fund did not deliver similar returns. As Section 28 of the Pension Funds Act restricts the investment of pension funds into equities, members cannot expect a full equity return from their fund.”

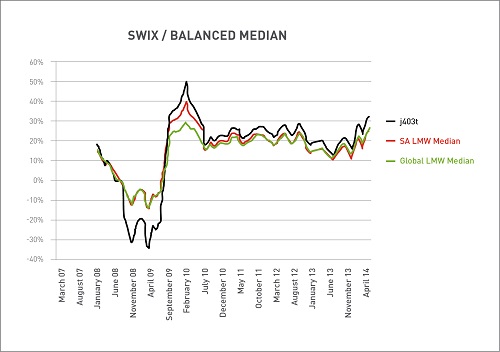

If one compares the returns on the average balanced fund with equity returns (see the graph provided), it is clear that balanced funds return less than pure equity investments. However, the return is smoother, making these funds a more prudent option, as is required by law.

Burger points out that up to a third of the pension fund payout when exiting early could vanish into the taxman’s coffers. In addition, members who used their pension fund as surety for a housing loan soon discover that the loan is settled first.

Burger says: “Outcome 5 of the Treating Customers Fairly (TCF) regulations stipulates that products should perform as product firms have led members to expect. Our interests as a product provider are closely linked to those of fund members. It is on our interest to meet their expectations as well as build assets appropriately”.

“The divergence of the expectation created by the broker and the client from the eventual payout highlights the need for ongoing communication. Financial education is an important part of TCF and will go a long way to tempering member expectations and avoiding the disappointment many members feel after years of diligently contributing to a pension fund,” concludes Burger.